Vietnam has just crossed a milestone that many economies spend years trying to reach: upper-middle-income status under the World Bank’s classification system. A 2025 Atlas GNI per capita figure of USD 4,970 is more than a neat statistical marker. It signals that the economy’s income base has moved into a different bracket of resilience and scale.VietnamPlus But if you own Vietnamese equities, the right takeaway is not “good macro news means buy the whole market.”

Put simply, an economy moving into a higher income bracket is a bit like a household reaching a more stable earnings level. It can support stronger consumption, more confident borrowing and more structured long-term spending. What it does not do is make every store sell more the next morning or guarantee that every listed company will post higher profits next quarter.

What actually changed

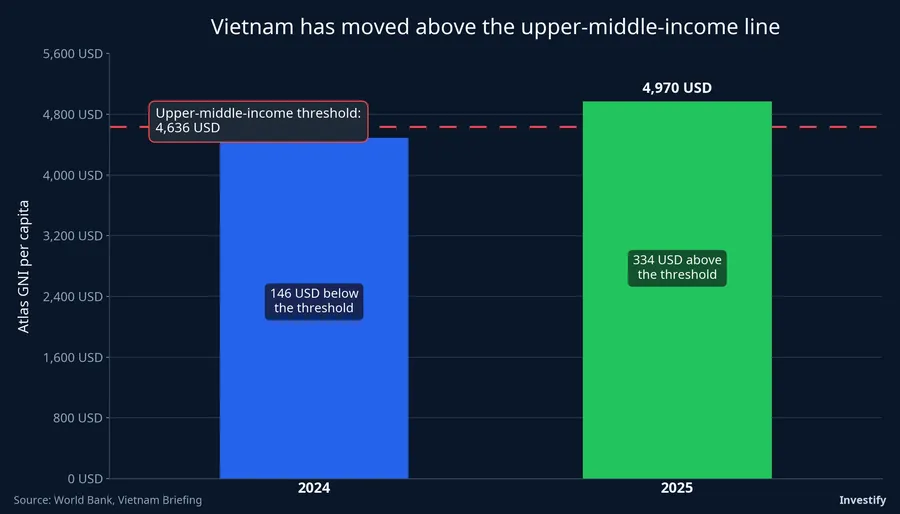

The World Bank updates its country income groupings every year using the previous year’s Atlas-method GNI per capita.World Bank For the current fiscal year, the upper-middle-income bracket starts at USD 4,636, while the lower-middle-income bracket ends at USD 4,635.World Bank

What matters here is that Vietnam did not cross that line because of a one-off administrative decision or a temporary stimulus package. It crossed because 2025 Atlas GNI per capita reached USD 4,970, or USD 334 above the new threshold.VietnamPlus Vietnam Briefing also noted that the metric rose from USD 4,490 in 2024, which makes this the result of an ongoing climb rather than a short-lived spike.Vietnam Briefing

That is why the upgrade is best read as confirmation of development quality, not as an instant earnings event. It tells investors that Vietnam now sits in a different reference group in the global income map. It does not say third-quarter profits will automatically rise, and it certainly does not say every stock deserves a higher multiple right away.

Why the market did not react on cue

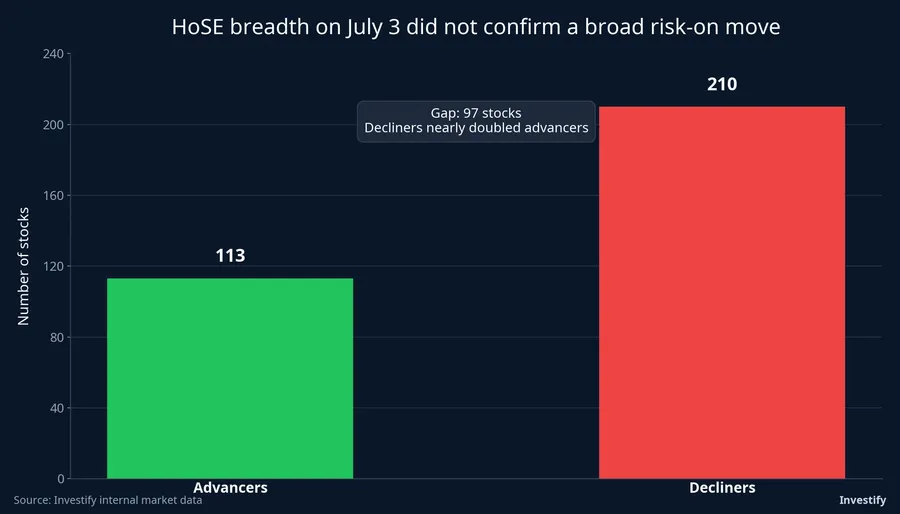

The July 3 session made that point clearly. Even after local media picked up the World Bank update on July 2, the VN-Index still closed on July 3 at 1,862.08 points, down 0.23%. Market breadth on HoSE leaned negative, with 113 advancers against 210 decliners. Financials fell 0.22%, consumer names lost 0.67%, materials slipped 0.60%, and real estate was almost flat with a 0.03% gain.

In other words, markets do not work like an on-off switch for macro headlines. A positive structural milestone can improve long-term confidence in Vietnam’s story, but short-term pricing still depends on how much optimism was already priced in, what the next earnings prints look like and where liquidity is choosing to go. If those factors are not aligned, the index can respond coolly, exactly as it did on July 3.

That distinction matters even more for newer investors. One common mistake is to hear a large, positive national headline and jump straight to the conclusion that every listed sector should benefit immediately. Real markets are more selective than that. The same country-level good news may help some businesses more clearly, reach others with a long lag and barely affect some names at all.

Three layers of impact

The first layer is the country backdrop. Once an economy moves into a higher income group, its growth story usually becomes easier to defend to long-term capital, to companies planning new investment and to consumers gradually upgrading their spending patterns. This is the broadest layer of impact, but it is also the slowest because it reflects structural change rather than a one-session trading catalyst.

The second layer is sector transmission. This is where the story becomes more actionable analytically. Higher incomes often come with stronger demand for services, modern retail, healthcare, education, personal finance and better-quality housing. That is why consumer, banking, insurance, infrastructure and capital-market businesses are the sectors most often discussed around milestones like this one.

Still, that is only the analytical frame. A retailer benefits only if stronger purchasing power actually flows into same-store sales and margins are not eroded by rent and competition. A bank benefits only if credit growth comes with healthy asset quality and does not simply import more NPL risk. An infrastructure company benefits only if projects have legal clearance, funding and reliable payment flows. Without those conditions, being placed inside a “beneficiary sector” is not enough to produce durable profit growth.

Where retail investors usually overread the story

The last layer is the stock itself, and this is where the biggest illusion tends to appear. A company can sit inside a sector with a favorable long-term narrative and still be a poor setup if the market has already priced in most of that optimism. On the other hand, a less-loved name can become worth monitoring if operating data starts to show real improvement in demand or clearer room to expand services.

That is why upper-middle-income status can help you narrow the list of stories worth deeper work, but it cannot do the valuation job for you. Investors still need to come back to the basic questions: where revenue growth is coming from, whether profit quality is durable, how much leverage sits on the balance sheet, whether cash flow is clean and whether the stock is cheap or expensive relative to the actual business quality.

So if the headline “Vietnam enters the upper-middle-income group” leads directly to the conclusion that banks, retailers, real estate and brokers should all surge together, an important step is being skipped. Macro context and profit conversion are not the same thing. A favorable macro backdrop can support valuations over time, but the bridge from backdrop to share price still has to be built with earnings, cash flow and execution.

A positive foundation, not a blanket buy signal

The most important part of this upgrade is that Vietnam has moved up a rung in the global development ladder. That should give long-term investors more confidence in the depth of the country’s consumption story, its financial-services runway and its need for sustained infrastructure investment. It should also encourage newer investors to look beyond short market swings and ask which structural shifts are forming underneath stock prices.

The core thesis is straightforward: this is a positive foundation for selected sectors, not a switch that reprices the whole market at once. If you want to track whether the story is becoming real in listed companies, the better signals over the next few quarters are consumer revenue growth, bank asset quality and infrastructure disbursement progress. Those are the indicators that will show which businesses are actually turning a macro milestone into profits, and which ones are still being carried mostly by expectations.