Domestic coffee prices in Vietnam softened slightly at the end of the week, but that is not the core story. A July 4 survey still showed buying prices in the Central Highlands at VND 92,300-93,000 per kilogram, well above the levels seen in the first half of June.Vietnambiz If you only focus on the last red session, it is easy to think the rally has failed. In commodities, and especially in coffee, that is usually the wrong lens. What prices are responding to is a deeper concern around harvest timing, bean quality, and when physical supply can actually reach the market.

In simple terms, equities tend to trade on expectations for corporate earnings, while coffee trades on expectations for an entire crop cycle. Once those expectations shift, prices can move well ahead of what is visible in the fields. The right question is not whether coffee rose or fell on a single day. The right question is what the market is looking ahead to.

Where the move began

The first important marker came on June 30. Data cited by Báo Chính phủ from the Mercantile Exchange of Vietnam showed arabica rising 6.7% to USD 6,535 per ton, while robusta gained 2.6% to USD 3,658 per ton.Báo Chính phủ At that point, coffee had advanced in 11 of the previous 15 sessions. That matters because it signals a sustained repricing, not a one-off reaction to a weather headline.

By July 1, the move had clearly spilled over from futures markets into Vietnam's domestic market. Vietnambiz reported that local coffee prices rose by VND 1,500-1,600 per kilogram, lifting the buying range to VND 91,600-92,000 per kilogram, while July robusta futures climbed 2.94% to USD 3,958 per ton.Vietnambiz Internal market data also show world coffee prices rising from 240.90 US cents per pound on June 9 to 309.90 US cents per pound on July 1, a gain of about 28.6% in less than a month of trading. That is the market pricing a tighter delivery window, not merely reacting to daily noise.

The key point is that prices did not return to where they started after the early-July pullback. On July 4, July robusta futures fell 1.39% to USD 3,903 per ton, while July arabica dropped 2.67% to 315.65 US cents per pound.VOV Even so, internal data still put arabica at 301.20 US cents per pound on July 4, roughly 25.0% above the June 9 level. That makes the late-week decline look more like profit taking than a confirmed reversal.

What the market is really buying is time

Why can weather in Brazil push prices this far? Because Brazil is the world's largest coffee producer, and late June sits right in the middle of peak arabica harvest season. Báo Chính phủ, citing Procafé, said about 60-65% of Brazil's arabica crop was still being harvested at that stage.Báo Chính phủ That is the most sensitive window for the market. Even a short disruption in picking or drying can change when beans are ready for shipment.

During the week ending June 28, rainfall in Minas Gerais reached 31.3 mm, nearly 20 times the historical average for the same period.Báo Chính phủ Heavy rain does more than slow harvesting. It raises the risk of cherries falling, stretches drying time, and can hurt bean quality. In coffee, the gap between having crop volume on paper and having export-grade beans ready to deliver is wide. That is why the market is no longer asking only whether supply exists. It is asking whether qualified supply can reach buyers on time.

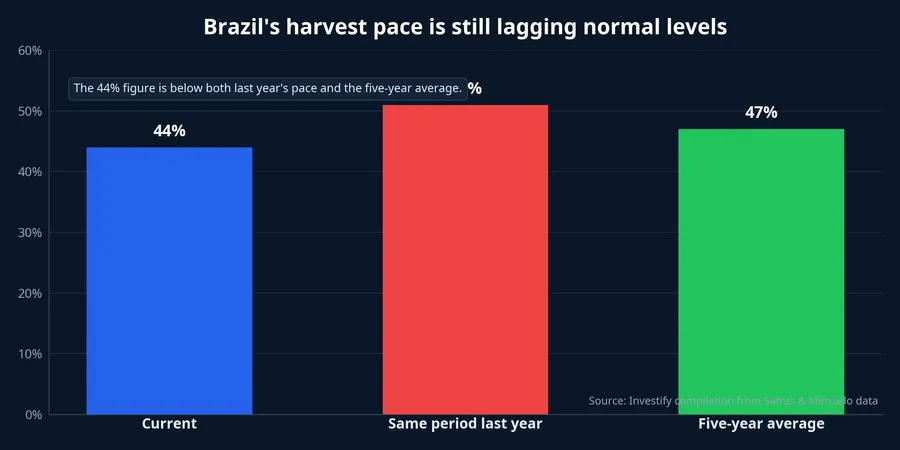

Safras & Mercado estimated Brazil's harvest progress at just 44% of expected output, 7 percentage points below the same period last year and around 3 percentage points below the five-year average.Báo Chính phủ This is the part many first-time investors miss: coffee prices do not need a full-blown supply crisis to rally. A slower flow of beans to market during a sensitive period is often enough.

Another data point supports the same reading. Cocoa Intel said Cooxupé had harvested only 24.9% of member output as of June 28, down from 31.4% a year earlier.Cocoa Intel When two separate sources both point to slower progress, the market has reason to price the risk around timing rather than annual production alone. In other words, the issue is not just how much coffee Brazil will produce. It is how quickly the market can access the part of that crop that meets delivery standards.

Vietnam is part of the story too

Brazil is only one side of the equation. On July 2, Reuters, cited by The Guardian, reported that robusta hit a five-month high of USD 3,920 per ton as traders worried about Vietnam's 2026/27 crop outlook.The Guardian The concern was not just drought or rain. Extreme weather can also increase fungal disease risk, which feeds into both yields and bean quality. For a country that is central to the global robusta trade, that matters immediately for how buyers value near-term supply.

Still, it would be too aggressive to say every price move last week was caused by Brazil alone or Vietnam alone. This is where causal discipline matters. The evidence most strongly supports a view that rain-delayed harvesting in Brazil triggered the first leg higher, while concern over Vietnam's next crop helped keep the risk premium elevated. But another explanation remains plausible: part of the move was likely amplified by speculative positioning and follow-through buying once prices broke through key technical levels. The available reporting is not enough to assign exact weights to each factor, so the more defensible conclusion is that several supply risks are pushing in the same direction at once.

It is also important to remember that the market still has natural brakes. Cocoa Intel said Vietnam exported 1.1 million tons of coffee in the first half of 2026, up 9.7% from a year earlier.Cocoa Intel That flow, together with shipments from Honduras, is why this rally should not be read as a straight line. If exports continue to move steadily, prices will need fresh negative news to keep climbing at the same pace.

How new investors should read coffee

The practical impact depends on where you sit in the chain. Farmers and exporters with inventory can benefit when local buying prices rise. Processors and roasters that have not locked in input costs face margin pressure instead. For equity investors, the lesson is not to assume that higher coffee prices automatically mean every coffee-linked company is a winner. Inventories, sales contracts, hedging ratios, and pricing schedules matter much more than the headline move in the commodity itself.

That is why coffee should not be read like a momentum stock. It trades on crop cycles, weather, certified inventories, shipment timing, and speculative flows on international exchanges. A single down day at the end of the week may reflect profit taking, better weather expectations in Brazil, or simply a market digesting an unusually fast run-up. Not every daily move deserves a grand narrative.

The clearest thesis right now is that the coffee market is looking at the next crop with more caution because the risk sits in quality and delivery timing, not only in headline production. That is why the late-week pullback is not enough to overturn the bullish story built since late June. Three signals are worth watching over the next one to two weeks: whether drier weather allows Brazil's harvest to accelerate, whether post-drying quality reports deteriorate, and whether domestic prices in Vietnam can hold around VND 93,000 per kilogram or start slipping below that zone.Vietnambiz

If all three trend negatively, today's risk premium still has room to persist. If Brazil's harvest speeds up and Vietnamese exports continue to flow, the market is more likely to move from a strong rally into a noisier consolidation phase. For newer investors, that distinction matters. The goal is not to guess tomorrow's price. It is to understand what kind of risk the market is paying for right now.