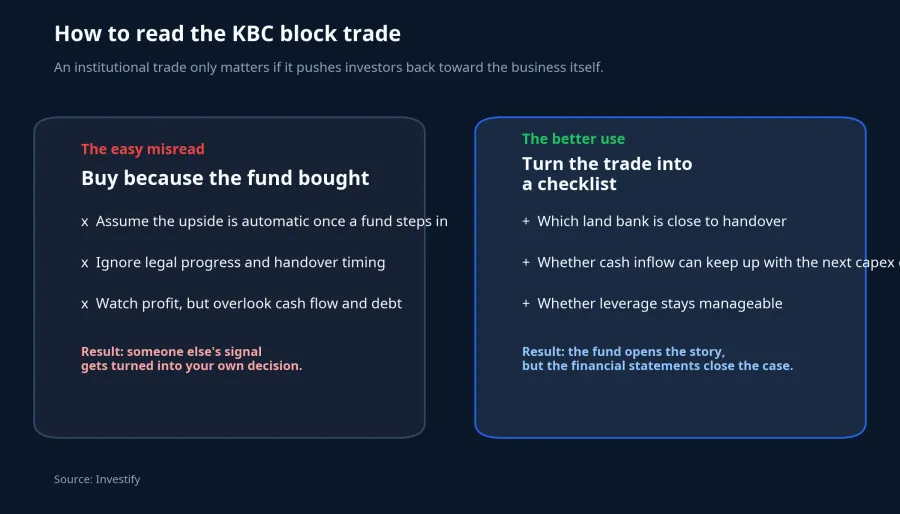

An institutional trade can change the tone of a stock overnight. Once investors see a fund stepping up its stake, many retail traders instinctively read that as confirmation that more upside must still be ahead. With KBC, that reading is understandable, but it is also too shallow. What PVI AM has really provided is not a ready-made answer. It is a reason to re-examine the business more carefully.

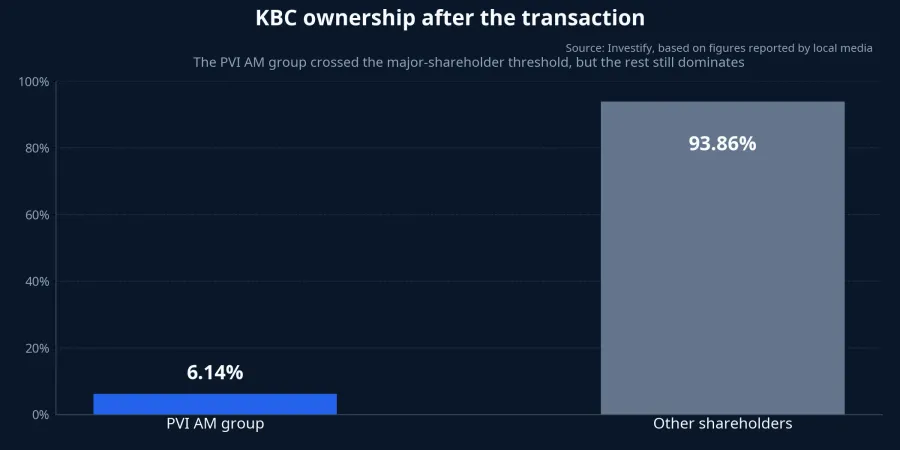

According to figures reported by VnEconomy from the ownership-change disclosure, PVI Asset Management bought an additional 3.46 million KBC shares in a June 16 transaction. After the deal, the PVI AM group and related parties held more than 57.84 million shares, equal to 6.14% of KBC's capital, at an average negotiated price of about VND 30,500 per share, for a total value of more than VND 105 billion.VnEconomy

The important word there is "group." Public information is enough to show that investors affiliated with PVI AM have now crossed into major-shareholder territory. What public information does not reveal is the full investment case behind the trade. It may reflect a long-term view on KBC's asset base, or it may simply be a portfolio-allocation decision inside the fund. If retail investors jump from "the fund bought" to "the thesis is now proven," they are moving much faster than the evidence allows.

From the Trade Back to the Business

KBC is not a bank, a consumer company, or a business that converts effort into monthly revenue in a predictable way. Industrial park developers move first through land acquisition, legal work, site clearance, infrastructure, and tenant relationships. Cash does not come back smoothly every month. It often arrives in lumpy waves, tied to handovers, large contracts, and legal milestones. That is why this type of stock almost always carries a timing gap between expectations and realized cash.

That timing gap is exactly why the PVI AM transaction matters only if it pushes investors back toward the core questions. Which parts of KBC's land bank are close to commercialization? Which areas are still in the expectation phase? And how much of the market's optimism is already resting on future handovers rather than present cash generation? Those questions are much harder than simply spotting a fund name on the tape, but they are also the ones that actually matter.

Another distinction matters here. A major shareholder is not the same thing as a controlling shareholder. The PVI AM-related group is now at 6.14%, which is enough to make future ownership changes more worth tracking, but still far from a stake that can shape KBC's direction on its own. In other words, this is a signal about institutional interest, not about a transfer of control inside the company.

Why KBC Still Draws Attention

If there is a plausible first-order explanation for the trade, the strongest one is still KBC's long-duration asset story. Industrial park developers sit at the intersection of factory demand, manufacturing relocation, and foreign direct investment into Vietnam. A company with the right land in the right locations, backed by enough legal and infrastructure progress, will naturally attract institutional capital that can afford to wait.

Still, correlation should not be mistaken for proof of causation. We can observe that PVI AM increased its stake in June. We cannot say with certainty, based on public data alone, that the fund bought because of one specific project, one tenant pipeline, or one near-term catalyst. The more defensible reading is narrower: professional money was willing to raise its exposure to KBC, and the underlying reason still has to be tested against project execution and future financial statements.

That is also where the fund's time horizon diverges from that of most retail investors. A fund can buy because it is comfortable waiting 12 months or 24 months for an asset thesis to play out. A retail buyer often wants validation within days or weeks. When both groups are looking at the same transaction, they are not necessarily reading the same signal at all.

What the Share Price Has Already Discounted

KBC last closed at VND 29,400 per share in Investify's internal market data. That is about 11.2% above the level seen a year earlier. The move is not extreme, but it is enough to make one point clear: the market was not waiting for PVI AM before it started forming a view on KBC. Some expectations around industrial land, tenant demand, and future handovers had already been reflected in the price.

That is where retail investors can misread the setup. Once they see a fund buying around an average negotiated price of VND 30,500, it is tempting to think that buying near the same zone must still be safe. But the fund and the retail investor are measuring risk differently. A fund may be willing to absorb short-term volatility for the sake of a long-term asset thesis. A late follower may be shaken out within a few sessions if the market does not move on the same timetable.

The price action also says something about valuation psychology. If a stock has already moved before the news becomes widely discussed, the edge for a late entrant no longer comes from knowing the headline. It comes from understanding the business more clearly than the crowd does. With KBC, that means distinguishing between the long-term land-bank story and the part of that story the market has already started paying for.

What Retail Investors Should Check Instead of the Fund Name

In plain terms, KBC becomes more compelling only when land turns into cash. The first thing to track is legal and handover progress. A large land bank does not automatically produce revenue if a project is not yet ready for delivery or if tenants are not signed on the expected timeline. Many new investors underestimate the distance between "owning land" and "collecting money from that land."

The second point is cash-flow quality. Industrial park developers can report attractive accounting profit in a strong handover quarter, but cash flow tells you whether money is actually coming back with enough consistency. If the company still has to commit large sums to infrastructure, clearance, or new development, working-capital pressure and borrowing needs can rise before the next revenue wave shows up. That is not a flaw unique to KBC. It is part of how the business model works. But it remains a real risk for minority shareholders.

The third issue is leverage during the waiting period. A fund can afford to view KBC through a multi-year lens. Retail investors need to ask a more practical question: if execution takes longer than expected, does the company still have enough financial room to stay on track. Industrial park stocks are usually attractive on the asset side. Their vulnerability tends to show up in the rhythm of cash.

That is why the better checklist is no longer "will the fund keep buying." The better checklist is which parts of KBC's land bank are close to generating revenue, whether cash inflow is keeping pace with expectations, and whether debt remains manageable. Once investors change the question, they also change the quality of the conclusion they are likely to reach.

Conclusion: A Better Signal, Not Final Proof

PVI AM makes KBC more worth monitoring. That is the strongest conclusion the evidence supports right now, and it is also the most honest one. The trade shows that institutional capital is willing to raise exposure to the company, and that is rarely meaningless.

But the rest of the story still has to be proven by KBC itself. If the company can accelerate handovers, convert its land bank into revenue on schedule, and keep capital pressure under control, the PVI AM transaction may later look like an early clue. If execution slips or cash flow fails to keep up, the fund's name will not complete the investment case on the company's behalf.

For newer investors, that may be the more valuable lesson than the stock itself. Institutional buying can be the reason to start paying attention. The most persuasive evidence still arrives later, in the financial statements, in project progress, and in actual cash generation. Over the next reporting cycles, those remain the signals worth watching most closely, far more than whether another fund decides to appear.