A project getting relief on pink-book procedures does not mean cash immediately flows back to the developer in the next quarter. What it does signal is that a major bottleneck in the housing market is finally being addressed in the right place: buyer ownership rights, project-related financial obligations, and real secondary-market liquidity. In Vietnamese real estate, cash is often blocked not at the construction site, but in the paperwork.

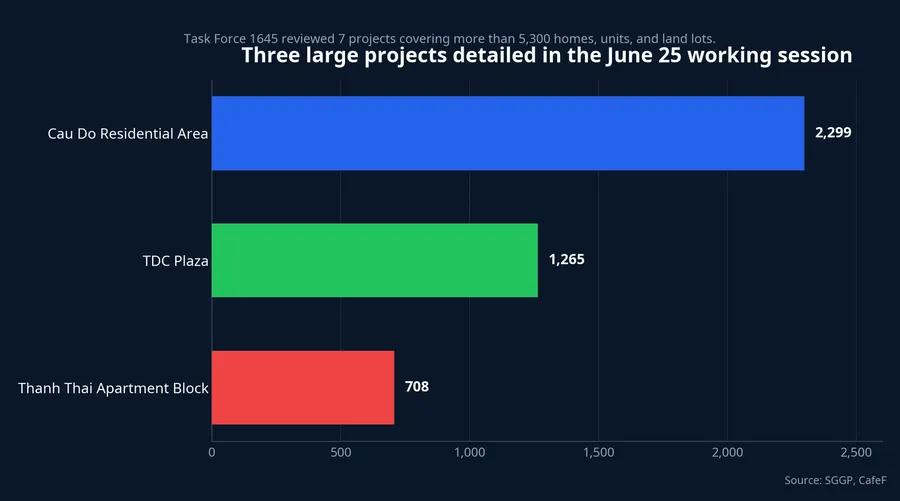

On June 25, Task Force 1645 in Ho Chi Minh City reviewed 7 commercial housing projects covering more than 5,300 apartments, homes, and land lots that need legal clearing before pink books can be issued to buyers.SGGP That is the freshest data point available, and it is a better starting point than the market's habitual shortcut of turning any legal headline straight into a revenue, profit, or stock-price story. Put simply, a pink book is not the final destination of cash flow, but it is the legal switch that gives cash flow a chance to keep moving.

What Has Actually Been Unlocked?

At the June 25 session, the three projects with disclosed scale were Cau Do Residential Area with 2,299 land lots, TDC Plaza with 1,265 units, and Thanh Thai Apartment Block with 708 units.CafeF Those three alone show how much housing inventory can remain trapped in documentation limbo. When paperwork is stuck for too long, buyers may see a finished apartment without fully secured property rights, while developers may see booked sales that have not yet turned into clean cash.

The easiest way to think about it is this: an apartment without a pink book is an asset that has been delivered physically, but not completely delivered legally. The resident may already be living there and may already have paid most of the contract value, yet selling the unit, mortgaging it, or defending ownership in a dispute remains harder than it should be. That is why pink-book progress improves asset quality first, and only later affects how fast money turns over.

Why Pink Books Matter for Cash Flow

For homebuyers, the pink book is the point at which the apartment becomes fully usable as a financial asset, not just a place to live. Without it, sellers often have to accept a legal-risk discount in the resale market, and borrowers may face tighter credit access if they want to use the property as collateral. Once the document is in place, the property's tradability improves first. That kind of liquidity matters far more than a short-term move in asking prices driven by expectations.

For developers, the effect follows a more indirect path. The good news is that once legal obstacles are eased, the company has a clearer path to finishing the last steps, collecting the remaining contractual payments, and reducing complaints from residents. The harder question is how much money comes back, how quickly it returns, and whether it becomes fresh profit. Part of that cash may still need to go toward land-related payments, tax obligations, mortgage releases, or unfinished infrastructure commitments.

That distinction matters for retail investors. Many people see a legal breakthrough and immediately assume that a property developer is about to breathe easier on debt or enjoy a sharp cash-flow rebound. The reality is more conditional. Pink books help reopen the pipeline, but cash returns quickly only when the project is largely sold, buyers are still willing to complete the last payments, and the developer does not face a large final legal bill before the file can close.

From Policy Framework to Individual Files

Pink books do not move faster just because one working session took place. Behind the June 25 meeting sits a broader policy framework. On April 24, 2026, the National Assembly issued Resolution 29/2026/QH16 on special mechanisms to deal with pre-2024 land-law violations and to clear long-delayed projects. On May 7, 2026, the Government then issued Decree 147/2026/ND-CP to guide implementation of that mechanism.Báo Chính phủ

That matters financially in a straightforward way. To accelerate pink-book issuance, the market needs more than goodwill around each project. It also needs a legal framework strong enough for agencies to sign off, take responsibility, and keep files moving. Policy signals without project-level execution leave files stuck. Project-level meetings without legal cover can leave files stalled while agencies seek more guidance.

Relief Does Not Mean Completion

The most common reading mistake is to collapse three different states into one: being placed on a review list, having a legal obstacle partially resolved, and actually receiving the certificate. They are not the same, and their cash-flow effects are different. A project being reviewed for relief only means the bottleneck has been identified. A project moving one step further means the process is alive. Only when certificates are actually issued, or buyers complete their financial obligations after the legal hurdle is cleared, does the money start circulating more visibly.

The market has already seen how long that lag can be. In the final week of June, Thanh Nien reported that residents at a project linked to Quoc Cuong Gia Lai received pink books after 15 years.Thanh Niên That example is a useful reminder: the gap between handing over a home and completing ownership rights can stretch for years. So if investors jump from a legal-relief headline to the assumption that all trapped value has already returned to the developer, they are moving ahead of the evidence.

What Should New Investors Watch Next?

The first signal is whether the process moves from meetings to concrete file progress. After a project is named, the key question is not the stock market's emotional response over one or two sessions. It is whether the file has completed another procedural step. Has the application been fully accepted? Is any part still waiting on taxes, land obligations, infrastructure commitments, or transfer conditions? Those are dry questions, but they decide whether money returns to the company or merely shifts from hope into paperwork.

The second signal is how existing buyers respond. In many cases, the earliest cash does not come from new customers. It comes from people who took possession long ago and are waiting for the final legal step that makes the asset fully secure. If those buyers begin completing their remaining financial obligations, paying relevant fees, and reducing complaints, that is a more meaningful sign than a few strong sessions in property stocks.

The third signal is secondary-market liquidity. Once pink books are truly issued, banks tend to accept the assets more broadly, new buyers demand less of a legal discount, and resale transactions become easier. If that happens, HCMC's housing market is recovering through real transactions. If the legal-relief headlines only push asking prices slightly higher while transaction volume stays thin, the recovery is still operating mainly at the expectation layer.

The Bottom Line

Pink books are not a magic wand that turns backlog into cash in one news cycle. The clearest thesis from late-June evidence is more modest and more useful: Ho Chi Minh City is reopening the legal pipeline one segment at a time, and as the segment closest to homebuyers starts moving again, the quality of the housing-market recovery has a better chance of improving. That is constructive, but it is still a step-by-step improvement rather than a broad instant reset for every listed developer.

For newer investors, the most useful shift is to stop reading real estate solely through stock prices. Pink-book news matters because it shows how tradable the asset really is, how well buyer ownership rights are being protected, and how likely it is that developers can collect cleaner cash. The signals worth watching over the next few weeks are the file-level progress of the projects just reviewed, how financial obligations are completed after those files reopen, and whether secondary-market activity improves at projects where residents are already living on site.