When new investors hear “investment fund,” they often think of a convenience product: let someone else choose the stocks for you. That is true, but incomplete. In a more mature financial system, funds also move idle savings into long-term corporate funding needs instead of forcing almost every financing path back through banks.

That is why the latest remarks from Dao Minh Tu, Vice Chairman and Secretary General of the Vietnam Banks Association, deserve more attention than a routine conference quote. Speaking at a banking conference on July 3, he argued that Vietnam needs to develop medium- and long-term capital markets more aggressively, especially equities, bonds, and investment funds, to ease the funding pressure on the banking system.Báo Đầu tư

The key phrase is “ease the pressure.” This is not really a story about adding another product to the market menu. It is a structural question about who is carrying long-term financing for the economy, and whether too much of that burden has landed on bank balance sheets.

Why Banks Are Carrying Too Much

Banks are naturally designed for intermediation: taking deposits, extending credit, managing liquidity, and pricing credit risk. In Vietnam, though, they have also become the default gateway for long-term funding, whether a company wants to expand a factory or fund a project.

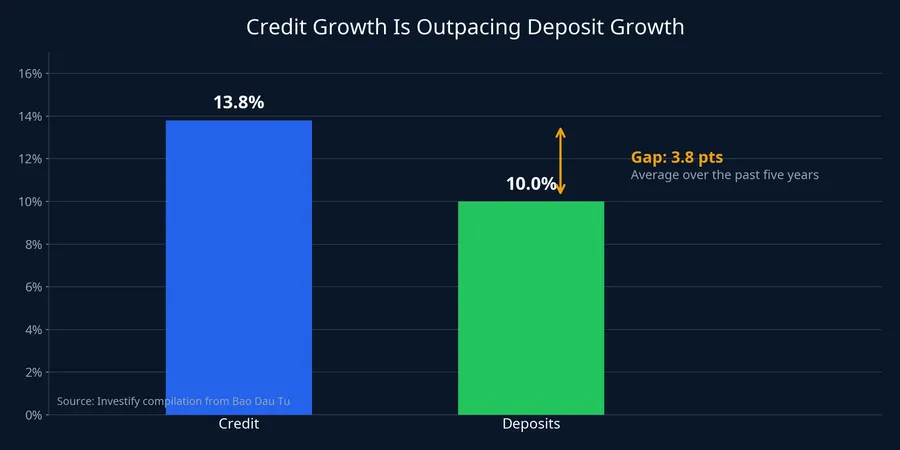

The mismatch is that bank funding sources do not always line up with how the economy uses money. Per Bao Dau Tu, average credit growth has exceeded deposit growth by 3.8 percentage points over the past five years. System-wide LDR is running at roughly 111% to 112%, and by June 26, 2026, total system credit had climbed above VND 19.97 quadrillion, up 7.41% from the end of last year.Báo Đầu tư

In plain terms, if borrowing demand keeps growing faster than deposits, banks have to keep stretching to support credit growth while preserving liquidity safety. Bao Dau Tu also reported that as of June 15, 2026, credit growth was still 2% ahead of deposit growth, even though the system continued to maintain a 100% payment capacity ratio.Báo Đầu tư That is not an immediate safety crisis, but it does mean the current funding structure depends too heavily on one door.

The deeper issue is that when both short-term and long-term financing are routed through banks, the financial system has fewer shock absorbers. Companies become more dependent on bank credit than they should be, while savers have fewer professional intermediary channels than a more balanced market would normally offer.

How Funds Actually Relieve the Burden

Funds matter here not as a substitute for stocks, but as a way to pool capital. When an investor buys units in an open-end fund or an ETF, that money enters a structure with portfolio rules, risk controls, disclosure obligations, and professional oversight.

This matters because capital markets need a deeper base of institutional investors that can read financial statements, value assets, monitor governance, and hold positions for longer periods. Funds are one of the clearest ways to turn fragmented retail money into a more disciplined capital pool. As that pool grows, companies gain another source of financing outside banks.

For new investors, funds also create an intermediate rung between bank deposits and single-stock risk. People who are not yet confident reading company filings can use open-end funds or ETFs to access broader portfolios from the start.

What the Draft Securities Law Could Change

Demand alone is not enough. If Vietnam wants more money to flow through funds, the legal infrastructure has to allow fund products to scale. That is where the draft revision to the Securities Law becomes relevant.

According to Thoi bao Tai chinh Viet Nam on July 3, 2026, the draft proposes revising the ETF definition so that funds could receive and exchange “other assets” under future government rules, rather than being limited only to securities baskets under the current framework.Thời báo TC That may sound technical, but it goes to the heart of ETF scalability. Large ETFs need creation and redemption mechanisms that are flexible enough to track benchmarks and handle inflows and outflows with less friction.

The same report says the draft would remove the 10% limit for constituent securities that belong to the benchmark index an ETF is replicating.Thời báo TC That matters because an ETF that scales quickly can run into technical ownership limits in some index names. If that happens, the fund may have to trim positions or stop accepting new money just as demand is building.

Source discipline matters here. These are still draft proposals, not active regulations. But the fact that ETF bottlenecks have been written into the draft suggests policymakers are looking at the right layer of market infrastructure.Thời báo TC

Another proposed change would allow the Investors' General Meeting to delegate certain decisions to the fund representative board, including financial statements or the selection of an audit firm, if that authority is defined in the fund charter.Thời báo TC In substance, it is an attempt to make public funds less rigid operationally while keeping oversight through charters and disclosure.

The Market Is Wider, but Depth Still Lags

The bigger picture is that Vietnam no longer lacks market participation. Nhan Dan reported that by the end of May 2026, securities accounts had surpassed 13 million, equivalent to more than 13% of the population, while equity market capitalization had moved above VND 10.6 quadrillion.Nhân Dân

But breadth is not the same thing as depth. If most trading still comes from retail investors moving in and out on short-term news, the market remains more vulnerable to sentiment swings and abrupt rotations. For the market to mature, it needs a larger layer of capital that follows an investment process rather than emotion.

Nhan Dan also reported that the revised Securities Law is expected to be submitted to the National Assembly in October 2026.Nhân Dân That timeline is not enough to conclude which provisions will survive intact, but it does signal a policy direction aimed at upgrading capital markets.

What New Investors Should Take Away

None of this means investment funds are the only answer. The corporate bond market still needs more transparency, listed companies still need better governance, and regulators still need to supervise well enough that trust is not eroded every time a new risk cycle appears. But in the architecture of capital formation, funds are hard to ignore because they create a middle path: more disciplined than atomized retail investing, yet more diversified than asking banks to finance nearly everything.

The core thesis is simple. Vietnam does not lack people willing to invest, and it does not lack companies that need capital. What it still lacks is a large enough intermediary layer to connect those two ends professionally and durably. If investment funds develop in the right direction, pressure on banks will fall not because the economy suddenly needs less money, but because capital finally has more than one path to travel.

The signals worth watching are the real legislative progress of the Securities Law revision and whether more retail money begins moving through fund structures rather than directly through short-term trading alone. When both shift together, Vietnam's capital market will be much closer to relying less on banks by default.