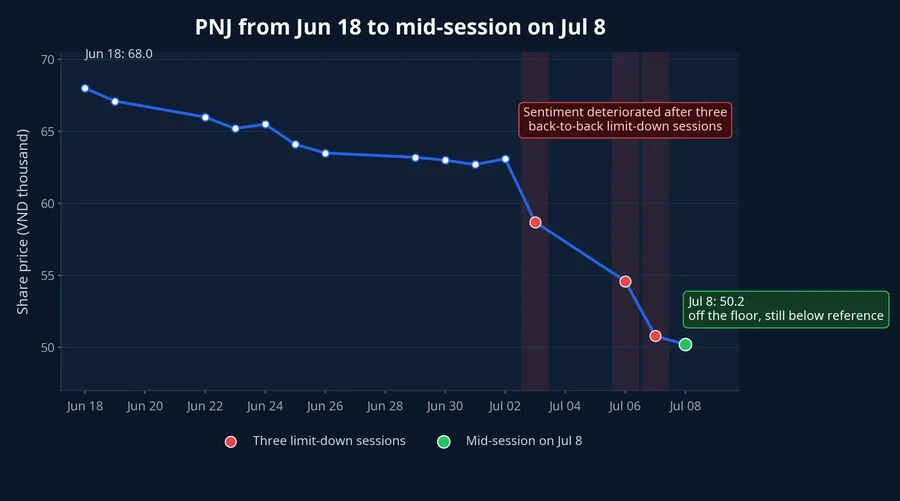

By mid-session on July 8, the VN-Index was still up around 1,851.68 points, while PNJ traded near VND 50,200 a share after coming off the floor. The screen was sending two messages at once. The broader market was not breaking down, but PNJ was still going through a credibility shock that had clearly not been resolved.

That distinction matters, especially for newer investors who tend to read any rebound as proof that the danger has passed. In reality, a mid-session recovery only shows that buyers were willing to absorb low-price selling at that moment. It does not prove that the market is ready to restore the valuation PNJ enjoyed before the P-Lab shock.

What the tape is actually saying

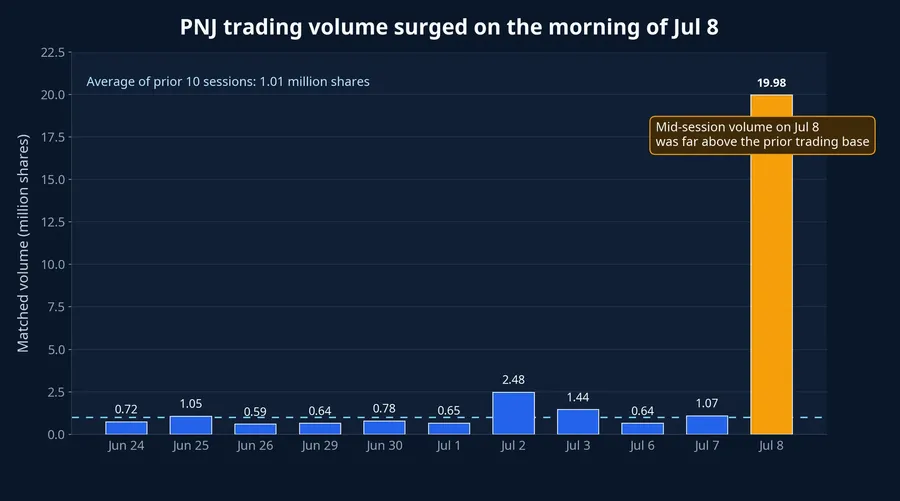

VietnamBiz reported that by 9:30 a.m. on July 8, PNJ was trading near VND 49,000, down 3.5% from the reference price, with about 13.4 million shares matched and trading value above VND 640 billion.VietnamBiz Those numbers matter because they show real money came in, yet the stock still could not return to a normal trading range. Buyers were present, but conviction was still thin.

The short-term price path explains why sentiment remained so fragile. PNJ closed at VND 58,700 on July 3, fell to VND 54,600 on July 6, and dropped again to VND 50,800 on July 7 before hovering near VND 50,200 by mid-session on July 8. Three straight limit-down sessions do more than erase market value. They create a psychological overhang that a single intraday bounce rarely clears.

Set that backdrop against mid-session volume of roughly 19.98 million shares on July 8 and the picture becomes clearer. There was genuine demand, but much of it still looked like a stress test of whether the market could digest forced selling. For investors, that is the difference between a technical rebound and a completed re-rating.

Why the risk is bigger than one price move

The more important issue is the quality of the rebound. VietnamBiz said foreign investors were still net sellers by nearly VND 200 billion in PNJ during the morning session on July 8.VietnamBiz When overseas money continues to leave while the stock is climbing off the floor, the message is fairly direct: buyers have appeared, but not every investor group sees the stock as safer again.

The easiest way to think about it is this. A store can suddenly see heavy foot traffic without having fully repaired its reputation; some people may simply be checking, returning products, or reacting to the event itself. Stocks behave the same way. A surge in liquidity does not automatically mean trust has returned.

That is why the market is not focused only on whether PNJ can avoid another down session. The larger issue is how investors reprice something less visible: the durability of the brand and the credibility of internal controls after the P-Lab incident. Once the debate shifts from next quarter's earnings to longer-lasting trust, recovery usually takes more time than a price bounce.

What new questions the P-Lab incident has opened

PNJ said P-Lab is a wholly owned subsidiary with charter capital of VND 10 billion and operates as an independent legal entity.VietnamBiz The company also disclosed that it had formed a special monitoring team, including two independent members, to review the situation after the incident.Tiền Phong Those are necessary steps, but they do not erase the broader question of how the risk-control system worked before the event.

What current disclosures do show is that PNJ's core business has not come to a halt. But the market is more interested in the second-order effects: whether customers delay purchases, whether buyback or exchange activity pressures liquidity, and whether the brand will need much longer to earn back its previous valuation. None of those questions can be answered by one session off the floor.

For experienced investors, this is the point where the market separates "the company is still selling products" from "the market is still willing to pay a premium multiple for that company." For newer investors, the clean takeaway is that a stock price does not only reflect next quarter's revenue. It also reflects the discount investors apply to governance risk, brand risk, and the quality of management's response.

Why both broker notes are centered on trust

ACBS, citing the company, said store traffic jumped in the first few days after the news broke, then gradually eased and was close to normal again. The note also said loose diamonds and diamond jewelry account for around 30% of retail sales, with loose diamonds alone contributing roughly 10%.ACBS In plain terms, ACBS was telling the market that any damage is unlikely to hit every part of PNJ evenly. The pressure would be concentrated in the segments most sensitive to customer confidence.

What stands out is that ACBS did not leap to the conclusion that revenue would immediately deteriorate sharply. Its emphasis was on liquidity pressure from possible diamond resales and on the challenge of restoring customer trust. That distinction matters because it avoids turning one event into a fully formed earnings narrative before the evidence is there.

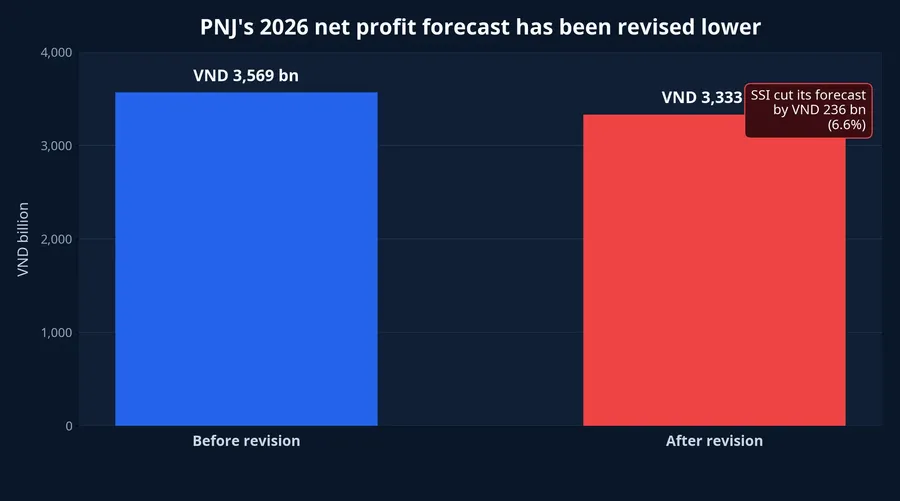

SSI Research took a similar line when it cut PNJ's 2026 net profit forecast to VND 3,333 billion from VND 3,569 billion.An ninh Thủ đô That revision is meaningful, but it is not the kind of slash that implies the business has collapsed. The real message in the report is that uncertainty around brand reputation, corporate governance, and internal controls has gone up.

When different research notes converge on trust as the core issue, investors should read that as a sign the market has moved beyond pure trading mechanics. Price can bounce because supply and demand briefly rebalance. A more durable re-rating only happens when the trust discount starts to shrink.

How to read the July 8 session from here

The morning of July 8 is better viewed as the market's first test of PNJ after three straight limit-down sessions, not as a final verdict. The constructive part is that the stock did not stay pinned at the floor for the entire session. The unresolved part is bigger: how long foreign selling lasts, whether liquidity holds once bottom-fishing fades, and how quickly the company can show that customer confidence has not been damaged for longer than a few days.

So the most defensible reading right now is neither "the risk is over" nor "the business is permanently broken." The evidence supports a narrower conclusion. PNJ has shown its first sign that the sell-off can be absorbed, but the market is still applying a steep discount for trust-related risk. Until capital flows, customer behavior, and company disclosures all improve together, moving off the floor on July 8 remains an early signal of stabilization rather than the end of the repricing process.