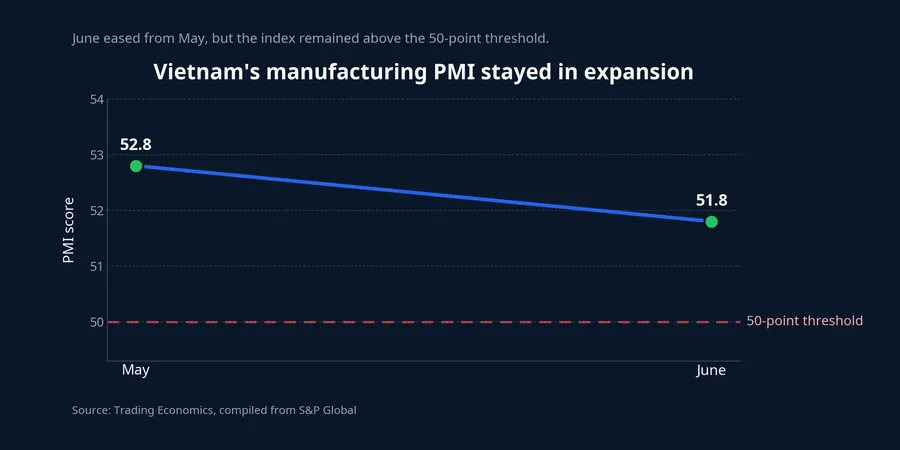

Vietnam's June manufacturing PMI came in at 51.8. That is strong enough to say the sector remains in expansion territory. But the tape on the morning of July 1 was telling a more cautious story: money was not moving evenly across every stock tied to manufacturing.Trading Economics

For newer investors, that distinction matters. A PMI reading above 50 does not mean every industrial, materials, or electrical-equipment stock should rally together. The simpler way to read it is this: PMI is a health check on the sector, while stock prices reflect where the market believes that improving backdrop can actually turn into revenue, margins, and cash flow.

What the June PMI is really saying

According to S&P Global data compiled by Trading Economics, Vietnam's manufacturing PMI eased from 52.8 in May to 51.8 in June, but it remained above the 50-point threshold. That means business conditions were still improving, even if the pace slowed from the previous month.Trading Economics

The constructive part of the report was not just the headline number. New orders kept rising, export orders stayed in expansion, and output grew at the fastest pace since February 2026. On that evidence alone, some readers might expect the market to reward the entire manufacturing complex immediately. But the second half of the report argues for more restraint: input inventories fell at the sharpest rate in a year, while employment in the sector declined for a fourth straight month.Trading Economics

Put differently, companies still have work to do, but not enough confidence to scale up every part of the operating chain. When businesses remain cautious on hiring and raw-material stocking, equity investors usually stop short of pricing in a broad profit rebound across the sector. That is the gap between a better macro signal and a market that still wants company-level proof.

Why the market has not confirmed a broad recovery

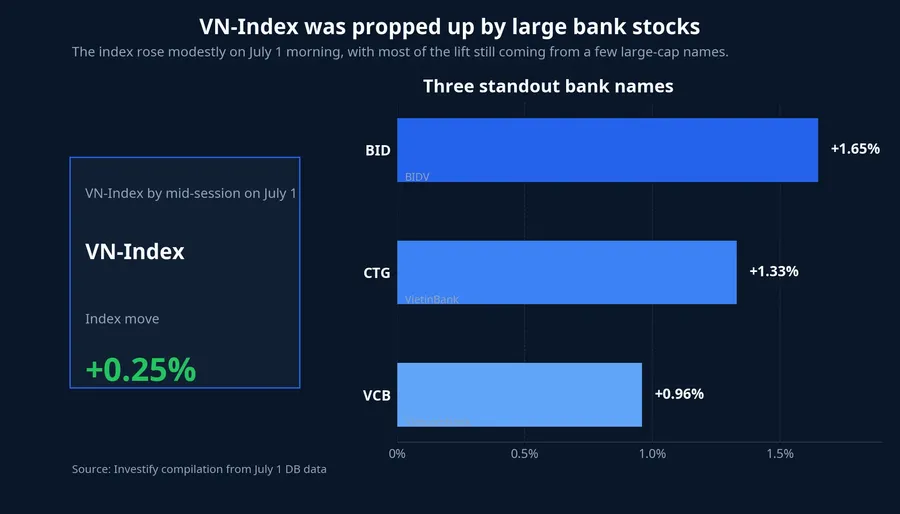

By mid-session on July 1, the VN-Index stood at 1,864.69, up 0.25%, with 182 gainers against 134 decliners. Market breadth leaned positive, but not strongly enough to say investors were making a broad-based bet on a manufacturing rebound.

If the newly released PMI were being treated as the starting gun for a wider recovery, you would normally expect clearer participation from multiple parts of the chain: materials, electrical equipment, components, industrial parks, logistics, and exporters tied to real order flow. Instead, the market's reward function still looked more selective, favoring a handful of specific stories rather than the whole production ecosystem.

That is where newer investors often confuse being right on direction with being right on timing. A macro indicator can point to an improving economy without the stock market paying for that thesis in the same session or the same week. Investors still need confirmation that the improvement is showing up in the earnings path of specific companies, not just in a sector survey.

Where money is actually going

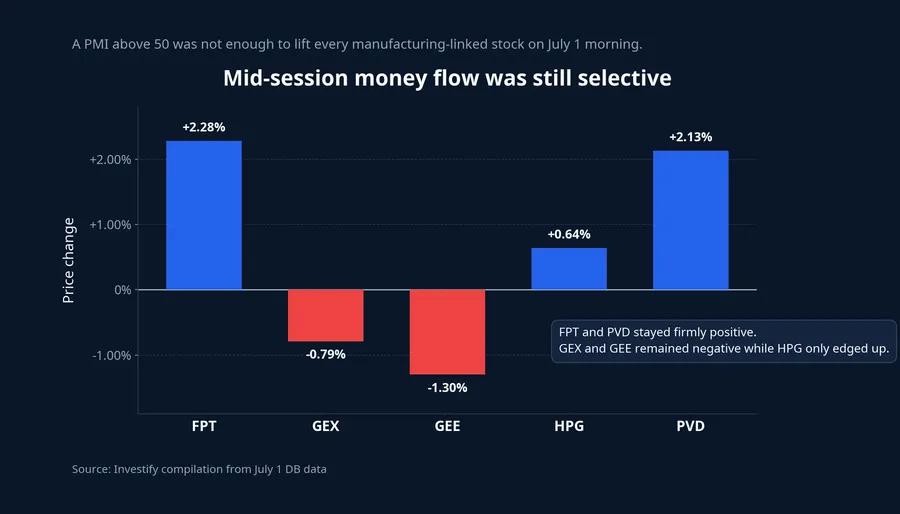

At the stock level, the split was easy to see. FPT rose 2.28% to VND 71,800, while PVD gained 2.13% to VND 33,500. HPG was only up 0.64% at VND 23,450, while GEX fell 0.79% to VND 31,200 and GEE dropped 1.30% to VND 91,100. Those numbers suggest money was not assigning the same value to every manufacturing-linked name.

It is also important not to force all of those moves into one explanation. FPT has as much to do with technology demand and service exports as with manufacturing PMI. PVD is similar. Its gain is also shaped by energy-sector expectations, so using a positive PVD print as proof that the whole manufacturing chain is being repriced would be an inference too far.

On the other side, GEX, GEE, and HPG sit closer to expectations around electrical equipment, industrial activity, and materials. When those stocks do not confirm the same direction, the market is effectively saying that a better PMI report has improved the backdrop but has not yet triggered a broad valuation reset. In other words, investors accept that the macro picture is less weak, but they are not yet treating it as proof that profit growth across the chain is about to accelerate.

What is holding up the index

Another useful layer is the role of large banks in keeping the benchmark positive. During the same morning session, BID rose 1.65% to VND 43,100, CTG added 1.33% to VND 34,400, and VCB gained 0.96% to VND 62,800. When three heavyweight banks lift together, the VN-Index can stay green even if the rest of the market is not participating in a broad way.

That does not negate the constructive PMI signal. It simply means a rising index is not the same thing as a market fully validating the manufacturing story. If the main push still comes from banks and a few large technology names, investors need to separate a healthy index print from healthy breadth. In stronger rallies the two often move together, but they do not have to arrive at the same time.

That is why the more defensible reading remains the cautious one. Nothing in the morning data rules out a broader expansion in money flow over the next few sessions. But at the exact moment the PMI was released, the observable evidence still showed the market favoring stocks with clearer earnings visibility or index-support roles, rather than buying the manufacturing chain as a package trade.

What investors should watch next

The better question is not whether a PMI above 50 is enough to buy the whole manufacturing group. The better question is where money goes next. If, over the coming sessions, materials, electrical equipment, industrial parks, and logistics all improve in both price action and turnover, then the June PMI report will have stronger evidence behind it as the start of a wider recovery.

If money remains concentrated in FPT, large banks, and a few other heavyweight names, then the 51.8 PMI should be read for what it is: a constructive macro base, not a blanket pass for every manufacturing stock. The larger picture right now is that manufacturing does not look weak, but the market is still highly selective about who will actually convert that backdrop into earnings.

The cleanest conclusion at this stage is straightforward. PMI is creating a better base for manufacturing expectations, but the case for a buy-everything rotation is still missing evidence. The near-term signal worth tracking is not only whether PMI stays above 50, but whether money flow broadens into the parts of the chain that are directly linked to orders, output, and margins. If that breadth appears, the thesis gets stronger. If it does not, selectivity remains the most honest reading of the July 1 data.