Late June presents retail investors with an uncomfortable mix of signals. Oil has cooled sharply, the U.S. dollar is still firm, domestic gold remains expensive, and Vietnamese equities have just come off a strong quarter. That combination often pushes new investors into the wrong mental shortcut: avoid what just fell, chase what is still rising, and assume the most visible asset must be the best place to park cash.

That is not the right question. Before comparing stocks, gold, and fixed-income products, the more useful test is simpler: when will this money be needed, how much short-term drawdown can you tolerate, and is the goal capital preservation or higher growth? Without those answers, asset selection becomes emotional substitution rather than financial planning.

Mixed signals first, asset choice second

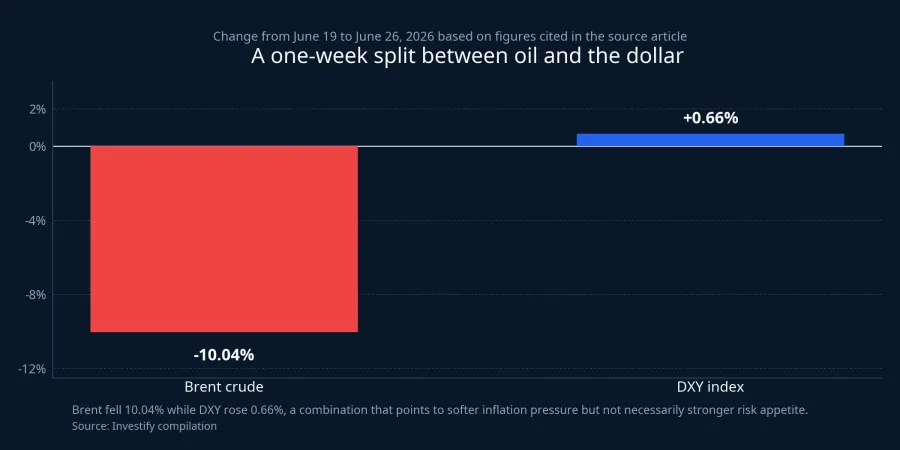

From June 19 to June 26, 2026, Brent crude fell 10.04% while the DXY dollar index rose 0.66%. Over the same stretch, the VN-Index closed at 1,871.91 on June 26, and SJC gold was quoted at VND 148.5 million per tael on June 27. Read in isolation, each figure seems to tell a different story. Together, they say something more useful: this is not a clean risk-on environment.

Lower oil usually helps ease input-cost pressure and softens inflation expectations. A firmer dollar tends to do the opposite for risk appetite, especially in emerging-market assets. So the macro backdrop is not “all clear.” It is more of a split screen: inflation pressure may be cooling, but global confidence is not strong enough to assume risk assets should automatically absorb every idle dong in the room.

For first-time investors, this matters because mixed backdrops call for classification, not prediction. The useful move is to separate money by job. Some money must stay stable. Some can absorb volatility in exchange for a better return profile. Confusing those buckets is usually what causes the most pain later.

Stocks still offer the best upside, but only for patient money

On recent performance, equities are still the most compelling growth asset in this comparison. From March 26 to June 26, 2026, the VN-Index rose from 1,644.63 to 1,871.91, or about 13.82%. Over one year, the index is up roughly 37.07%. Those numbers are powerful, and they naturally create fear of missing out for anyone sitting on cash.

But strong returns do not arrive as a free gift. They come bundled with timing risk. A good market can still be the wrong place for money that must be used in a few months. That is the distinction newer investors often miss: a good asset is not automatically the right asset for a specific liability or spending plan.

The practical framing is straightforward. Stocks are the better option when the money has time, and when the investor can accept a temporary drawdown without being forced to sell. If the cash is earmarked for tuition, rent, working capital, or a near-term purchase, then putting all of it into equities means letting market volatility dictate a real-life plan. That is not investing discipline. It is a mismatch between asset behavior and cash-flow needs.

The current macro mix also argues against simplistic thinking. Lower oil prices can help some sectors by reducing cost pressure. A firmer dollar, however, often keeps risk appetite selective. That means equities remain attractive for the long-horizon bucket, but they are still a poor holding tank for all idle cash just because the market has had a strong quarter.

Gold hedges some risks, but it is not a calm asset

Gold feels safer to many retail investors because it carries a long cultural memory of protection. In broad terms, that instinct is understandable. But protection over a long cycle is not the same thing as low volatility over a three-month window.

From March 26 to June 27, 2026, SJC gold fell from VND 171.5 million to VND 148.5 million per tael, a decline of about 13.41%. Over a one-year window, however, it is still up around 23.75% from June 26, 2025. Those two facts do not conflict. They simply show that gold can preserve value over time while still delivering painful short-term mark-to-market losses to buyers who entered at overheated levels.

That has three implications for beginners. First, gold carries behavioral risk as much as price risk: the hotter the move, the easier it is to justify overpaying out of fear of missing out. Second, the domestic market also involves buy-sell spreads, so the holding period often needs to be longer for the “safety” thesis to work in practice. Third, if inflation pressure is easing somewhat because oil has come down, gold is no longer supported by exactly the same set of drivers that mattered during more intense inflation scares.

That makes gold more suitable as a diversification sleeve or a longer-duration hedge, not as the default destination for all short-term idle cash. If the money may be needed soon, a gold position can become most dangerous precisely when it was expected to feel safest.

Fixed-income products look less exciting, but they solve a different problem

Deposit products and other fixed-income channels rarely inspire the same enthusiasm as a rally in equities or a dramatic move in gold. Yet comparing them on excitement misses the point. They are not designed to win a performance race against growth assets. They are designed to deliver visibility.

VietNamNet reported on June 23 that deposit rates for six- to twelve-month tenors at some banks were running in the 5.9% to 7.4% annual range, while one- to under-six-month tenors were in the 4.1% to 4.6% range.VietNamNet

That matters because short-horizon money has a different job description. If the cash will be used in the next three to six months, the highest priority is usually not to maximize upside. It is to make sure the plan survives intact. For a beginner, the biggest advantage of fixed-income products is not the headline yield. It is the reduction of one of the costliest mistakes in personal finance: buying a volatile asset simply because somebody else made money on it recently.

There is still a trade-off, of course. In exchange for stability, the investor accepts slower growth during periods when equities are running hard. But that trade-off is healthy when it matches the purpose of the money. Short-term money should arrive on time. Long-term money can work harder.

The cleanest framework is to sort cash by when it will be used

The core takeaway from this week is not that one asset has clearly defeated the others. It is that the right answer changes once the time horizon changes. Money needed soon is usually better placed in low-volatility instruments with predictable cash flows. Money that can stay invested through a rough patch can take more equity risk. Gold can still play a role, but mainly as a hedge or diversifier rather than a universal safe box.

That leads to a fairly disciplined conclusion. With Brent down, the dollar still firm, and domestic assets sending mixed signals, idle cash should be allocated by time horizon before anything else. Protect the money that must stay stable. Only the portion that can remain patient should be asked to absorb volatility in pursuit of higher returns. The next two weeks are worth watching for three markers: whether DXY extends its rise, whether SJC gold can stabilize around VND 148.5 million per tael, and whether the VN-Index can hold onto the gains built over the last quarter.