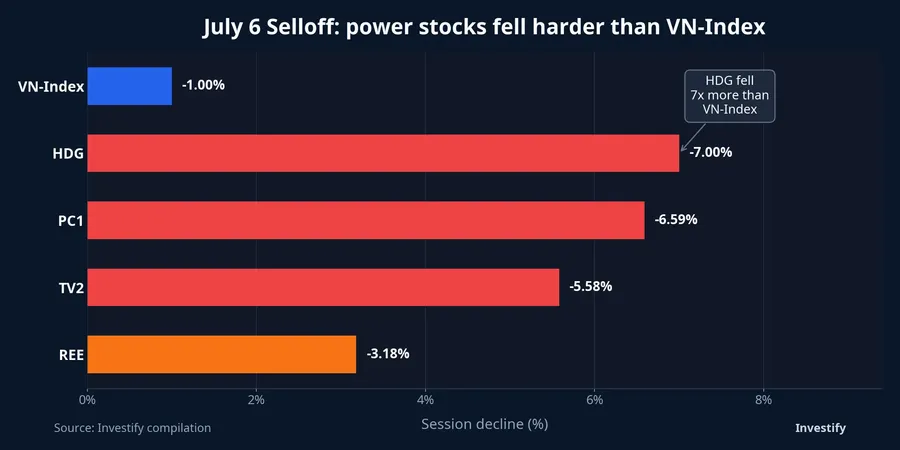

July 6 offered a sharp lesson for new investors: the tape does not wait for investigators to name every company before repricing a sector. VN-Index closed at 1,843.50, down 1.00%, yet HDG fell 7.00%, PC1 lost 6.59%, TV2 dropped 5.58% and REE slipped 3.18%. On the surface, that looks like an emotional selloff. But who usually takes the bigger hit in sessions like this? It is often the investor who fails to separate direct legal exposure from a broader sector discount.

What matters here is the chain effect embedded in the story. Once a legal case touches power infrastructure, investors do not only reprice the company explicitly mentioned. They also scan consultants, contractors, generators, bond obligations and margin-sensitive names sitting close to the same narrative. The core thesis is straightforward: the July 6 move looks mainly like an expansion of risk discounting across the power complex, not proof that every listed power name faces the same cash flow shock.

Legal headlines widened the discount zone

On July 2, 2026, Vietstock, citing Vietnam's Ministry of Public Security, reported that investigators had prosecuted 47 defendants in a case tied to the 500kV Line 3 project involving the National Power Transmission Corporation, PC1 and other companies in the power sector. The same report said the case had originally been opened on April 29, 2026 with five groups of charges.Vietstock

The market immediately focused on scope. Vietstock also reported that, as of that disclosure, defendants had been prosecuted at 13 companies and units, including the National Power Transmission Corporation, power project management boards, PC1 and several power engineering consultants.Vietstock Once the list starts to look like a chain rather than a single node, investors do not wait for a final legal conclusion. They reduce the price they are willing to pay across the cluster of stocks that may be pulled into the same zone of uncertainty.

That is the point many first-time investors miss. Share prices do not only reflect confirmed events. They also price the cost of not knowing. A fund manager looking at the power group on July 6 would have had to ask several immediate questions: which contracts may be reviewed, which projects may slow down, which cash flows could be delayed, and which companies depend more heavily on borrowed capital or market funding. When those answers are missing, discount rates tend to rise.

Not every stock carries the same kind of risk

The biggest mistake after a deep red session is to force every stock in a sector into one conclusion. For PC1 and TV2, the perceived link was clearly tighter because the reporting around the case touched the engineering and contracting chain directly. Vietstock said Power Engineering Consulting JSC 2 had disclosed that its chairman and chief accountant were prosecuted in developments related to the same case.Vietstock For companies sitting in that exact segment of the value chain, the market typically demands a wider margin of safety because legal risk can spill into project timing and funding costs.

PC1 also faces a second layer of pressure from its bond issue. On July 4, 2026, Vietstock reported that the State Securities Commission required PC1 to repurchase a VND 900 billion bond lot after proceeds were used for the wrong purpose. According to the report, VND 90 billion out of the total was used to repay a short-term VietinBank loan, which did not match the stated use of proceeds.Vietstock This is where the real concern sits: when a stock is hit by a sector-wide legal shock and a capital-obligation problem at the same time, the market stops valuing it as a plain power story.

HDG and REE need to be read differently. The source article does not show either company as directly implicated in the case. So saying that HDG or REE is legally entangled would go beyond the evidence. A more defensible reading is that investors also sold companies with power assets or power-linked investment narratives because the boundaries of the fallout were still unclear. In other words, this was a sentiment discount and a sector discount, not a legal conclusion applied evenly across every red ticker on the screen.

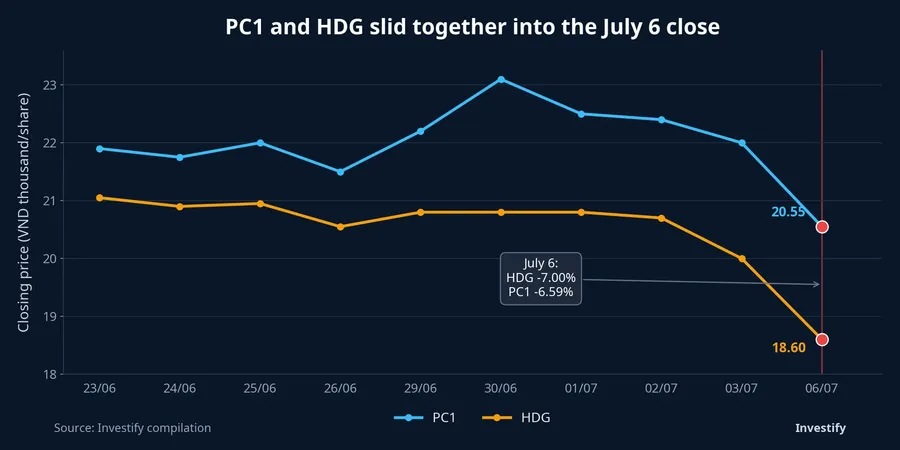

The counterfactual matters too. HDG's floor move may also reflect technical pressure after an already weak price pattern, while REE's smaller decline suggests the market was still differentiating, at least partially, on asset quality and corporate structure. The evidence available today supports the idea that investors were first dumping the names perceived to sit closest to the risk zone, rather than declaring that every power company shares the same problem.

Why margin can accelerate the spillover

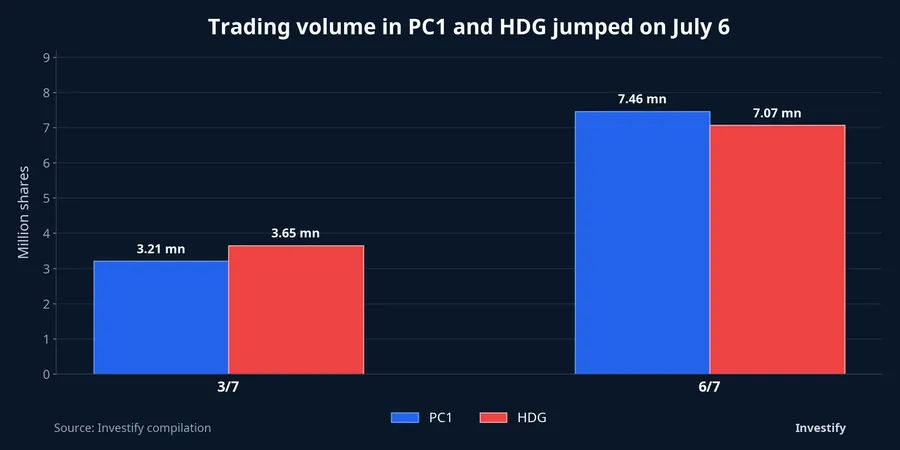

Bad news is only the spark. The mechanism that spreads the fire often sits inside leveraged accounts. On July 6, PC1 traded 7.46 million shares, sharply above the 3.21 million shares seen on July 3. HDG traded 7.07 million shares, nearly double the 3.65 million shares from the prior session. When turnover surges while prices are falling hard, the odds of forced or defensive de-risking rise well above those of a routine correction.

That still does not prove a broad margin call event. But it does suggest that the sell side was no longer limited to investors choosing to cut losses on their own terms. In practice, when a stock drops hard while sitting close to an unresolved legal story, many accounts will proactively trim other names in the same sector just to preserve room on the balance sheet. That risk-management behavior is why spillover selling often becomes stronger than the original headline in the first few trading hours.

Put simply, markets hate blind spots. When investors do not yet know where the boundary lies, capital usually exits the area under suspicion first and sorts out the details later. That is why July 6 should be read as a stress test for market liquidity and risk tolerance, not as a final verdict on the entire power sector.

Three signals to track next

Breadth of selling inside the power group. If PC1 and TV2 keep falling hard while names not directly mentioned start to stabilize, the market is separating direct exposure from guilt by association. If the whole group keeps sliding together, the sector discount is still open.

Volume relative to price. Another leg down with lighter turnover would suggest emotional selling is starting to exhaust itself. A continued decline with rising volume would imply holders still want out before repricing is complete.

Company-specific disclosures. For PC1, the market needs to watch how the VND 900 billion bond issue is handled and how the board is reorganized ahead of the extraordinary shareholder meeting scheduled for July 24, 2026.Vietstock For the other names, the key question is whether they can publish enough concrete information to pull themselves out of the shared discount bucket.

The evidence so far points to a market that is widening the risk discount across the power chain, not confirming a uniform earnings or cash flow collapse across the sector. That view only changes if new information shows the legal scope is broader than currently understood, or if capital stress starts surfacing across more companies. As of July 6, 2026, the most important line to watch is not which stock is redder. It is how quickly the market redraws the boundary between companies directly exposed to the case and companies being sold mainly on association.