BCG shareholders are facing a transition that many first-time investors tend to misread. When HOSE forces Bamboo Capital off the exchange on July 15, 2026, the problem is not just that the ticker loses its listing. The more serious shift is that the risk profile changes: from a stock that can still fall on-screen to an asset with weak liquidity and limited information for the market to price properly.VietnamNet

That is why a delisting is very different from a sell-off or even a margin restriction. As long as a stock is still trading, investors at least have a market in which to react. Once it has been frozen for too long and then removed from HOSE, ownership may remain intact, but the ability to turn that ownership into cash becomes far less predictable.

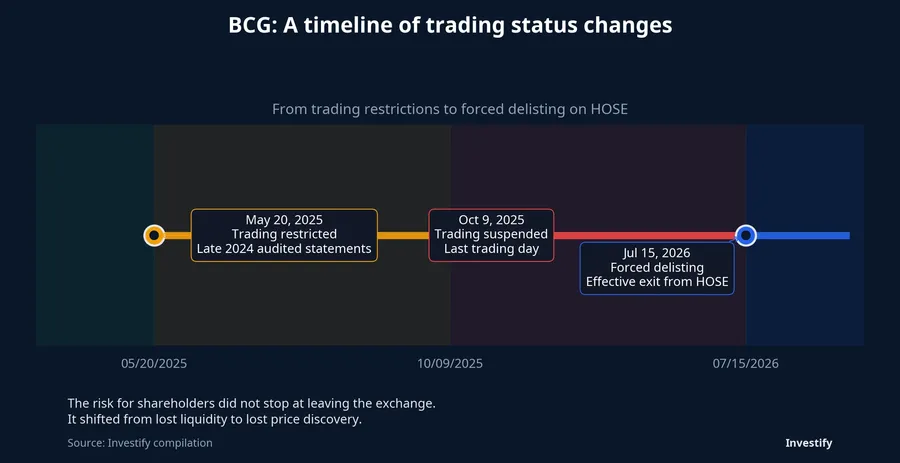

What just happened to BCG

According to VietnamNet, HOSE announced the forced delisting of more than 880.21 million BCG shares, equivalent to more than VND 8,802 billion in par value. The delisting takes effect on July 15, 2026, while the last trading day was recorded as October 9, 2025.VietnamNet

On the surface, that looks like an exchange-level disciplinary decision. For shareholders, however, the real impact lies in the chain of consequences that follows. Internal data shows that from after October 9, 2025 through July 10, 2026, BCG stayed at VND 2,530 per share and matched volume was zero. That tells investors something simple but important: the ticker may still sit in an account, but the market has almost stopped functioning as a venue for actual trading.

This is why BCG should not be read as a one-day shock. It is a process that moved from restricted trading to suspension and now to forced delisting. Each step does more than damage the company's market image. It steadily reduces a shareholder's ability to exit the position.

Why HOSE went as far as a forced delisting

The direct trigger was not price action but disclosure failure. VietnamNet reported that Bamboo Capital had not submitted and disclosed a range of required financial statements, including audited statements for 2024 and 2025, reviewed semiannual statements for 2025, quarterly statements for 2025 and the first-quarter 2026 report.VietnamNet

What the report does not state bluntly enough, but investors need to understand, is that the stock market runs on a shared data base. Financial statements are where shareholders check assets, debt, cash flow and earnings power. When that reporting chain breaks over multiple periods, the gap is not just a few missing PDF files. The market loses the foundation it uses for valuation.

Circular 96 requires listed companies to publish audited annual financial statements within no more than 90 days after the end of the fiscal year. Reviewed semiannual statements are generally due within 45 days, while a parent company with consolidated statements can take up to 60 days.LuatVietnam

For a stock that has missed disclosure across that many reporting windows, the core risk is no longer whether the market feels bullish or bearish on the business. The real risk is that the market loses the ability to verify. A stock can still have projects, assets and a legal entity. But if investors do not have an updated set of numbers to test against, any future price becomes closer to a guess than a valuation.

Delisting does not mean shareholders are wiped out

This is where retail investors tend to panic, and it is also where misunderstanding is most common. A delisting does not mean the company disappears overnight, and it certainly does not mean shareholders automatically lose ownership. Shares remain shares. What changes is the trading venue, the level of transparency and the odds of finding a buyer when investors want to sell.

If the company still qualifies as a public company, a stock that is forcibly delisted must still register for trading on UPCoM under the current rules. Under Article 133 of Decree 155, the processing of that trading registration is carried out within 07 working days from the effective delisting date.Government

But this is exactly where many investors jump into a second misconception: that a move to UPCoM solves the problem. It does not. UPCoM only creates the possibility of a centralized trading venue instead of a complete freeze. It does not guarantee that liquidity will return quickly, and it does not guarantee that the market will accept the old reference price.

Put differently, HOSE is the story of listing status. UPCoM, if it happens, is only the story of where the stock may trade next. The most important question remains unchanged: can the company close the information gap quickly enough for the market to price it again with some confidence.

What is the real risk for investors still holding BCG

The first risk is liquidity. When a stock has been suspended for a long period, the old screen price loses much of the meaning it had during normal trading. The VND 2,530 level currently recorded in the data is not a promise that investors will be able to sell there if trading resumes. If the backlog of sell orders outweighs buying demand, the stock can be repriced very differently.

The second risk is the information gap. If Bamboo Capital releases the missing financial statements, the market at least gets a basis for reassessing assets, debt and cash flow. If disclosure remains delayed, the stock could reappear on a new trading platform and still remain extremely difficult to value. In that kind of setting, markets usually apply a heavy discount for uncertainty rather than waiting for fully confirmed bad news.

The third risk is a false sense of ownership. Many investors reassure themselves that nothing fatal has happened because the stock still appears in the account. That view misses a central feature of capital markets: a financial asset only carries its full economic meaning when ownership, price discovery and tradability all work together. Once the last two weaken, "still holding the shares" is not the same thing as preserving value.

What shareholders should watch after July 15

The first thing to watch is the next set of notices from HOSE, HNX, VSDC and Bamboo Capital itself on the stock's technical path forward. The practical question is not whether BCG still appears in an account. It is whether the stock moves to a new trading mechanism, when that might happen and whether new restrictions would still apply.

The second point is the release schedule for the missing financial statements. This is the bottleneck that determines whether the market can build a fresh valuation case. If disclosure resumes, shareholders get a way to reassess the company using current numbers. If disclosure remains broken, any hope of liquidity returning will weaken very quickly.

The third point is the market's behavior if trading does resume. Investors should not assume that a return to trading automatically means healthy liquidity. The real indicators are matched volume, price movement and the continuity of actual transactions in the first sessions back. A stock can be "trading again" in a technical sense while still being very hard to buy or sell in practice.

Bottom line: this is no longer mainly about price

The clearest thesis here is that the risk for BCG shareholders has moved away from day-to-day price volatility and toward liquidity and disclosure quality. When the stock was still matching, investors could respond to bad news through trading. After suspension and delisting, the old price board matters less than the new trading path and the speed at which the company restores disclosure discipline.

For the next one to two weeks, the watch list should stay narrow: BCG's new trading-registration status, the release of the missing financial statements and actual liquidity if the stock returns to a market venue. Until those three links are restored, leaving HOSE is only the opening stage of the risk story, not the end of it.