One summary statistic made the July 10 session look better than it felt. Foreign investors posted roughly VND 1,393 billion in net buying across the market, including more than VND 1,387 billion on HOSE.VietnamBiz For newer investors, that kind of headline is easy to read as proof that serious money is coming back.

The broader tape said otherwise. The VN-Index closed at 1,828.34, down 12.36 points, while HOSE breadth was still heavily negative with 82 advancers against 239 decliners. Put simply, foreign money did show up, but it was far too concentrated to turn a down session into a broad sign of strength.

That is the core takeaway from this post. Beginners often treat net foreign buying as a green light for the whole market, when the more useful question is structural: was the buying spread across leadership groups, or was it concentrated in one name. On July 10, the evidence points decisively to the second scenario.

Real inflows, but mostly into VIC

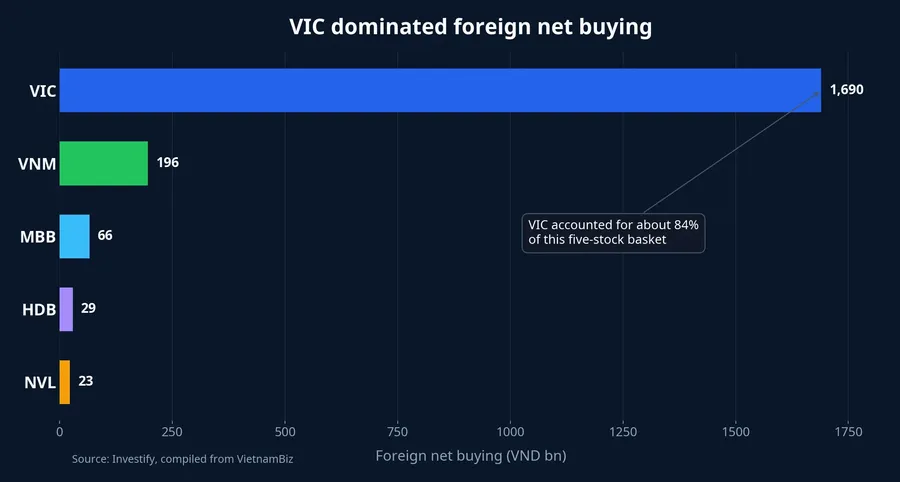

Once you strip away the headline number, the picture changes quickly. VIC alone absorbed about VND 1,690 billion of foreign net buying, equal to roughly 8 million shares, which was actually larger than the entire exchange-level net buying figure for HOSE that day.VietnamBiz At that point, the story is no longer “foreign investors returned to the market.” It is closer to “foreign investors targeted one very specific trade.”

Everything behind VIC was much smaller. VNM saw about VND 196 billion in net buying, MBB VND 66 billion, HDB VND 29 billion, and NVL VND 23 billion.VietnamBiz The gap is so large that it is hard to frame the day as a broad risk-on move in index leaders. It looks much more like a highly selective allocation.

The easiest way to think about it is this: if someone walks into a supermarket and spends almost all their money at one counter, you would not conclude that the whole store is crowded. Equity markets work the same way. A very large order in VIC can flatter the aggregate data without proving that risk appetite has spread across the board.

That is why headlines like “foreigners bought more than VND 1,300 billion net” can mislead when they stand alone. The number is correct, but it does not answer the question that matters for retail investors: was your part of the market actually inside that flow. If the answer is no, portfolio reality can look very different from headline sentiment.

Breadth shows the market was still fragile

In sessions dominated by a handful of large caps, breadth becomes the second essential filter. The VN-Index is weighted by market capitalization, so a small cluster of heavyweights can keep the index from looking as bad as the average stock feels. Newer investors often miss this because they start with the index and only later check what individual stocks actually did.

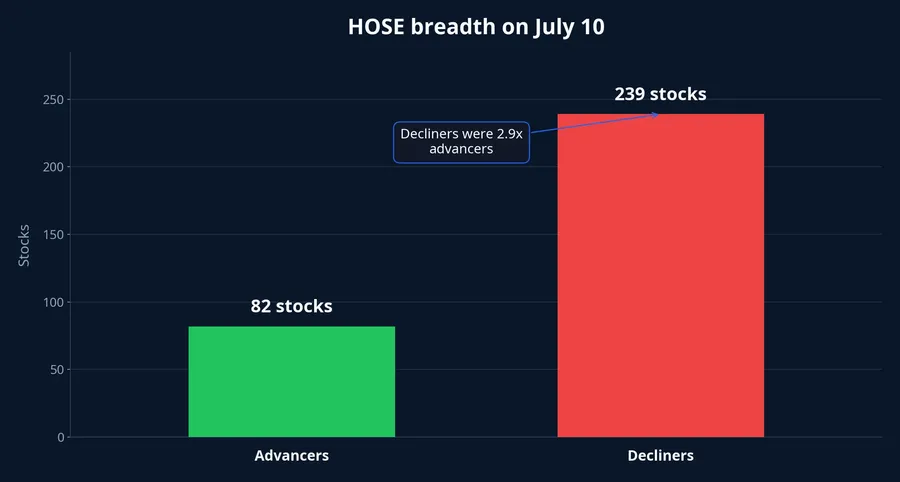

July 10 is a clean example of why that sequence should be reversed. HOSE recorded just 82 advancers against 239 decliners, meaning losers outnumbered gainers by almost 2.9 times. When breadth is that skewed, the market is signaling either deep fragmentation or broad weakness, not a healthy advance.

Another way to say it: the headline index can be supported by a few pillars, but breadth captures the experience of far more accounts. If most stocks are still red, investors should be careful about treating the session as confirmation that the market as a whole has turned stronger. At most, it shows that capital was active. Whether that capital was narrow or broad is what determines how durable the move might be.

This is the difference between local support and real market health. Local support can stabilize the index for a day or two. Real health is only confirmed when flows start to spread across sectors, across market-cap buckets, and across the stocks that normally drive sentiment.

One pillar was not enough to change the session

VIC did play the role of a pillar. The stock closed at VND 222,800, up 0.81%, which helped cushion the index against broader selling pressure. But one rising heavyweight is not enough when several other large caps are still moving lower at the same time.

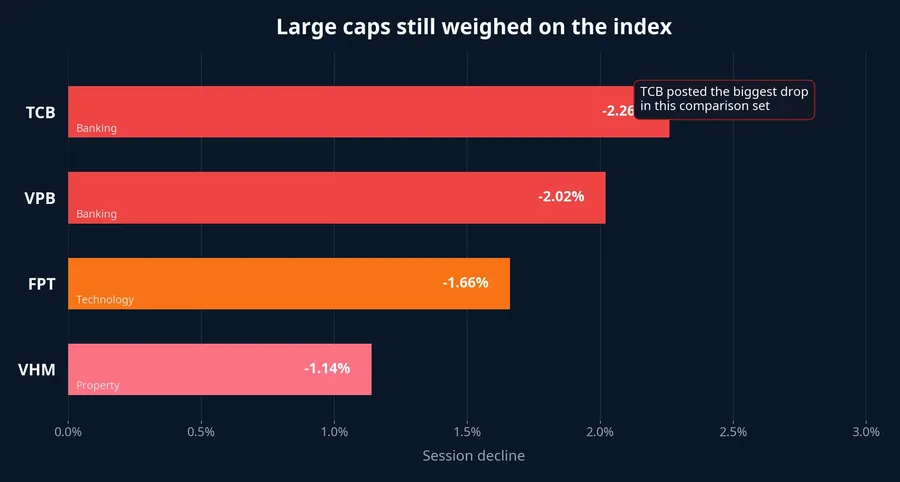

TCB fell 2.26% to VND 32,400 per share, VPB dropped 2.02% to VND 26,700, FPT lost 1.66% to VND 70,900, and VHM declined 1.14% to VND 147,000.VnEconomy That mix matters because the pressure did not come from one isolated corner of the market. It came from banking, technology, and property, which are exactly the groups with the power to shape both the index and overall sentiment.

There is another useful detail here: foreign investors were not even buying evenly within the large-cap universe. FPT still saw roughly VND 119 billion in net foreign selling, while VPB posted about VND 82 billion in net selling.VietnamBiz That strengthens the case that July 10 was not a basket-style return to Vietnam equities. It was a selective flow tied to specific names.

So if someone uses “foreign net buying” alone to argue that the market is improving broadly, that conclusion runs ahead of the evidence. The July 10 data support a more disciplined reading: a heavily bought index pillar can improve the mood of the headline, but it does not automatically improve the quality of the tape underneath.

How retail investors should read this setup

This matters for process more than for the single session itself. When a large net-buying number appears, the first reaction should not be excitement. It should be a three-step check: which stocks absorbed the money, what did breadth look like, and which groups were pushing or pulling on the index. Only when those layers point in the same direction does the market message become more trustworthy.

On July 10, the layers did not align. Foreign money came in hard, but it was narrowly focused on VIC. Breadth remained weak, while major banks and a key technology name were still falling or being sold. That is the profile of a sharply fragmented market, not a clean all-clear signal.

The clearest thesis from the available evidence is straightforward: July 10 should be read as a selective-flow story, not as confirmation that the broader equity tape has regained health. The real risk for beginners is not missing VIC. It is taking one aggregate statistic and applying it to an entire portfolio. The signals worth tracking over the next few sessions are therefore not just whether foreigners stay net buyers, but whether breadth improves and whether the flow starts spreading into other leadership groups.