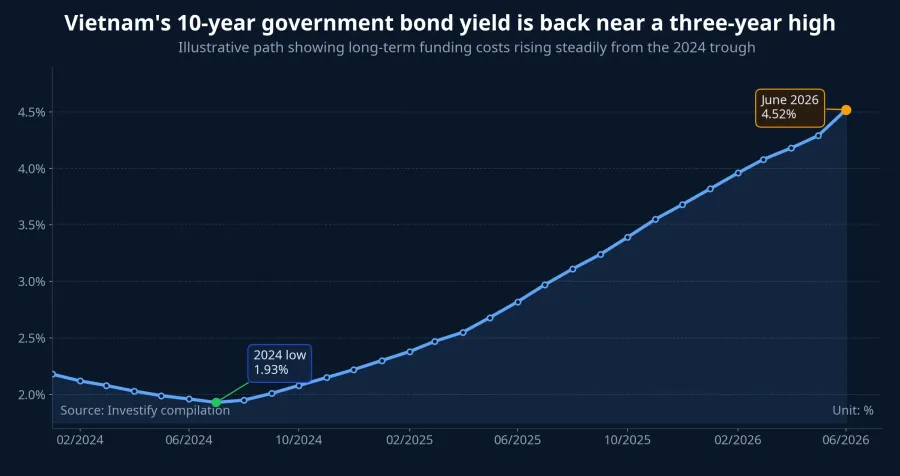

Vietnam’s 10-year government bond yield has climbed to about 4.52%, putting it back near a three-year high.Doanh Nhân VN For many newer investors, that number still feels distant from the things they watch every day, like deposit rates or stock quotes. In practice, though, it is one of the cleanest reference points for how the market is pricing long-term money.

That is why this move matters beyond the bond market itself. A higher government bond yield does not automatically mean a liquidity crisis is underway, but it does mean investors are demanding more return to lock up money for longer. In plain terms, the market is no longer treating long-term capital as cheap.

Why this matters for newer investors

Government bonds sit close to the “lowest-risk” end of the local capital market. If that safer benchmark has to pay more, every riskier asset has to justify itself against a tougher baseline. That includes equities, corporate bonds, and even the way savers think about deposits.

So when parts of the market still talk about cheap money returning soon, the yield curve is sending a more cautious message. Long-duration funding costs are being repriced, and that repricing tends to spill over across asset classes. For retail investors, that is the real takeaway.

This is not a panic signal

If the system were under acute stress, the bond move would usually come with a broader cluster of warning signs: severe funding strain, major dislocations in short-term rates, or widespread auction failures. The evidence in hand does not force that conclusion. A better reading is that buyers have become more selective and want a higher yield before stepping in.

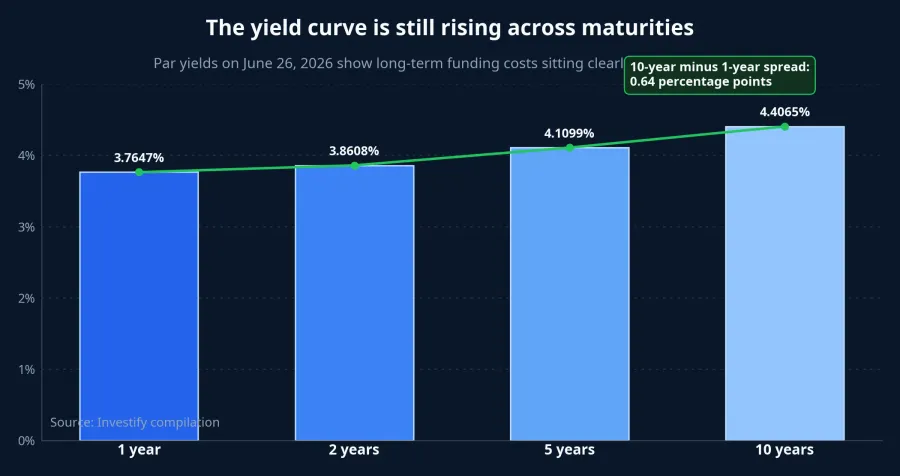

The move is also not just a one-day print. SHS Research, as cited by Doanh Nhân VN, said the 30-year government bond yield was nearing 4.6% per year as of May 28, 2026, while the 10-year was around 4.2% before continuing to rise in later weeks.Doanh Nhân VN Investify’s internal series points in the same direction: as of June 26, 2026, par yields stood at 3.7647% for one year, 3.8608% for two years, 4.1099% for five years, and 4.4065% for ten years.

The gap between the internal 4.4065% reading and the 4.52% market quote is not a contradiction. Those figures can differ because of timing and methodology. The more important point is that both show the same shift: yields have moved materially higher from the lows seen in 2024.

Three forces are pushing yields higher

The first is weaker demand from banks. According to SHS Research, as cited by Doanh Nhân VN, softer primary-market demand, especially from commercial banks, is one of the main reasons yields have risen.Doanh Nhân VN That matters because banks are usually a major source of demand in Vietnam’s government bond market.

Why does that matter so much? When credit growth looks more attractive, or when banks have to manage lending and funding more tightly, they have less incentive to expand long-dated bond holdings aggressively. If a large buyer becomes less active, issuers typically need to offer a higher yield to clear supply.

The second force is that short-term policy liquidity is not especially cheap. The same source said rates on the open market operations channel are around 4.5% per year.Doanh Nhân VN If a shorter and safer channel is already paying that much, longer-dated bonds have to offer enough compensation to attract demand.

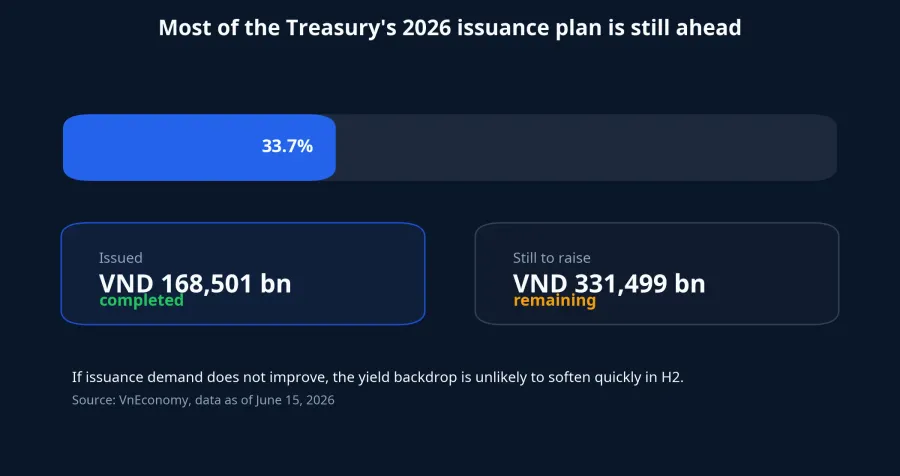

The third force sits on the supply side. VnEconomy reported that Vietnam’s 2026 government bond issuance plan is VND 500,000 billion, but only VND 168,501 billion had been raised by June 15, equal to 33.7% of the annual target.VnEconomy In the second quarter alone, the Treasury had run 11 auctions and raised VND 88,400 billion, or nearly 59% of the revised quarterly plan.VnEconomy

Put simply, the seller still has a lot of bonds left to issue, while the buyer base is not as relaxed as it was during the most liquid periods. That combination does not necessarily create a shock, but it can keep yields pinned at a higher level. For newer investors, the key is to see “higher yields” as a price signal for capital, not as an isolated bond-market headline.

How the pressure spills into equities

The clearest transmission channel is valuation. Once the 10-year yield is sitting around 4.4% to 4.5%, the discount rate used to value future corporate cash flows also becomes harder to keep at old low levels. Stocks priced on distant growth, or on profits that are still far in the future, tend to be more sensitive to that change.

That does not mean all equities have to fall. The VN-Index closed at 1,871.91 on June 26, above its January 5 level of 1,788.40. But the VN30 closed at 2,008.57 on June 26, slightly below its January 5 reading of 2,028.68. For retail investors, that is a useful reminder that a rising market headline does not mean large-cap valuations are getting an easy ride in a higher-cost-of-capital environment.

It is also important not to overstate causality. Higher yields are not the only reason behind large-cap performance; sector rotation, earnings expectations, and portfolio rebalancing may all matter. Still, the evidence is strong enough to say that the new yield backdrop is making valuation less forgiving.

What it means for corporate bonds and deposits

For corporate bonds, higher government yields raise the base cost of borrowing. A company issuing debt has to pay for its own credit risk on top of a safer benchmark that is already more expensive than before. That makes it harder to argue that long-term funding can remain as cheap as it was in earlier phases of the cycle.

For deposits, the story is closer to household cash decisions. If banks still need to retain funding and market yields have not cooled meaningfully, deposit rates are unlikely to drop quickly. That helps savers in the short run, but it weakens the broader narrative that cheap money will soon return and lift every asset class at once.

The simplest way to think about this is relative pricing. When the safer asset pays more, investors become stricter with riskier assets and ask whether the expected return is really enough to compensate for added volatility. That question is the bridge connecting government bonds, deposits, equities, and corporate debt.

What to watch next

Rather than staring at the 4.52% headline alone, retail investors should watch two sets of signals over the next few weeks. The first is government bond auction results. If auction demand improves without another leg up in yields, pressure may be starting to ease. If the Treasury still needs to pay up to place meaningful volume, the market is saying buyers are not ready to accept a lower yield regime yet.

The second is short-term liquidity conditions. If OMO rates and system liquidity cool more clearly, the case for cheaper money becomes more credible. If short-term conditions stay firm, longer-dated yields usually struggle to fall quickly in a durable way.

That leaves a fairly clear conclusion. Higher government bond yields are not a crisis signal, but they do not support the idea that cheap money is about to return quickly either. For newer investors, the more useful response is not to avoid every risky asset. It is to re-read valuations, re-check return assumptions, and accept that the market’s cost-of-capital benchmark is now sitting on a higher floor. Over the next two weeks, the most useful checkpoints are bond auction outcomes, OMO conditions, and whether the 10-year yield stays anchored around the 4.4% to 4.5% area.