For a new investor, the phrase “margin cut” can sound like a universal red flag. If a stock is removed from the eligible margin-trading list, the instinct is to treat every name the same way: equally weak, equally dangerous, or equally tempting after a price slide. HoSE’s newly published list of 59 ineligible stocks for the third quarter of 2026 can easily trigger exactly that reaction.CafeF

That reading is too blunt to be useful. A margin cut is not a ranking of corporate quality. It is a rules-based filter. Two stocks can reach the same end state, meaning investors can no longer use borrowed funds to buy them, while the underlying reason is completely different. One stock may be there because the company is loss-making or under trading supervision. Another may be there simply because it has been listed for less than six months and has not yet cleared the minimum time requirement.LuatVietnam

That difference matters more than the label itself. For retail investors, especially first-timers, the real task is to separate technical restrictions from business risk.

What a margin cut actually means

Under current rules, brokerages determine which stocks can be bought on margin based on the list announced by the exchange. Once a stock is moved into the ineligible bucket, investors can no longer use margin loans to open fresh long positions in that name through their brokers.LuatVietnam

That has an immediate effect on the financing layer around the stock. A name that previously attracted leverage-supported demand may see weaker short-term buying power, thinner liquidity and faster sentiment damage once margin is no longer available.

But that technical effect does not explain the full risk picture. Margin is only the outer layer. Investors still need to understand why the stock lost eligibility in the first place.

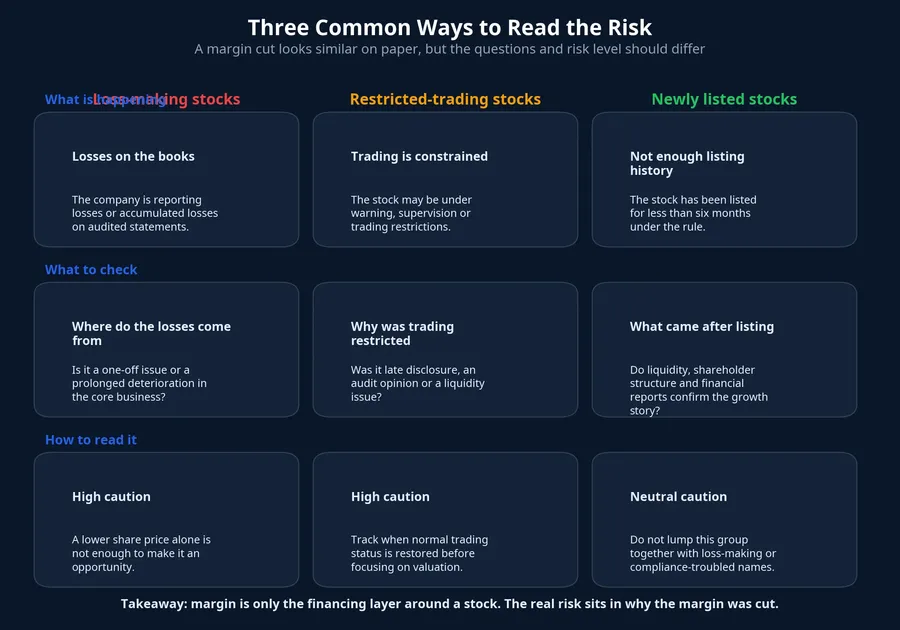

One outcome, several very different risk buckets

CafeF’s breakdown of HoSE’s Q3 2026 list shows that the 59 names do not belong to a single category. Some are already under warning, supervision, trading restrictions or suspension. CafeF cites examples including APG, APH, ASP, BCG, DQC, DGC, HVN, LDG, OGC, NVT, PTL, TDH, TLH, TMT, TTF and VMD.CafeF In those cases, the issue is not just leverage access. The bigger concern is trading status, disclosure quality and whether the market still trusts the company.

Another group consists of stocks removed because of financial performance. Decision 87/QD-UBCK says a listed security is not eligible for margin trading if the issuer posts a loss during the review period or carries accumulated losses on its latest audited annual statements, or on reviewed or audited interim financial statements.LuatVietnam CafeF lists DAH, HAP, SPM, ST8, TNH and VPH in that group, which makes the signal much more directly tied to corporate financial health.CafeF

Then there is the compliance bucket. The same decision excludes shares of companies that receive findings from tax authorities for violations of tax law. CafeF points to names such as GDT, ITD, MDG and STG.CafeF That does not automatically mean the business model is broken, but it does force investors to ask about tax obligations, penalties, cash impact and the clarity of management disclosure.

The lightest bucket in terms of underlying business quality is newly listed stocks that have been on the exchange for less than six months. Under the current rule set, those names simply have not met the minimum listing period required for margin eligibility.LuatVietnam CafeF mentions AAN, ANT, GEL, GHC, HPA, KLB, MZG and TSA, along with ETFs such as FUEMITEC and FUEVN50G.CafeF Here, “margin cut” is mostly a technical restriction, not a verdict on operating quality.

Where retail investors usually get it wrong

The most common mistake is to react to every case with the same mental shortcut. A newly listed stock that is still inside the six-month window gets lumped together with a company that is loss-making or under trading supervision. At the other extreme, a heavily sold-off stock that has just lost margin eligibility can look like a bargain, even though the real issue may be audited losses or a damaged trading status.

Price alone is not enough. If a company has fallen into the loss-making group, the right question is where the losses are coming from, whether they are one-off or structural, whether operating cash flow can absorb them and whether the balance sheet is tightening. A company hit by a temporary expense is very different from one whose core business is deteriorating quarter after quarter.

If the stock is under warning, supervision or trading restriction, the questions change again. Investors should focus first on actual liquidity, disclosure discipline, the chance of restoring normal trading status and the exchange’s response. If normal trading has not been restored, getting trapped in the position can be a bigger risk than any valuation argument.

For tax-related cases, the headline is only the starting point. Investors need to know what the tax finding says, how large the cash obligation may be, whether the issue is administrative or points to deeper internal-control weaknesses, and how openly management addresses it.

Newly listed names are the easiest to misread

This is the bucket where newer investors should be most careful not to overreact. A stock that has been listed for less than six months and is therefore not yet margin-eligible does not carry the same meaning as a stock removed because of losses or trading restrictions. It is not a stamp of quality, but it is not a condemnation either.

The practical implication is that the market still needs more observation time. Investors should ask whether post-listing liquidity is stable, whether ownership is too concentrated, whether results after listing confirm the growth story and whether disclosure discipline remains strong. Those are better questions than treating the margin label as a shortcut.

How to read HoSE’s 59-name list in practice

The most useful approach is to move from the reason to the monitoring task. If the stock is in the loss-making bucket, watch for profit recovery, operating cash flow improvement and changes in the next audit review. If it is under warning or trading restriction, watch for the restoration of normal trading status and for signs that disclosure bottlenecks are being resolved.

If it is in the tax-violation bucket, the focus should be on the actual financial obligation and how it affects earnings and cash. If it is newly listed, the focus should be on post-listing data rather than the margin label itself.

Another phrase that investors often misread is “margin reinstatement.” When a stock leaves the ineligible list, it may attract some technical buying because brokers can reopen margin access. But that is not a guarantee that the share price will rise. It only means that a previous restriction no longer exists at the review date. Price still depends on earnings, cash flow, supply and demand, and market confidence.

The reverse is also true. A margin cut is not automatically a sell-at-any-price signal. If the cause is simply insufficient listing history, the risk profile is completely different from a stock under trading restriction. But if the cause is audited losses, accumulated losses or tax violations, a deep price decline is still not enough on its own to turn the stock into an opportunity. Investors need evidence that the underlying issue is being fixed.

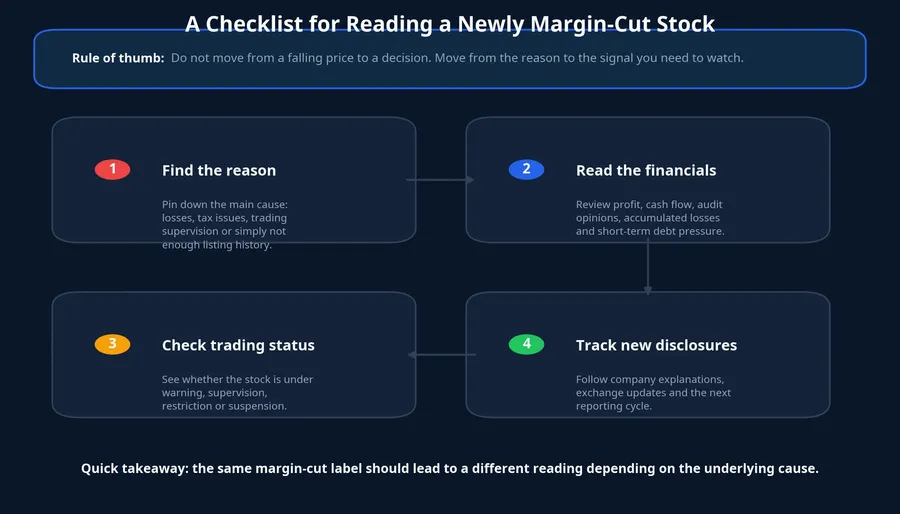

A short checklist for newer investors

Instead of asking whether a margin-cut stock is still “buyable,” retail investors should follow a different sequence. First, identify the reason for the margin cut. Then read the financial statements, check the trading status and monitor new company and exchange disclosures. That order helps separate a technical signal from a fundamental problem.LuatVietnam

The core thesis is straightforward. HoSE’s list of 59 margin-cut stocks should be read as a risk map, not as a uniform basket of bad companies. The loss-making bucket, the restricted-trading bucket and the compliance bucket deserve a meaningfully higher level of caution than the newly listed bucket. In the sessions ahead, the most important signal is not simply how these tickers trade, but whether the underlying reason for the margin cut is being resolved. That is what will determine whether the label disappears quickly or stays attached much longer than the market first assumes.