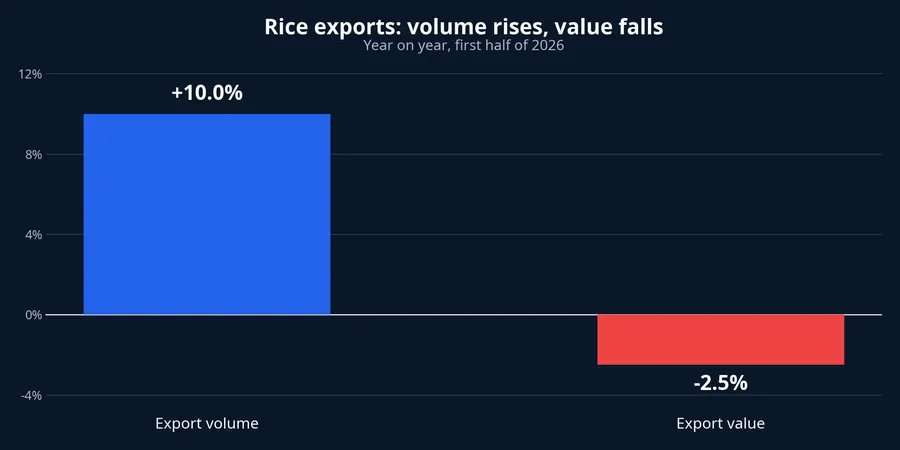

More bags leaving a port makes for an encouraging picture. For a rice exporter, though, higher volumes do not automatically translate into more value for shareholders. The first half of 2026 offers a clean illustration: Vietnam exported 5.2 million tonnes of rice, up 10% year on year, while export revenue came to USD 2.4 billion, down 2.5%.Thanh Niên

Those two figures are not contradictory. Volume measures goods sold; export value measures money received. Average selling price connects the two. When the price decline is larger than the volume gain can offset, total revenue can still fall. For a new investor, that is a much more useful starting point than a headline saying only that shipments rose.

A simple equation with a material difference

Put simply, export revenue equals volume multiplied by the average selling price. In the first half, Vietnam's average rice export price fell 11.3% from a year earlier to USD 459.6 per tonne.Thanh Niên That decline was large enough that a 10% increase in volumes did not turn into growth in export value.

The chart is not evidence that rice demand has weakened. Higher volumes suggest that buyers are still absorbing supply. What it does show is pressure on revenue quality: each tonne generated less money than it did a year earlier. That is the difference between selling more product and selling it on more favourable terms.

Average prices can fall because prices across grades have declined. They can also fall because the mix has shifted toward lower-priced rice, or because exporters accept more competitive prices to retain customers and enter new markets. Each explanation carries a different implication for profit, so aggregate volumes alone cannot tell us how an individual company is performing.

A benchmark price is not a company's realised price

In early July, Vietnam's Jasmine rice price rose by USD 8 to USD 520 a tonne, while fragrant 5% broken rice gained USD 5 to USD 510 a tonne.Thanh Niên The international rice benchmark contract also stood at USD 13.44 per hundredweight on July 9, 8.5% above June 9. That is a constructive signal for the rest of the year, but it is not yet proof that profit margins have recovered.

Market quotations and the price recorded in a company's accounts are different things. The realised price depends on grade, contract timing, destination and freight terms. An exporter may still be delivering older contracts agreed at lower prices even as current quotes improve. Conversely, a company with more fragrant rice or more flexible contracts may feel the benefit sooner.

That is why the next quarterly or half-year report calls for more than a revenue-growth figure. Investors should check whether cost of goods sold moves in the same direction, whether gross margin changes and whether inventory is expanding or contracting. Those lines show whether firmer market prices are actually reaching the financial statements.

A new market helps only if the order economics work

The Philippines remained Vietnam's largest buyer, accounting for 45% of rice export volume in the first half.Vietnam Investment Review A large destination supports scale, but that concentration also gives one market substantial influence over industry pricing and purchase terms. Investors should treat it as a measure of dependency, not simply a welcome market-share statistic.

China, meanwhile, bought more than 1 million tonnes, up 87% year on year, and represented 19.4% of the market mix.Vietnam Investment Review This may support fragrant rice, glutinous rice and specialty products, which typically command higher value. The aggregate data does not, however, disclose the exact grade mix of all orders. It is more accurate to view this as a potential improvement in revenue mix than to declare that average selling prices will rise.

Iraq also increased its purchases sharply, with imports of Vietnamese rice 132.4 times higher than a year earlier.Vietnam Investment Review The percentage stems from a low comparison base, so it does not mean Iraq has replaced core markets. More useful questions are what grades it is buying, at what price, on what payment terms, and whether the orders recur or represent a short-lived purchase cycle.

Costs determine what remains for the exporter

Even a recovery in selling prices does not flow directly into profit. Rice exporters carry costs for paddy procurement, drying and milling, packaging, storage, transport and working capital. International urea reached USD 416.5 a tonne on July 9, 7.7% above the start of the year. This is not the actual cost base of every Vietnamese rice company, but it is a reminder that agricultural inputs can rise alongside commodity prices.

Inventory management therefore matters. A company that buys paddy at a sensible price, stores it well and delivers under favourable contracts can protect its margin. One that has fixed its selling price while procurement costs rise may report higher revenue yet face a squeezed gross margin. Operating cash flow is the final check: selling more while collecting cash slowly can still raise the need for working capital.

This also explains why companies in the same industry can produce very different results. The gap need not be export scale. It may instead reflect product mix, contract quality, inventory turnover and discipline over costs.

For that reason, a single favourable price quotation should be read as a clue, not a verdict on earnings. The combination of contract timing, inventories and cash collection determines whether an improvement in the market becomes an improvement in reported profit.

What to watch in the second half

The central thesis is that higher shipment volume is a positive signal for demand, but it does not confirm profit quality. To test that thesis in the next reports, investors should watch the average export price per tonne, the mix of fragrant and standard rice, exposure to major destinations, gross margin, inventory turnover and operating cash flow.

The early-July price increase could improve the picture, especially if new orders concentrate in higher-value segments. But the market can only say that incremental rice volumes have created more shareholder value when average selling prices stabilise or rise, costs do not overwhelm them, and cash collection keeps pace with revenue. The next quarterly report should provide the missing part of that equation.

This framework also keeps the analysis from becoming a prediction based on one headline. A rise in volume can coexist with weak pricing; firmer quotations can coexist with old low-priced contracts; and higher revenue can coexist with pressure on working capital. Each of those outcomes is possible without invalidating the others. The useful question is whether several indicators improve together, rather than whether a single headline is positive or negative.

For investors learning to read commodity exporters, this is a practical habit: start with the volume figure, then ask what price sits behind it, what costs sit beneath it and how much cash the company retains after delivering the order. The answers belong together. Looking at only one of them makes a business with thin and shifting margins appear simpler than it is.