VN-Index closed July 10 at 1,828.34, down 12.36 points from the previous session. On the surface, that looked like another red day for large caps. But inside the banking sector, the more important shift was not the headline decline. It was the fact that the stocks were already moving to different rhythms.TBTCO

That distinction matters for new investors. In many phases, retail money treats banks as a single block: when credit is strong, the whole sector wins; when rates rise, the whole sector is punished. That shortcut still works at a very high level, but it is no longer enough when bank safety rules are easing one layer of pressure while opening the door to a more demanding review of capital, liquidity, and funding quality.

The core thesis here is straightforward: after the July 10 session, bank stocks should be read as several smaller stories sharing the same tape. The index can still set the mood, but capital and liquidity buffers are becoming the layer that explains which names can decouple first when the market heads into the new week.

A red session did not mean a uniform move

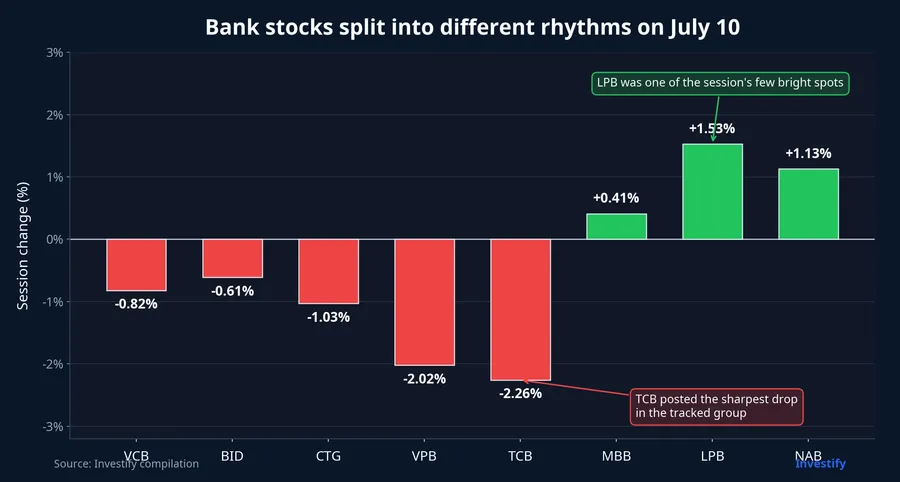

The July 10 numbers already show that split. Within the large listed banks, VCB fell 0.82%, BID lost 0.61%, CTG dropped 1.03%, VPB slid 2.02%, and TCB fell 2.26%. On the other side, MBB still gained 0.41%, LPB rose 1.53%, and NAB added 1.13%.

That may sound incremental, but for anyone who watches the market closely, it is a meaningful difference. A sector is still trading as one block only when most of its names move in the same direction and with broadly similar intensity. That was not the feel of this session. Some banks simply tracked the index lower, some were sold much harder, and some still managed to hold green territory.

At the same time, it would be a mistake to pin the entire gap on a single cause. Short-term profit taking, money coming out of large caps, and the broader market pullback are all plausible explanations. The more useful point is that July 10 showed investors now have reasons to sort banks more carefully instead of assuming the whole sector will react the same way.

Policy is pulling the market in two directions

The first direction is easier near-term relief, and that part is already in effect. Circular 08/2026/TT-NHNN was issued on May 15, 2026 and revised how deposits are counted in the LDR calculation, rather than excluding the entire stock of term deposits from the State Treasury under the previous stricter reading.Chính phủ For new investors, the simple takeaway is that the revised formula softens the liquidity math for some banks, especially those with larger links to Treasury-related deposits.

Then came Circular 25/2026/TT-NHNN, issued on June 22, 2026 and effective from July 1, 2026, which raised the maximum share of short-term funding that can be used for medium- and long-term lending from 30% to 40%. That matters because it gives banks more room in their funding mix instead of forcing them to chase long-term deposits at any cost in the short run.Chính phủ

If those were the only developments, investors could reasonably conclude that pressure on the sector is easing. That conclusion is not wrong, but it only tells half the story. Near-term relief does not erase the bigger question of what happens when the market starts preparing for stricter safety standards further ahead.

That second direction is where the split can persist. The State Bank of Vietnam is still collecting feedback on the draft circular that would replace Circular 22/2019/TT-NHNN, and the draft uses a much broader framework than the familiar LDR discussion. According to Thời báo Tài chính Việt Nam, the focus shifts toward CDR and adds measures such as LEV, LCR, and NSFR in a framework closer to Basel III; procedurally, this remains a draft under consultation, not an issued rule.NHNNTBTCO

That is the part many first-time investors tend to miss. Markets do not wait for the effective date before repricing. Once investors believe banks will soon be judged through a tighter set of metrics, money can begin favoring institutions with thicker capital, safer liquidity profiles, and less dependence on expensive funding.

Capital and liquidity buffers are telling different stories

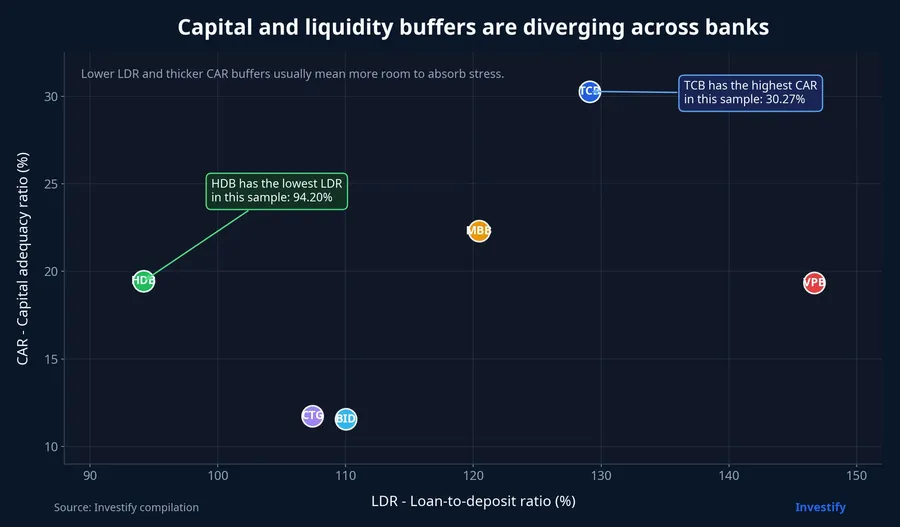

The most revealing part of Investify's first-quarter data is how uneven the starting points already are. On capital, TCB posted a CAR of 30.27% and MBB stood at 22.30%, while BID was at 11.57% and CTG at 11.75%. On that layer alone, TCB and MBB clearly look much better cushioned than the large state-owned banks.

But the second layer, liquidity, tells a different story. HDB reported an LDR of 94.20%, while TCB was at 129.10% and VPB climbed to 146.70%. Put simply, a bank can have strong capital and still face more near-term pressure if loan growth is running far ahead of deposits or if funding costs rise as the market pays closer attention to the quality of its liabilities.

That is why TCB's decline on July 10 should not be read as a one-way judgment on franchise quality. First-quarter data show the bank still has a very strong capital ratio, but its LDR is also high. Once the market evaluates banks through more than one lens, the stock can reflect liquidity pressure or short-term trading flows at the same time, not just a simple verdict of strong versus weak.

The reverse is also true. A stock that rose in the session has not automatically cleared the risk test. MBB and LPB holding green is a useful signal, but it becomes more meaningful only if that pattern repeats over several sessions while the broader market remains unstable. One isolated day shows what the market is testing, not what it has fully decided.

What to watch at the start of the new week

The larger picture is that the market is caught between two forces. One is near-term support from policy changes that are already effective and that reduce immediate pressure on funding and liquidity versus the old framework. The other is the expectation that safety standards will become tighter over time, which encourages investors to distinguish more clearly between banks with stronger buffers and those that may be more exposed.

For the July 13 session, the useful question is not simply whether banks finish green or red. More important are market breadth, whether the names that were sold hardest on July 10 keep drawing heavy selling, and whether banks with thicker capital or lower LDR can continue to separate themselves from the rest. If that happens, the market is moving away from sector-wide trading and toward balance-sheet differentiation.

That leads to a simple conclusion: the right adjustment is not to pick a stock immediately, but to change how the sector is read. After July 10, treating every bank as the same trade is less accurate than it was before. The index will still matter, but the direction of differentiation is already visible, and capital, liquidity, and funding structure are now the three layers worth watching most closely.