The headline that can scare gold holders most is not always a price drop. Sometimes it is a claim that sounds final: from July 1, 2026, every gold-bar sale will immediately be charged a 0.1% personal income tax on transaction value. The problem is that this interpretation is moving faster than the paperwork. According to Báo Chính phủ, the Ministry of Finance said tax on gold-bar transfers is not yet being collected from July 1, 2026.Báo Chính phủ

Put simply, the law has opened the door, but the cashier still does not have instructions to collect the money. For first-time investors, that distinction matters because it separates a rule that is already operating from a rule that still needs an implementation step. If you miss that difference, you can end up selling out of fear rather than because the numbers justify it.

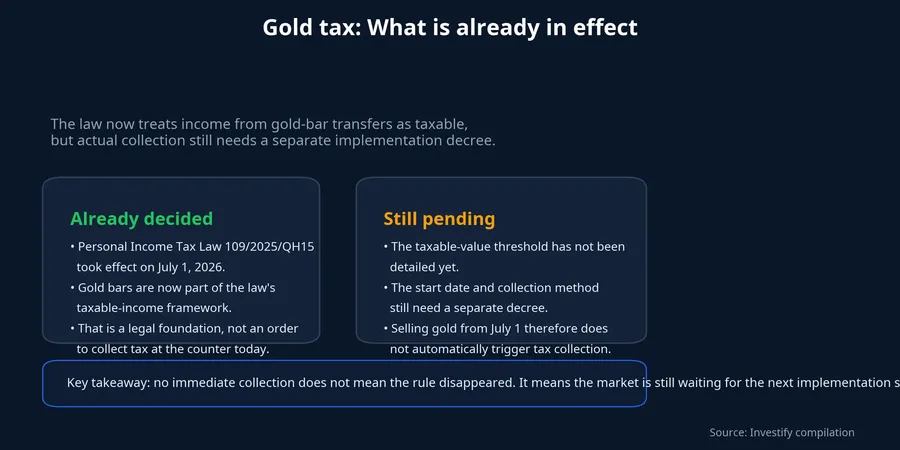

The law is effective, but that does not mean tax is charged immediately

Personal Income Tax Law No. 109/2025/QH15 took effect on July 1, 2026 and added income from gold-bar transfers to the taxable-income category.Văn bản CP Read in isolation, that sounds like every gold-bar transaction from the morning of July 1 should already face tax collection at the counter. But that is a very short reading of a longer legal process.

Per Báo Chính phủ, the law still leaves crucial details to the government, including the taxable-value threshold for gold bars, the actual start date for collection, and any adjustment of the tax rate to fit the broader roadmap for managing the gold market.Báo Chính phủ In plain language, the framework exists, but the practical conditions for applying it are not complete. That is why moving straight from “the law is in effect” to “selling gold today triggers tax collection” is a leap the source does not support.

The cost that distorts today’s decision usually is not tax

If you are holding SJC gold bars, the first question should not be “do I need to sell now to avoid tax”. It should be “what real cost do I lock in if I sell today”. At this stage, the most immediate cost is still not tax. It is the gap between the store’s buy quote and sell quote.

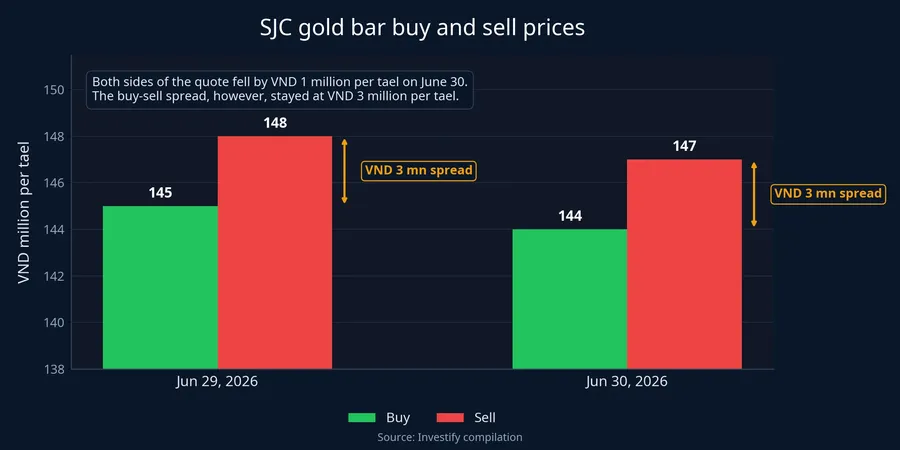

On June 30, 2026, SJC gold bars were quoted at VND 144,000,000 per tael on the buy side and VND 147,000,000 per tael on the sell side. That leaves a spread of VND 3,000,000 per tael, or about 2.08% of the buy price. In other words, if you bought and immediately sold back, the first loss would come from the domestic spread, not from a tax that is already being collected at the counter.

Compared with June 29, 2026, both the buy and sell quotes fell by VND 1,000,000 per tael, yet the spread stayed flat at VND 3,000,000 per tael. This is the detail first-time investors should read carefully. The headline price may rise or fall every day, but the fixed gap between the two sides of the quote is the transaction layer that short-term traders pay almost instantly.

So if you sell only because you fear an immediate 0.1% tax from July 1, you are letting a cost that has not materialized overpower a cost already sitting on the price board.

The bigger risk sits in the premium over world gold

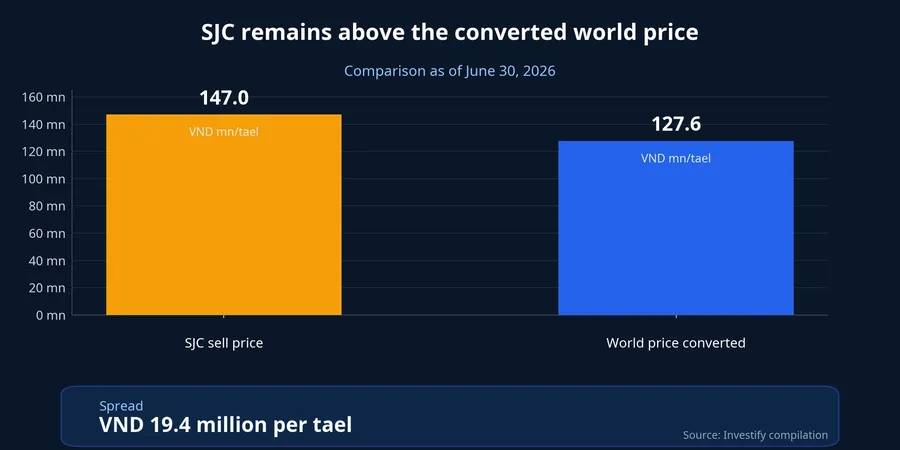

The second layer of risk is the gap between domestic SJC prices and the converted world gold price. On June 30, 2026, world gold stood at USD 4,023.55 an ounce, while USD/VND was 26,303. Converted into one tael, that implies a world gold value of about VND 127,595,670 per tael, which is roughly VND 19,404,330 below the SJC sell quote of VND 147,000,000 per tael. That is a premium of about 15.21%.

That number does not automatically mean SJC prices must fall next. What it does mean is that an SJC holder is not only exposed to moves in global gold. The position also carries a domestic pricing layer. That layer reflects local supply and demand, the market structure around SJC bars, regulatory conditions, and policy expectations. If one of those factors shifts, SJC can react very differently from international gold.

That is also why the tax story should not be asked to explain everything. Even if no tax is collected today, gold holders still face a separate reality: they own an asset whose local sell price remains far above the value implied by the global market. If that premium narrows during a policy adjustment or a change in domestic demand, the impact on a portfolio could be much larger than the 0.1% tax rumor drawing attention right now.

How new investors should read this market

With gold bars, the order in which you process information matters. Start with the legal stage. A law taking effect is one thing. A working mechanism to collect tax in real transactions is another. Until the taxable threshold, start date, and implementation method are defined in detail, investors should not assume their own sale already creates an immediate tax payment at the store.Báo Chính phủ

Next, look at the domestic price board before social media. What is the buy quote. What is the sell quote. Is the spread widening or narrowing. Does the cash you actually receive after selling still match your original target. Before debating a tax that is not yet being collected, investors should know exactly what they are already giving up in the quoted market.

Only then should the holding horizon enter the discussion. If you own gold as a longer reserve asset, one or two sessions of price swings may not decide the outcome. But if you bought into the recent move or plan to trade it tactically, the VND 3,000,000 per tael spread and the roughly VND 19,404,330 gap between SJC and converted world gold are figures you cannot treat lightly. They are the numbers affecting profit and loss today.

What to watch over the next few weeks

There are three signals worth tracking in the near term. First, what the next implementation document says about taxable thresholds, the start date, and who must declare or withhold the tax. Second, whether the domestic buy-sell spread remains elevated. Third, whether the premium between SJC and converted world gold narrows or widens again.

The short conclusion is straightforward. There is no solid basis to sell gold simply because of fear that tax is being charged immediately from July 1, 2026. That part is still waiting for implementation guidance. But that should not be confused with safety. For SJC holders today, the real pressure still sits in the cash realized after the domestic spread and in the very wide gap between local prices and the converted world benchmark. Those are the two cost layers that deserve the closest attention in the weeks ahead.