For beginner investors in Vietnam, the usual comparison between open-end funds and self-picked stocks has often been too simple: which one delivers the higher return. From July 1, 2026, that shortcut becomes less useful. Under Decree 253/2026/ND-CP, individual investors may be exempt from personal income tax when selling open-end fund units if the units being sold have been held for at least 2 years.LuatVietnam For anyone investing with a multi-year horizon, that changes the discussion at the level that matters most: net returns after frictions.

The first thing to keep straight is what this reform does not do. It does not turn open-end funds into the universally superior choice. What it does is narrower and more useful: it lowers the exit cost for investors willing to hold long enough. For beginners who do not yet have a demonstrated edge in stock selection, that cost advantage deserves more attention than it used to.

What exactly changed

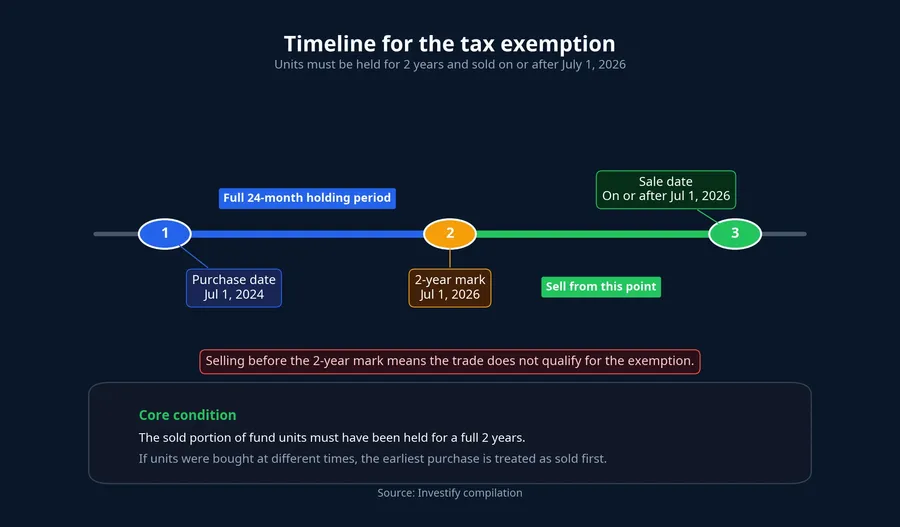

The key condition is the holding period. An open-end fund created under Vietnam's securities law qualifies for tax exemption on transfer income if, at the time of sale, the sold units have been held for at least 2 years from the purchase date.LuatVietnam If an investor bought units at different times, the earliest purchases are treated as sold first. That detail matters because eligibility is determined lot by lot, not at the portfolio level.LuatVietnam

In practical terms, the tax break is not automatic just because someone owns an open-end fund. Monthly savers still need to understand that their holdings accumulate in separate lots, each with its own holding clock. The exemption only applies to the portion that has actually reached the 2-year mark.

Stocks remain on a different tax track. Under Article 54 of the same decree, personal income tax on securities transfers is still calculated at 0.1% of the transfer value for each sale.Xây dựng Chính sách The important part is that the tax is based on sale value, not on whether the investor made a profit. A sale to lock in gains, cut losses or simply rotate into another stock still triggers the tax.

That difference looks small when viewed as a single transaction. It looks larger when placed inside a real long-term investing habit. Self-directed stock investors often rebalance more often than they expected, especially in their first years in the market. Open-end funds, by contrast, rebalance internally at the fund level. The individual investor is not the one selling each security and therefore is not the one repeatedly triggering a transfer tax on each internal adjustment.

The cost advantage is real, but it does not create returns by itself

This is where the new rule is easiest to oversell. A tax exemption does not guarantee that an open-end fund will outperform a self-directed stock portfolio. What it does mean is that if two strategies produce similar gross results over time, the fund route may leave more of that return in the investor's pocket because one layer of exit cost has been reduced or removed.

That matters most for investors without a stable process yet. Many beginners do not lose money because of one disastrous stock pick. They lose because they keep changing their minds: selling when screens turn red, chasing a hot theme, then rotating again a few weeks later. In that pattern, the 0.1% tax is not the biggest cost, but it is still added to each sale and gradually erodes realized performance over time.Xây dựng Chính sách

Open-end funds, on the other hand, reward a very specific behavior: staying invested long enough. That is why the tax reform fits the product structure so well. The investor delegates security selection, portfolio weighting and rebalancing to a professional team. In exchange, the investor accepts a longer time horizon and less day-to-day reaction to market noise. When the tax code explicitly rewards patience, that model becomes more compelling for beginners.

Still, the tax break does not erase the trade-offs. Open-end funds still charge management fees. Their results still depend on portfolio construction, manager discipline and whether the strategy actually matches the investor's goals. A fund can be tax-efficient at the exit and still be a poor fit if fees are high, the portfolio is misaligned, or long-term performance does not justify the fee burden.

In other words, tax is one variable that improves the equation. It does not replace product due diligence. Investors who hear “tax-free” and stop their analysis there are still skipping the hard questions: what strategy they are funding, what volatility they are accepting and what kind of outcome they should reasonably expect.

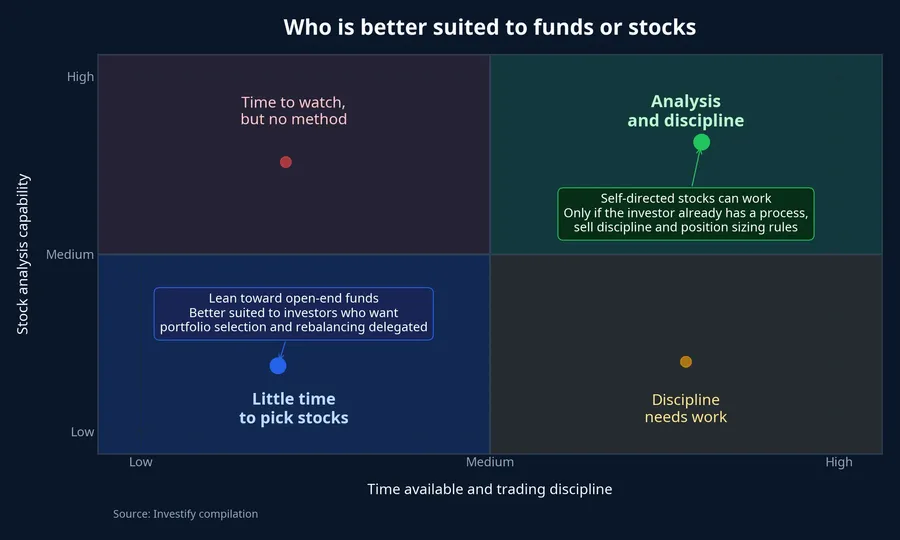

When self-directed stocks can still be the better route

Open-end funds are not the right answer for everyone. Investors who have time to read filings, understand businesses, follow industry developments and sell when the original thesis changes still retain an advantage that funds cannot replicate. That advantage is control: which names to own, where to add weight, when to hold cash and when to concentrate on a narrow set of businesses they understand deeply.

For that group, the 0.1% transfer tax can be viewed as the price of direct control.Xây dựng Chính sách If an investor genuinely has better-than-average stock selection skill, or can hold a small number of high-quality businesses for years, the tax may not be the decisive factor.

But that “if” is doing a lot of work. The market backdrop on July 6 offered a useful reminder: the VN-Index closed at 1,843.50, down 18.58 points, with 282 decliners. One down session says little about a full-year trend, but it does show how much harder discipline becomes when a real portfolio is under pressure. Beginners often overestimate their tolerance for volatility before they experience it.

That is why the difference between funds and stocks is not only about products. It is also about behavior. One route suits investors who want investing to become a structured habit. The other suits investors who want, and are prepared, to take responsibility for each individual buy and sell decision.

How beginners should rethink the long-term decision

The tax change that took effect on July 1, 2026 does not produce a universal answer. What it does is strengthen one answer for one specific group: new investors with a long horizon, no clear edge in picking stocks and no desire to turn investing into a part-time job.LuatVietnam

If that description fits, open-end funds are no longer just the option that feels simpler. They now come with a concrete, measurable cost advantage tied directly to long holding periods. That does not guarantee better performance than self-directed stocks, but it does reduce one kind of leakage that beginners often suffer from: trading too much before they have developed an information edge or a repeatable method.

The practical approach is to read an open-end fund as a full investment product, not as a tax slogan. Look at the fund's mandate, the assets it is allowed to own, its management fee, how it reports NAV, how it behaved in weak markets and whether it imposes an early-exit fee. The right product is the one that helps the investor stay with a plan long enough for the tax advantage to matter, not the one with the most attractive headline.

The core conclusion is straightforward. The tax exemption does not make open-end funds automatically better than stocks. But for long-term beginners who have not yet proved they can pick stocks with discipline, it makes open-end funds a more credible option than they were before. The signals worth watching from here are fund-level performance quality, fee levels and whether investors actually maintain the holding discipline required for the benefit to work.