Many first-time investors instinctively place steady-yield products in the “safe” corner of a portfolio. That instinct is understandable, but it often misses one critical layer: price stability is not the same thing as instant access to cash. On July 2, Blue Owl said investors had asked to pull a combined $4.7 billion from two flagship funds in the second quarter of 2026, even though both vehicles kept a standing 5% quarterly repurchase cap.AOL

The real lesson is not that Blue Owl is suddenly insolvent. The more useful lesson is that redemption pressure eased from the prior quarter's $5.4 billion and still remained far above the exit door that the funds had built into their structure.AOL Put differently, a higher yield does not magically erase the trade-off between return and liquidity.

The details matter. OCIC received $3.6 billion of withdrawal requests, equal to 18.8% of its outstanding shares. OTIC received $1.1 billion, equal to 38.1% of its shares.AOL In dollar terms, OCIC looks bigger. In percentage terms, OTIC is where the redemption stress was much more intense.

Stability on screen is not the same as liquidity on demand

The easiest way to understand this is to separate two layers. The first layer is the underlying asset base. In private credit funds, the assets are often loans that do not trade continuously like listed stocks. When a manager needs cash quickly, it cannot simply sell with one click during the trading day. It may need to hunt for a buyer, accept a discount, or wait for a transaction to be arranged.

The second layer is the investor's exit right. This is the part many retail investors skim. OCIC says its share repurchase program is conducted quarterly and may not exceed 5% of outstanding common shares in a given period.OCIC OTIC states that periodic repurchases depend on available cash, legal requirements, board approval, and may be suspended or terminated at any time.OTIC

Put those two layers together and the misunderstanding becomes obvious. A product can feel calm because it is not repriced publicly every minute the way a listed stock is. But that calm appearance tells you very little about how fast you can get your money back. When too many investors try to leave through a narrow gate, the stress shows up in cash flow first, not necessarily in a flashing price quote.

That is why the word “safe” needs to be unpacked. Safe on price is one thing. Safe on credit quality is another. Safe on liquidity, meaning your ability to turn the position back into cash when you actually need it, is a separate question again.

Why funds keep the exit door narrow

The immediate reaction to a redemption cap is usually that investors are getting trapped. That is only half the story. If a fund owns hard-to-sell assets and lets everyone redeem at once, the early sellers can walk away with the easiest cash while the remaining investors are left with the messier assets. In that scenario, unlimited liquidity can create unfairness between those who leave first and those who stay behind.

That is why a 5% quarterly cap is not only a shield for the manager. It is also a way to slow a run on the door and avoid dumping assets at distressed prices to satisfy whoever gets there first. Reuters reported that both OCIC and OTIC still had enough liquidity to meet repurchases within the current cap and did not need to rush-sell private loans to meet those payments.AOL

From a product-design standpoint, the trade-off is straightforward. Investors give up part of their flexibility in exchange for a chance to earn more than they would in ordinary deposits. In calm markets, that trade-off is almost invisible. Once many people need cash at the same time, the contract makes clear who owns a long-duration asset and who really owns cash.

Blue Owl should not be used as proof that every private credit fund is broken. The evidence supports a narrower point. Liquidity in this product category always comes with structure and limits. The problem is not that one manager wrote a strange contract. The problem is that many investors read the yield number as if it were the whole product.

Where new Vietnamese investors can make the same mistake

Retail investors in Vietnam face familiar choices too: bank deposits, bond funds, corporate bonds, and fixed-income products sold through digital platforms. On the surface, many of them are marketed with reassuring phrases such as “stable,” “steady income,” or “low volatility.” But the redemption rights across those products are not the same.

Bank deposits are usually the easiest to understand. If you break them early, the interest you receive may be sharply reduced, but the process for getting principal back is usually clear. Bond funds work differently. You redeem or sell on the fund's dealing schedule, while the timing of cash settlement depends on the fund's workflow, its portfolio, and the mechanics of processing the order.

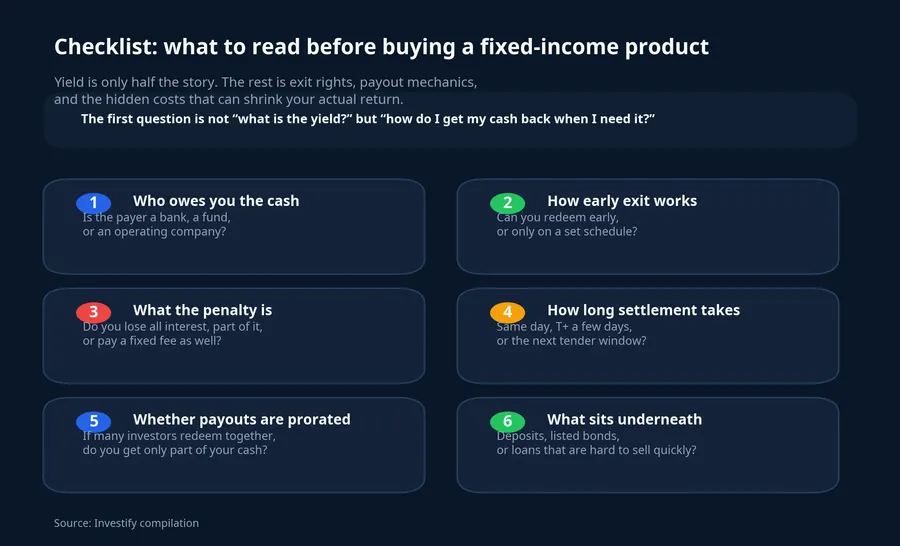

With private corporate bonds, the question shifts to who is willing to buy them back and whether there is a meaningful secondary market at all. With fixed-income products sold on investment platforms, the checklist becomes even more important: who is legally responsible for repayment, what the collateral is, whether early exit is allowed, what the penalty is, and whether payouts can be prorated if many investors try to leave at once.

The practical way to read these products is not to ask “what is the yield?” first. Ask where your money sits, who owes it back, and how the contract behaves if many investors request cash together. Yield is always compensation for some kind of risk. Sometimes that risk is credit quality. Sometimes it is interest-rate risk. And sometimes, as Blue Owl shows, the risk sits in the liquidity door itself.

A better filter before you commit money

One useful mental model is to split your money into two buckets. The first bucket is money you may need within a few weeks or a few months. That bucket should prioritize certainty of access, even if the return is lower. The second bucket is money you can afford to lock up for longer in exchange for a better yield. Investors get into trouble when they fund the second bucket with money that actually belongs in the first one.

The key checklist is not just how the interest is calculated. It is six simpler questions: who owes you the cash, whether early exit is allowed, what the penalty is, how long settlement takes, whether payouts can be prorated during heavy redemptions, and whether the underlying assets can be sold quickly at a fair value. Miss even one of those questions and the feeling of safety may rest on the wrong assumption.

That makes Blue Owl a strong case study in product mechanics rather than a reason to panic about every income-generating product. The evidence does not say that fixed-income vehicles are always more dangerous than stocks. It says something narrower and more useful: if redemption rights are limited, the product does not belong in the cash-ready portion of a portfolio.

Conclusion: Do not confuse yield with cash availability

The core thesis here is simple. Higher-yield products are not inherently bad, but they are misclassified if investors treat them like cash that can be withdrawn at will. Blue Owl merely exposed a feature that has always existed in strategies backed by illiquid assets: a higher promised payout usually comes with a narrower exit gate.

For new investors, the takeaway is not to avoid all income products. The takeaway is to assign each instrument the right job inside the portfolio. The capital that must remain flexible should stay in places with more reliable liquidity. The capital that can stay locked for longer can then reach for more yield. The next useful signal to watch is whether redemption pressure across similar funds cools in coming quarters, because that will say more clearly whether the market is dealing with a temporary liquidity scare or a deeper repricing of the model itself.