BSR rose nearly 5% in a session when the VN-Index fell 0.70%. That is not the kind of move investors should explain away with a simple “oil up, oil stocks up” narrative. In BSR's case, the market is reacting to something more concrete: first-half earnings have already run far ahead of the company's full-year plan, forcing investors to rethink what the stock should be worth in the near term.

That distinction matters, especially for newer investors. Oil and gas is not one story. Upstream names trade on crude prices, service names trade on drilling activity and capital spending, while a refiner like BSR lives and dies by the spread between what it pays for crude and what it can charge for refined products. Miss that mechanism, and it becomes very easy to chase a rising stock for the wrong reason.

What the market is reacting to

The first anchor is BSR's estimated first-half performance. The company said output reached 4.05 million tons, up 5.5% from a year earlier. Consolidated revenue came in at VND 100,922 billion, up 47%, while consolidated net profit reached VND 12,636 billion, almost seven times the year-ago level.CafeF

For the second quarter alone, BSR posted more than VND 55,000 billion in revenue and VND 4,097 billion in net profit, up more than 384% year on year.CafeF The key point is not just that growth was strong. What matters is that the story has moved from analyst expectation to a company-backed earnings estimate. Once the market shifts from “this may happen” to “this is already showing up in the numbers,” valuation usually adjusts fast.

That is exactly what the July 9 session looked like. While the broader index slipped, BSR still closed at VND 26,350 per share, up 4.98%, on volume of more than 21.2 million shares. A move like that usually says two things at once: fresh data was strong enough to attract stock-specific buying, and investors were willing to look past market weakness to pay up for a higher earnings path.

That does not mean every point of the rally came from one single driver. BSR may also be benefiting from better sentiment toward oil-related names, from investors hunting for standout earnings stories, and from expectations around refining margins. But among those explanations, the earnings data is the one with the strongest direct evidence behind it.

The gap between plan and reality is too large to ignore

If you only look at growth rates, BSR looks impressive. That still does not explain why the market reacted this sharply. The answer sits in the gap between management's full-year plan and what the company has already delivered after six months. First-half revenue has reached about 65% of the annual target, while net profit is already more than 5.8 times the company's full-year profit goal.CafeF

The 2026 plan the market is now comparing against called for consolidated revenue of more than VND 154,140 billion and net profit of VND 2,162 billion.CafeF In plain terms, BSR has already generated far more profit in the first half than the company itself had penciled in for the full year. For a stock that trades on expectations, that is the kind of information the market has to reprice.

Seen that way, the rally makes sense. When a plan proves too conservative or real operating conditions turn out much better than management assumed, investors immediately start resetting the base case. The core question becomes simple: if first-half earnings were this strong, where does full-year profit actually land. That reset in expectations is the main driver of the stock move, not a one-day swing in crude.

This is also where newer investors need to slow down. Beating an annual target does not mean a stock will keep rising in a straight line. Share prices move ahead of reported numbers. Once the market starts paying up early, the margin for error becomes thinner for anyone buying later, because the next quarter has to clear a higher bar than it did before.

Refining margins matter more than crude alone

BSR's business model is often misunderstood. The company does not benefit from crude prices in the same way many retail investors assume. A refinery makes money from the refining margin, the spread between crude input costs and selling prices for gasoline, diesel and jet fuel. When that spread widens, earnings can jump quickly. When it narrows, profits can compress just as quickly even if revenue stays large.

That is why the right question after July 9 is not whether Brent goes up or down in the next session. The right question is whether refined product prices can hold up better than crude, and whether BSR's refining margin can stay supportive in the second half. That is the difference between reading the tape and reading the business model.

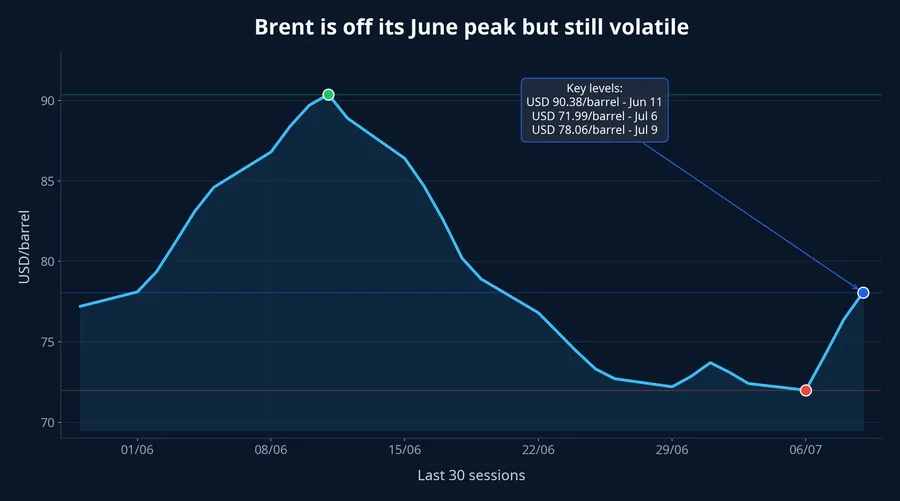

Recent Brent moves show that the input side is still volatile. Brent closed at USD 78.06 per barrel on July 9, above the USD 71.99 per barrel area seen on July 6, but still well below the USD 90.38 per barrel peak recorded on June 11. The market has backed away from the June high, but the input environment is nowhere near stable yet.

That volatility cuts both ways. On one hand, crude staying below the June peak can ease working-capital pressure and input costs. On the other, if product prices fall faster than crude, the margin that refiners keep on each unit sold will shrink. Put simply, BSR does not need crude to be as high as possible. It needs a price structure that leaves enough room between feedstock and finished products.

That is also why second-quarter earnings should not be projected mechanically into the second half. The quarter tells us BSR executed well in a favorable window. Whether that window remains open is a different question, and the answer depends far more on refining spreads than on any single Brent price point.

Dung Quat is where expectations become real earnings

Price is only part of the story. Execution matters just as much. BSR operates the Dung Quat refinery, Vietnam's first refinery, with designed capacity of about 6.5 million tons of crude per year and supply equivalent to roughly 30% of domestic fuel demand.CafeF That scale gives the company a unique position, but it also means investors have to pay close attention to operational discipline.

VietnamBiz, citing BSR, said the company will keep monitoring market developments, supply conditions and oil prices, while maintaining Dung Quat in safe, stable and continuous operation at optimal capacity and preparing for its sixth major maintenance cycle.VietnamBiz That detail is not a footnote. A refinery only turns a supportive market backdrop into real earnings if the plant runs smoothly and product offtake remains uninterrupted.

That leaves BSR facing a two-layer test in the second half. First, can refining margins remain supportive. Second, can Dung Quat stay at optimal operating conditions while the company prepares for the next maintenance cycle. Only if both pieces hold up does the case for sustained high earnings remain intact.

The cleanest way to read BSR after July 9

The clearest thesis from the available evidence is that the market is repricing BSR because reported profitability has already outstripped the company's annual plan by a wide margin. This is not a purely emotional move, and it is not a story built on hope alone. It is anchored in first-half numbers strong enough to force investors to rethink the earnings base.

What the market is paying extra for from here, however, is no longer about the past. It is about durability in the second half. If refining margins stay favorable and Dung Quat keeps running smoothly, the current move has a foundation that can extend beyond a one-session reaction. If margins tighten quickly or operations interrupt output, part of that forward-loaded optimism will have to come back out of the stock.

For newer investors, the useful lesson is not whether BSR will close green or red in the next session. The lesson is how the market values a refiner. Sometimes the tape is reacting to crude on the day. At other times, it is reacting to something much more specific: real earnings have already moved ahead of plan, and the only question left is whether that profit level can last.