Retail investors tend to think a stock trade ends when the order matches. In reality, that is only the visible layer. After the match comes the machinery that books the securities, moves the cash, nets obligations across intermediaries, and contains the damage if one participant fails to perform. That is why the Ministry of Finance's draft replacing Circular 119/2020/TT-BTC is more than a legal update for back-office specialists.KTTC

On July 10, 2026, the VN-Index closed at 1,828.34, down 0.67%. That figure is a useful reminder of how most market commentary works: investors watch prices, turnover, and index levels. But as the market grows, the harder question is whether the infrastructure behind each trade is strong enough to move cash and securities on time, with clear responsibilities and lower systemic risk.

In plain English, the trading screen is the storefront. Custody, clearing, and settlement are the warehouse, the ledger, and the delivery chain behind it. The storefront can look efficient while the system behind it remains messy. If that happens, the cost eventually lands on investors, even if it does not show up in the quote board immediately.

What the draft is actually changing

According to Tạp chí Kinh tế Tài chính, the draft spans 9 chapters, 67 articles, and 6 appendices, covering not only equities but also fund certificates, covered warrants, and listed corporate bonds.KTTC The practical point is that it targets the stretch between order execution and final recognition of assets and obligations across the post-trade system.

On the registration side, the draft revisits cancellation of registration, adjustments to registered securities volume, security code issuance, entitlement processing, and off-system transfer of ownership.KTTC For newer investors, those are not the topics that usually make headlines. But they matter whenever a listed company pays a stock dividend, issues new shares, moves exchanges, delists, or changes the legal attributes of the securities investors hold.

On the custody side, the draft updates rules for depository accounts, collateral-handling accounts, transfers, freezes and unfreezes, and securities borrowing and lending. The common thread is standardization around the KRX system, which has been in operation since May 2025.KTTC Put differently, the market is trying to make its rulebook fit the machinery now running underneath it.

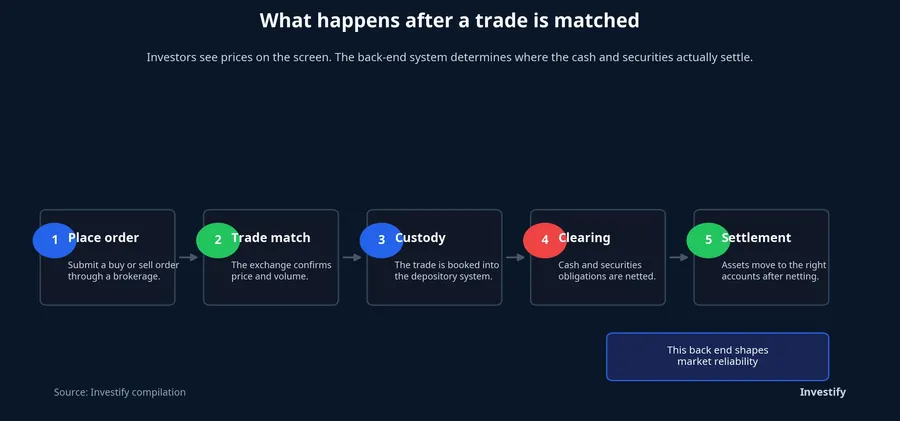

What happens after a trade is matched

Many retail investors mentally compress the process into two steps: place the order and get matched. But final settlement still depends on custody, clearing, and cash movement after that point. If those layers are vague or fragmented, problems may not show up as a dramatic market event right away. Instead, they show up as higher operating friction, greater counterparty risk, and weaker confidence from larger pools of capital.

That is why this topic belongs in a retail-investor conversation. The clearer the post-trade system, the less likely operational errors are to spread, the easier it becomes to process corporate actions consistently, and the more credible the market looks to institutions that care about execution quality rather than just headline performance.

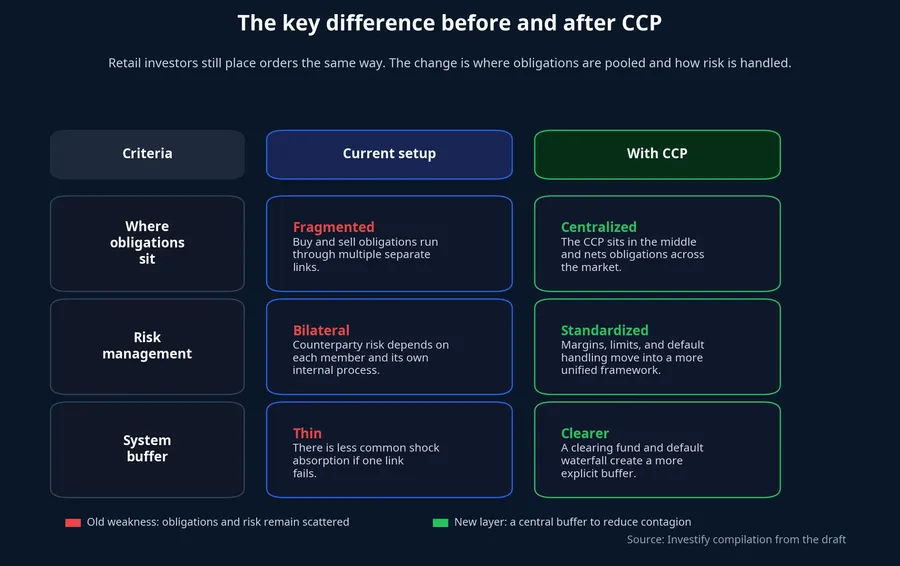

Why the central counterparty piece stands out

The most consequential part of the draft sits in clearing and settlement. Báo Đầu tư reported that the rules before a central counterparty model goes live largely preserve the current framework, while the post-implementation stage would more clearly define the roles of Vietnam Securities Clearing Company and VSDC in clearing, obligation determination, and securities settlement under the new structure.Báo Đầu tư

That sounds abstract until it is translated into investor terms. In the current setup, obligations and counterparty risk are more dispersed across multiple links. A central counterparty adds an institutional node in the middle that pools obligations, standardizes risk controls, and creates a more explicit buffer if one participant fails. Retail investors do not clear trades themselves, but they benefit if the market depends less on a web of bilateral relationships.

Fili, citing the draft, said VSC would conduct multilateral clearing for securities transactions already established on the trading system, based on results supplied by the exchange.Fili Separately, VSDC issued the decision establishing Vietnam Securities Clearing Company as a single-member limited liability company on April 15, 2026.VSD Together, those facts point to more than a paper exercise. The market is also building the organizational scaffolding needed to make the new framework operational.

That still does not mean the impact is immediate. A draft is not the same as a rule in force, and a new clearing model only matters once market participants can test it, use it, and rely on it when something goes wrong. But the direction is increasingly clear: Vietnam is trying to move from a more fragmented post-trade structure toward a more centralized one with stronger risk discipline.

Why foreign capital watches the back end closely

Retail investors often hear the phrase market upgrade and think first about stock prices. Foreign institutions usually start somewhere else. They want to know whether prefunding is required, where assets are held, who sits on the settlement obligation, and what absorbs the first loss if a participant cannot perform. Those are not glamorous questions, but they shape the real cost of participating in a market.

FTSE Russell has already announced that Vietnam will be reclassified from frontier market to secondary emerging market, effective September 21, 2026.LSEG That does not mean every operational bottleneck has been solved. If anything, the closer the effective date gets, the more pressure there is to prove that the post-trade architecture can support stricter institutional requirements.

One detail in the draft matters here. According to Fili, the proposal adds a settlement custodian bank model that would allow a custodian bank to participate in settlement through an agreement with a clearing-member securities company, without becoming a clearing member itself.Fili In practical terms, that addresses a real friction point: foreign investors do not want their assets forced into an operating structure that their custodian banks cannot or will not join directly.

Discipline matters here. The evidence does not justify saying that foreign money will automatically flood in once the rule is finalized. It also does not justify claiming that reclassification alone solves the problem. What the evidence does support is narrower and more useful: the draft is aiming at the exact parts of the market structure that institutional investors usually scrutinize first.

What retail investors should watch next

The first milestone is the final circular itself. Once the final text is issued, the key task is not to memorize every provision but to compare it with the current draft. Did the market keep the core design around VSC, settlement custodian banks, margin accounts, the clearing fund, and default handling? That is the real substance test.

The second milestone is actual CCP implementation. Legal architecture matters, but market impact begins when systems run smoothly, members integrate the process, and edge cases are handled without confusion. That is when post-trade reform stops being a policy story and starts becoming investor reality.

The third milestone is how the market behaves as the FTSE upgrade becomes effective. A label can attract attention. Operational consistency is what helps retain capital. For retail investors, that means the quality of the unseen plumbing may matter more over time than a short burst of optimism on the tape.

The single takeaway is straightforward. This draft is not a reason to chase a stock tomorrow morning. It is a reason to pay attention to the quality of the market you are using. The final circular and the rollout of CCP will show whether Vietnam can turn an infrastructure upgrade into something investors actually feel: cleaner settlement, clearer responsibility, and a market that is easier to trust at scale.