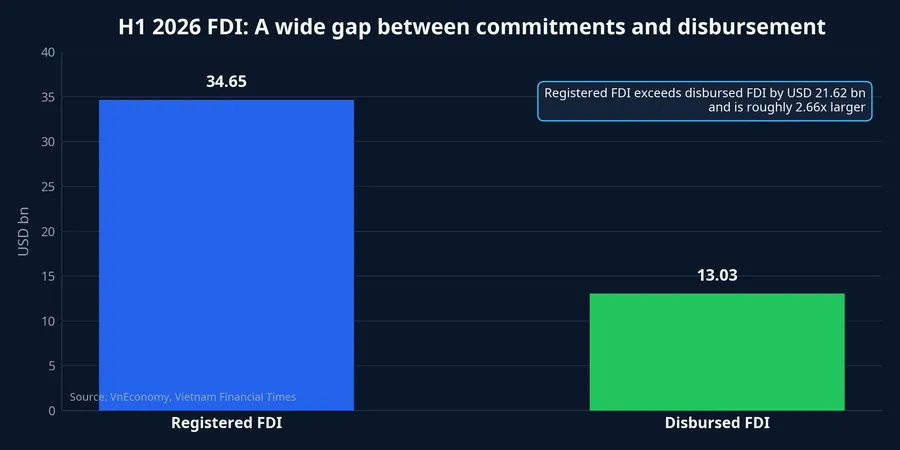

Vietnam drew USD 34.65 billion in registered FDI in the first half of 2026, up 61% from a year earlier. At first glance, that sounds like a straightforward bullish headline for listed industrial park developers: more foreign capital, more factory demand, more land leases.VnEconomy

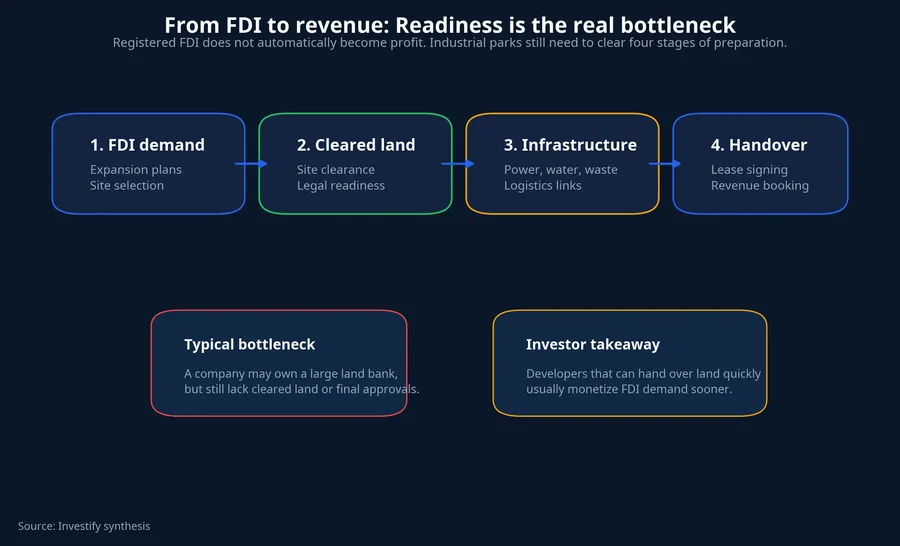

That reading is now too simple. What the market is starting to reward is not just the size of a company’s land bank, but how quickly that land can be turned into booked revenue. In other words, the sector is moving away from a “who owns the most land” story and toward a “who is actually ready” story.

FDI is rising, but the composition matters more

The first reason is that FDI is changing in quality as well as quantity. Newly registered capital reached USD 17.39 billion in the first half, up 87.2%, while additional registered capital for existing projects rose to USD 11.04 billion, up 23.5%. Vietnam is not only attracting new names. It is also keeping existing manufacturers engaged enough to expand capacity.VnEconomy

That matters because an expansion project does not usually wait around for a long development story. It needs speed. Investors should therefore read the FDI headline with more nuance: new commitments can widen demand across the sector, but follow-on manufacturing investment tends to favor developers that can clear land, secure approvals and complete infrastructure fast enough for tenants to start building on schedule.

The chart above captures the gap between intention and execution. Registered FDI exceeds disbursed FDI by USD 21.62 billion and is roughly 2.66 times larger. That gap is the key reminder for equity investors: demand can show up quickly in macro data, but revenue only appears after projects move through the messy real-world steps of site clearance, infrastructure and handover.

The money is still flowing into real production

A deeper look at sector allocation makes the story clearer. Manufacturing and processing attracted USD 17.91 billion in newly registered and additional capital, accounting for 63.0% of the total. On the disbursement side, realized FDI reached USD 13.03 billion, up 11.2% and the highest first-half reading in five years. Manufacturing alone absorbed USD 10.76 billion, or 82.6% of total realized FDI.VnEconomyTBTCVN

This is still a real-economy story, not a fleeting financial-flow story. That raises the bar for industrial park landlords. Electronics, high-value manufacturing and export supply chains are not just buying square meters. They are paying for reliable power, environmental compliance, logistics access and the confidence that operations can start on time.

That is why two developers in the same industrial province can deserve very different valuations. One may have cleared land, usable infrastructure and a location embedded in a supply-chain cluster. Another may also control a large land bank, but if that land is still waiting for compensation, permits or utility connections, the economic value is not ready to flow into earnings yet.

Policy is also pushing the sector toward a new standard

This shift is not driven only by tenant demand. Policy is reinforcing it. Resolution 10-NQ/TW dated June 8, 2026 puts greater emphasis on FDI quality, technology, innovation, green transition and linkages with domestic firms, rather than simply maximizing the volume of registered capital.Chinhphu

At a June 30 implementation conference, Báo Chính phủ reported that the policy direction is shifting from competition among provinces for FDI inflows toward national-level coordination, stronger regional links and a fuller ecosystem for foreign-invested businesses.Báo Chính phủ

That policy angle matters for listed names because it changes what “competitive advantage” means. Low-cost land alone is becoming less decisive. Parks that can host higher-spec tenants, meet environmental standards and connect efficiently to ports, airports and supplier ecosystems are likely to stand in a stronger position as the next investment cycle unfolds.

Why a large land bank is no longer enough

One common retail mistake is to assume that any developer with a large land bank automatically wins when FDI rises. That lens fit an older market narrative better, when investors mostly wanted a long-duration growth story. In the current setting, the more relevant variable is project readiness.

An industrial park developer still has to move through several stages: tenant demand, cleared land, completed infrastructure and finally handover that can be recognized in revenue. If one stage stalls, the entire “FDI beneficiary” thesis can slip by quarters. A favorable macro headline, by itself, does not guarantee near-term earnings delivery at the company level.

The source article points to BCM, KBC and IDC as names that analysts often mention because of their land banks and potential exposure to the next cycle of green, smart and higher-tech industrial parks.Tin Nhanh CK But being named in a brokerage report is not the same as proving who will monetize the FDI wave first. The decisive factors still sit at the project level: approval timing, infrastructure completion, target tenant mix and actual handover capacity.

This is also where investors need to avoid turning correlation into causation. A stronger FDI backdrop supports the whole industry, but company-specific outcomes still depend on site clearance, legal procedures, financing and location within production networks. Ignore those layers, and it becomes easy to buy the right macro story through the wrong stock or at the wrong stage of the cycle.

Five checks retail investors should make

For newer investors, a simple framework helps. First, look at cleared commercial land rather than total headline land bank. How much can actually be leased now, and how much still exists only in expansion plans. Second, check legal progress: land allocation, compensation, permitting and supporting infrastructure all determine how quickly revenue can be recognized.

Third, focus on infrastructure that is genuinely usable, not just promised. Internal roads, power, water, wastewater treatment and logistics links determine whether a tenant can move from signing to operating on schedule. Fourth, look at tenant quality and industry mix. If new inflows are concentrated in electronics, semiconductors, data infrastructure or export manufacturing, technical standards rise sharply.

Fifth, assess the developer’s balance sheet. Industrial parks are capital-intensive long before cash is collected. Developers with stronger finances usually have a better chance of finishing utilities, roads and site preparation on time. That is often the final filter between companies that can capture a new FDI cycle and companies that merely have the narrative.

Bottom line: FDI is the starting point, not the answer

The first-half 2026 FDI numbers are clearly positive for Vietnam’s industrial park segment, but they do not justify a blanket call on the whole group. The strongest thesis supported by the current evidence is that the winners are more likely to be the developers with cleared land, functioning infrastructure, the right supply-chain locations and the operational ability to hand sites over fast enough to convert demand into cash flow.

The main risk to that thesis is not an immediate collapse in FDI. It is execution lag at the project level. If legal work, infrastructure rollout or site clearance slips in coming quarters, part of the growth story will simply be pushed further out. The signals worth watching next are therefore not only aggregate FDI numbers, but also disbursement momentum, which industries are driving new commitments and which listed developers are genuinely shortening the path from land bank to handover.