For many newer investors, the intuitive read is straightforward: if the U.S. dollar softens globally, pressure on the Vietnamese dong should ease almost immediately. This week is a good reminder that the mechanism is more complicated than that. DXY can fall sharply on weaker U.S. data while USD/VND barely moves because Vietnam's exchange rate is still anchored by real dollar demand at home.

The simplest way to frame it is this: DXY tells you whether the external wind is blowing harder or softer. USD/VND, by contrast, reflects how much dollar demand is still coming from import payments, foreign-currency liabilities, liquidity management and defensive corporate balance sheets. If that domestic demand has not cooled, the exchange rate can remain firm even after the global dollar loses momentum.

That leads to a clean thesis for the entire piece. A weaker dollar abroad only removes part of the external pressure. The dong does not really get breathing room until domestic dollar demand begins to cool as well, especially through imports, the trade balance and commercial bank pricing.

DXY is only the outer layer of the story

The global mood shifted after the June U.S. jobs report. Vietnamese financial media, citing U.S. Labor Department data, reported that nonfarm payrolls rose by only 57,000 in June while the unemployment rate held at 4.2%.CafeF Once labor-market momentum cools, investors have fewer reasons to assume the Fed must stay as hawkish as before.

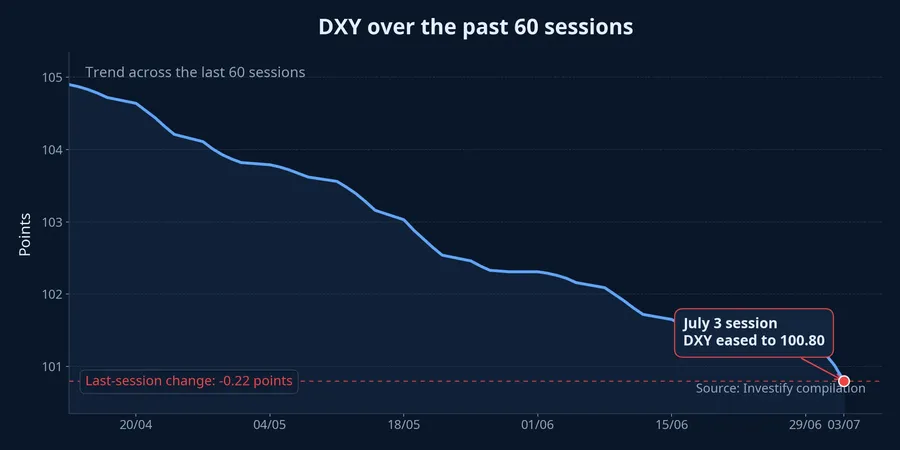

That change in expectations showed up quickly in the dollar. Thanh Niên reported that the U.S. Dollar Index slipped to around 100.85 on July 3 as investors reassessed the Fed path after weaker-than-expected payroll data.Thanh Niên In Investify's market database, DXY closed at 100.80 on July 3, down 0.53% from the previous session.

In plain English, the logic is familiar. If markets think U.S. rates are less likely to move higher, dollar assets usually lose some of their yield advantage. That takes some of the defensive bid out of the greenback and gives emerging-market currencies a bit more room. This is why a softer DXY is usually treated as the first positive signal.

But “first” is not the same as “enough.” DXY measures the dollar against a basket dominated by major currencies such as the euro and the yen. It does not automatically tell you how fast the dong should strengthen, because Vietnam still has its own domestic layer: who needs dollars, in what size, and whether the supply is actually ample enough to meet that demand.

USD/VND still answers to real domestic demand

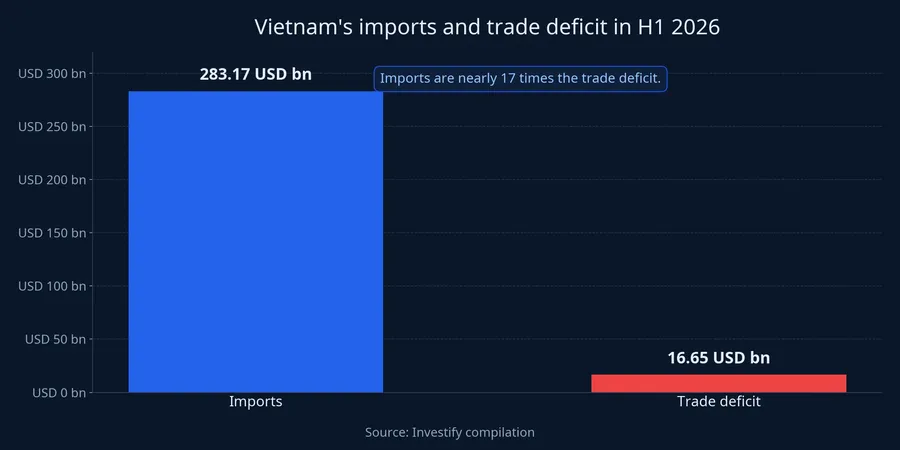

The domestic numbers explain why the exchange rate has not eased much. In the first half of 2026, Vietnam's imports reached USD 283.17 billion, up 33.4% from a year earlier.Báo Chính phủ Over the same period, the merchandise trade balance swung to a USD 16.65 billion deficit, versus a USD 7.95 billion surplus a year earlier.VOV

That matters because it sits directly on top of real foreign-currency demand. When businesses import more machinery, components and raw materials, they need more dollars to settle those payments. From a growth perspective, that may simply mean production is recovering. From an exchange-rate perspective, however, the immediate effect is higher demand for USD inside the system.

This is where many retail investors misread the setup. They see DXY falling and expect USD/VND to mirror the move. But the two variables are being driven by different forces. One is about the market's view on U.S. rates. The other is about how much foreign currency Vietnamese companies still need to buy for actual transactions.

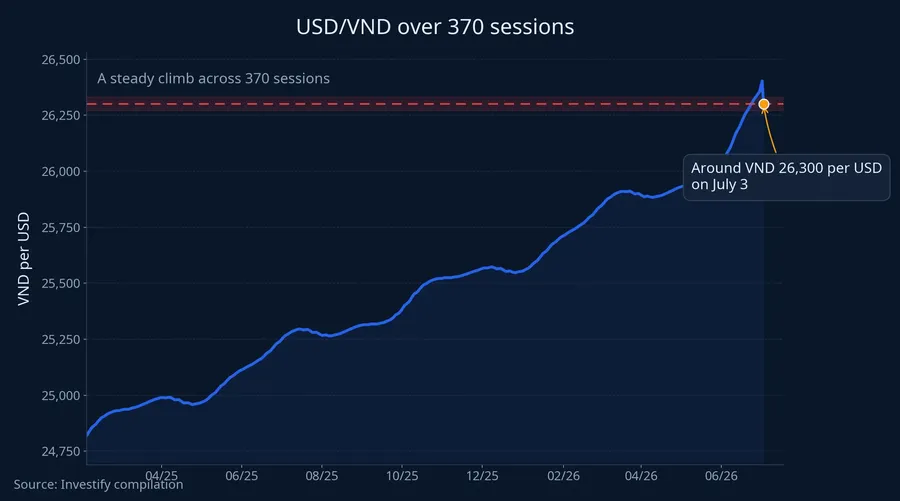

The official pricing framework also points to gradual adjustment rather than a sharp turn. On July 3, the State Bank of Vietnam set the central rate at VND 25,203 per USD, down just VND 2 from the previous day; with the ±5% band, the ceiling for commercial-bank trading stood at VND 26,463.VietnamPlus That is a softer signal, but it is still a measured one.

Over a longer window, the 370-session chart tells the more important story. USD/VND has been moving higher through a cumulative trend, not through a single headline spike. For newer investors, that is the useful lesson: the exchange rate is rarely just a reaction to one overnight report. It is the end result of months of trade flows, liquidity conditions, expectations and policy management.

Imports are keeping the domestic pressure alive

When imports are running 33.4% above last year, that is not a side note in a macro report. For the exchange rate, it is often more important than a one-session move in DXY. The more firms need to buy dollars to pay suppliers, the harder it becomes for USD/VND to come down quickly.

That does not mean stronger imports are inherently negative. In many cases they reflect inventory rebuilding, better manufacturing activity or preparation for a stronger order cycle. But the FX market reacts first to the immediate need for dollars, not to the revenue those goods may generate several months later.

So the right analytical question is not whether the dollar will rise or fall tomorrow. The better question is which layer of pressure is truly fading and which layer is still fully in place. Right now, the evidence suggests that external pressure has eased, while domestic foreign-currency demand has not.

Gold and equities still have to pass through the FX filter

One practical consequence is that local gold cannot be read from global bullion prices alone. In Investify's database, spot gold rose to USD 4,170.51 per ounce on July 3, up 1.16% from the prior session. On the same day, SJC gold's selling price climbed to VND 151.4 million per tael, up 2.02%. The direction is the same, but the magnitudes diverge because local gold always passes through the exchange-rate channel as well as domestic supply-demand conditions.

For newer investors, the easiest analogy is to treat global gold as the raw input price and local gold as the final retail price after the FX conversion and market-specific premium. If USD/VND is still elevated, the domestic gold market is unlikely to behave as a clean copy of the international chart. The local pricing layer remains too important.

The same logic applies to equities. Companies that import raw materials, borrow in dollars or carry USD-linked input costs are still exposed if USD/VND stays firm. Exporters may gain on translation, but that benefit depends on how much imported input they carry, how healthy margins are, and whether their order book remains stable.

In other words, the headline “the global dollar is weaker” does not translate into the same outcome for every asset. Gold tends to react quickly to shifting Fed expectations, but local prices are still filtered through Vietnam's FX conditions. Equities face the same split: the outside signal may improve, but the final impact depends on each company's revenue mix, cost structure and balance sheet.

What investors should watch next

Instead of relying on one indicator, it helps to break the picture into three layers. The first is DXY and U.S. Treasury yields, because that is where the external pressure signal comes from. If U.S. data keeps weakening, the outside environment for the dong could improve further. But that remains only a necessary condition.

The second layer is domestic dollar supply and demand, especially imports, the trade balance, FDI disbursement and commercial-bank pricing. This is the part that answers the more difficult question: are dollars actually becoming less scarce inside the Vietnamese system? If that layer does not ease, USD/VND can stay high or move lower only very slowly.

The third layer is policy response. If the central rate continues to edge down in small increments while bank quotes remain close to elevated levels, the message is clear: policymakers are taking advantage of a softer external backdrop, but they are not treating the pressure as fully resolved. That distinction matters, especially for retail investors who tend to overread a single move in DXY.

The bottom line is straightforward. A weaker dollar globally is good news, but it solves only half the problem. Until domestic USD demand cools more convincingly, especially through imports and the trade balance, the dong is not really out of pressure just because DXY has slipped. The signals worth monitoring over the next two weeks are the next round of U.S. data, commercial-bank USD quotes, and whether import momentum remains as hot as it was in the first half.