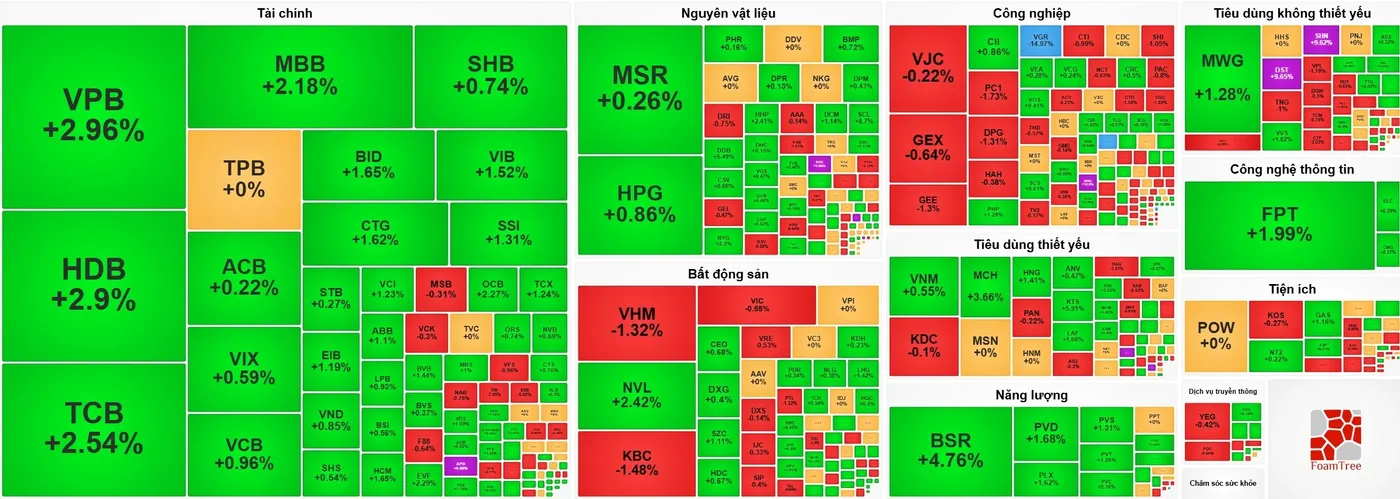

VN-Index added 7.20 points on July 1 to close at 1,867.21. For a new investor, that kind of finish can easily look like a clean signal that money is back and the market is strengthening across the board. But the internal structure of the session says something narrower: the green close was real, yet it was driven by a handful of leadership groups rather than a market-wide advance.

That distinction matters because the index is only an aggregate result. A few large-cap stocks, or a few sectors with enough index weight, can make the market look healthier than it really feels underneath. Vietstock's own recap of the July 1 session pointed in that direction as well: the market held in positive territory, but leadership came from familiar pockets rather than from a synchronized advance across sectors.Vietstock

In plain terms, this was not a "money is back everywhere" session. It was a "money is choosing carefully" session. Flows moved toward areas with liquidity, index influence and a story that was easy for the market to price in over a short horizon.

Where the green close actually came from

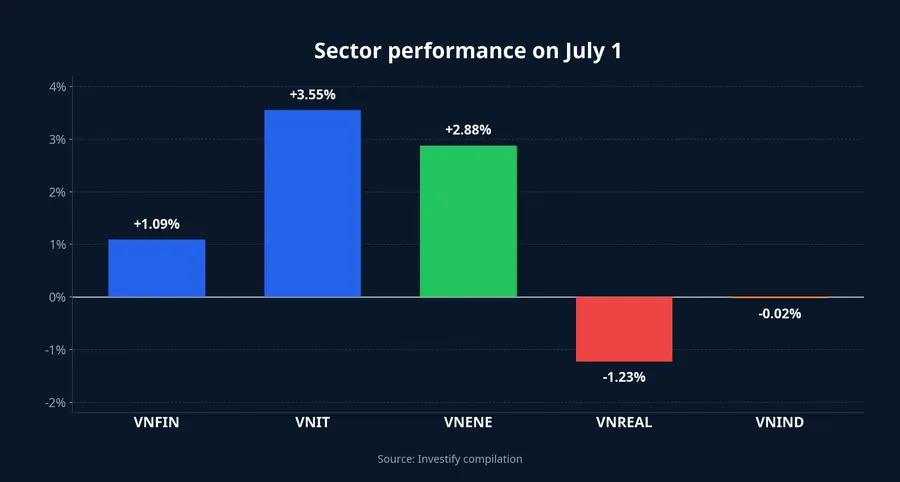

The numbers make that structure fairly obvious. VN30 rose 0.88%, comfortably ahead of the VN-Index's 0.39% gain. Financials climbed 1.09%, information technology gained 3.55%, and energy advanced 2.88%. Real estate, by contrast, fell 1.23%, while industrials were essentially flat at -0.02%. When sector performance looks like that, the first conclusion should be simple: the index was being held up by specific leadership clusters, not by a broad consensus bid.

That is a useful lesson for first-time investors. Reading only the headline index move can create the illusion that almost every corner of the market improved. The July 1 tape shows the opposite. Capital favored financials, technology and energy, while still avoiding weaker pockets such as real estate.

This also explains why the close can look stronger than the session felt in real time. The board ended green, but leadership was still selective. Some groups were clearly doing the lifting, while others were still pulling in the opposite direction.

Financials led, but the move was not uniform

Saying that financials were the main engine of the session does not mean every name in the group won in the same way. Several banks posted solid gains: TCB rose to VND 34,300, VPB to VND 27,700, HDB to VND 26,600 and MBB to VND 25,750. These are exactly the kinds of stocks short-term flows tend to favor when the market wants liquid leaders that can support the index.

But the more important point is not just that financials were higher. It is that investors were not buying the entire sector indiscriminately. They were leaning toward names with clearer near-term narratives. For banks, that may include expectations for second-quarter earnings, better liquidity profiles, or simply their role as index anchors. For securities firms, the link is more direct: better trading activity can feed into brokerage income and margin lending.

That is the difference between broad risk appetite and selective positioning. July 1 clearly fits the second category. The session was constructive, but it was not indiscriminate.

Technology and energy made the rally more credible

If banks had been the only support, the session would have looked much more fragile. That was not the case. FPT rose 3.85% to VND 72,900, and the information technology group as a whole gained 3.55%. That matters because it shows money was not only hiding in defensive index heavyweights. It was also willing to pay for growth stories that still looked attractive on expectations and positioning.

Energy added another leg of support. The energy index rose 2.88%, while BSR gained 5.38%, PLX added 1.35% and PVD climbed 1.98%. This is important because intraday volatility could easily have led to the wrong conclusion that oil and gas remained weak. The closing data says otherwise: energy ended up among the clearest positive contributors of the session, and Vietstock highlighted the group as one of the brighter spots during trading.Vietstock

For newer investors, the takeaway is straightforward. The market had more than one pillar of support. Financials, technology and energy moved together strongly enough to make the green close more believable than a one-stock rescue. But "more believable" is still not the same thing as "broad."

Why real estate kept the picture incomplete

The missing piece on July 1 was real estate, especially at the mega-cap end. VIC fell 1.32% and VHM dropped 2.04%, which meant the sector still acted as a drag on the index. That alone is enough to keep the session from qualifying as a clean, market-wide show of strength.

The mechanism is important. A market can close higher even while one major sector remains under pressure, as long as enough leadership emerges elsewhere. In this case, financials, technology and energy scored enough points for the index, but real estate was still playing against that move.

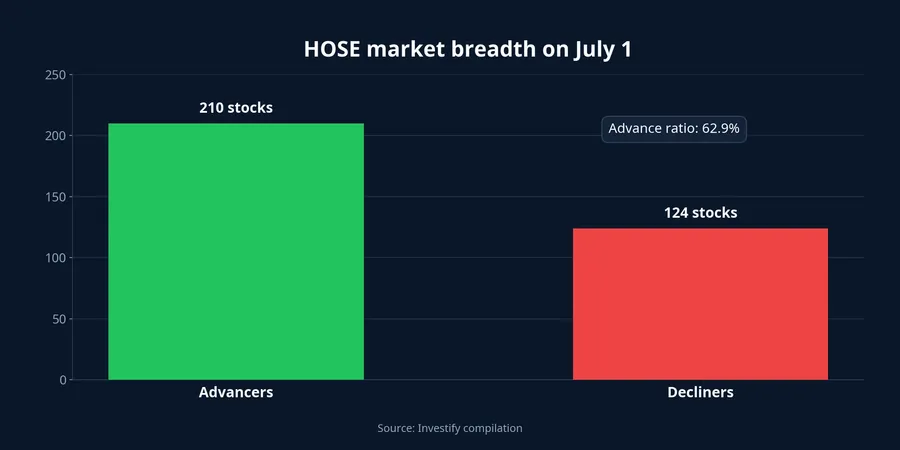

HOSE breadth improved to 210 advancers versus 124 decliners, better than the previous session. Even so, healthier breadth does not automatically confirm a more durable expansion in risk appetite. Breadth still has to be matched by the quality of participation. If more stocks rise but the real money remains concentrated in already-liquid leaders, the market is still selective rather than genuinely broad.

What liquidity says about the quality of the move

Trading volume adds another layer to that reading. VN-Index volume reached 615,059,624 shares on July 1, down from 691,943,851 shares on June 30. That matters because it keeps us from overstating the strength of the session.

If volume had expanded meaningfully alongside stronger breadth and multiple sector gains, the picture would have looked more like a genuine confirmation of renewed confidence. Instead, the decline in turnover suggests a market that is rotating within leadership groups rather than one receiving a fresh wave of broad-based capital. The green close therefore had quality, but the quality came from selective allocation, not from universal participation.

That distinction should shape expectations. A session like this is not enough to conclude that every part of the market is ready to benefit in the next leg. The more defensible interpretation is that money may continue to favor areas that already proved they can lead, while weaker groups still need time to earn their way back into the trade.

Flows are still tilted toward the heaviest names

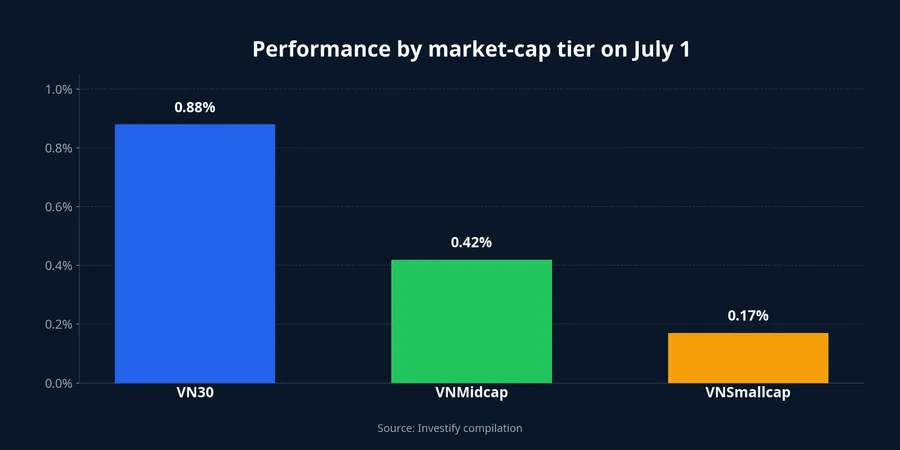

The split becomes even clearer when measured by market-cap tiers. VN30 gained 0.88%, while VNMidcap rose only 0.42% and VNSmallcap just 0.17%. That gap shows money was still leaning toward larger index leaders rather than spreading evenly into mid-cap and small-cap stocks.

That is worth emphasizing because "the market is up" and "most portfolios feel better" are not the same statement. When money is concentrated in VN30, the headline index can look healthy while many accounts with heavier mid-cap or small-cap exposure feel only limited improvement.

So the cleanest thesis after July 1 is not that the market has entered a fully broad recovery. It is that the market has built a visible base of leadership strong enough to keep the index green, while the spread into smaller-cap layers remains limited. That is constructive, but conditional.

What to watch next

After a session like this, the three key signals remain breadth, liquidity and participation beyond the leadership group. If advancers keep outnumbering decliners and turnover improves, the market will have a stronger case that the rebound is moving beyond a few heavyweights. If VN30 continues to lead while mid-caps, small-caps and real estate lag, then the current selective structure is still intact.

The short conclusion is this: July 1 was good enough to show the market has not lost its footing, but not broad enough to claim that money has returned to the entire market. Financials, technology and energy carried the tape. The missing pieces are real estate, stronger liquidity and wider participation across smaller-cap tiers. If those pieces improve over the next few sessions, the setup becomes more convincing. If they do not, this remains a selective rally, one where the index looks better than the average portfolio may feel.