One red month is often enough to trigger a simple conclusion: equity funds fell, money kept leaving, so the fund channel must be weakening. That conclusion is understandable, especially for first-time investors. It is also incomplete. A bad month in equity funds does not automatically mean the product is deteriorating. More often, it shows that investors are using the wrong benchmark for something that still holds stocks underneath the wrapper.

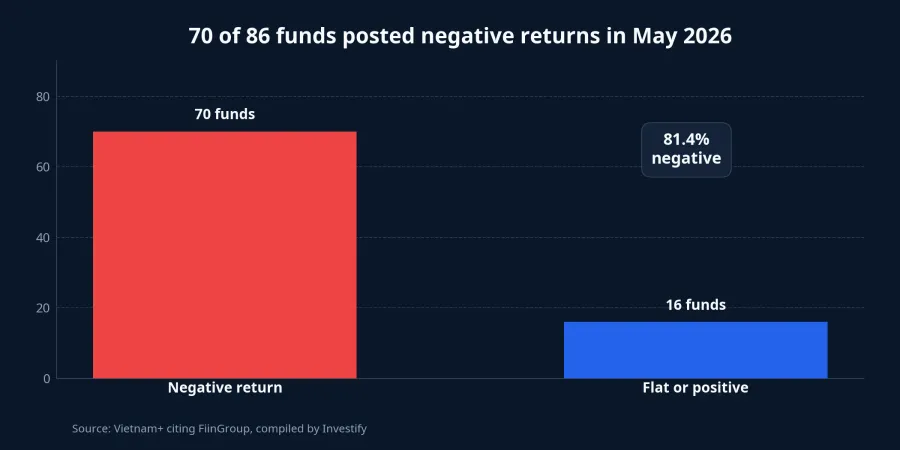

Vietnam+ cited FiinGroup data showing that 70 out of 86 funds posted negative returns in May 2026. Equity funds fell by an average of 1.4%, total net outflows from the fund market topped VND 2.5 trillion, and equity funds alone saw more than VND 1.8 trillion in net withdrawals. The same report described May as the 31st straight month of net outflows for equity funds.Vietnam+

Those numbers are strong enough to justify concern, but not strong enough to convict the entire fund market. To read them properly, investors need to separate three different layers: what the market itself is doing, how portfolio managers are responding, and how fund holders behave when short-term returns turn negative. Once those layers are collapsed into a single headline such as “funds are doing badly,” the analysis becomes emotionally neat and analytically weak.

An equity fund is still an equity product

That sounds obvious, but it is exactly where many beginners go wrong. Buying a fund means outsourcing stock selection. It does not mean removing stock-market volatility from the experience. Investors buy the manager's process, not a promise that the NAV will stay smooth every month.

When the market swings, an equity fund's NAV can fall. A manager can raise cash, cut exposure to riskier sectors, or stick to a longer-term allocation instead of trading every short-term move. None of those choices changes the nature of the product. If an investor expects an equity fund to capture upside while avoiding most down months, the mismatch begins before performance is even measured.

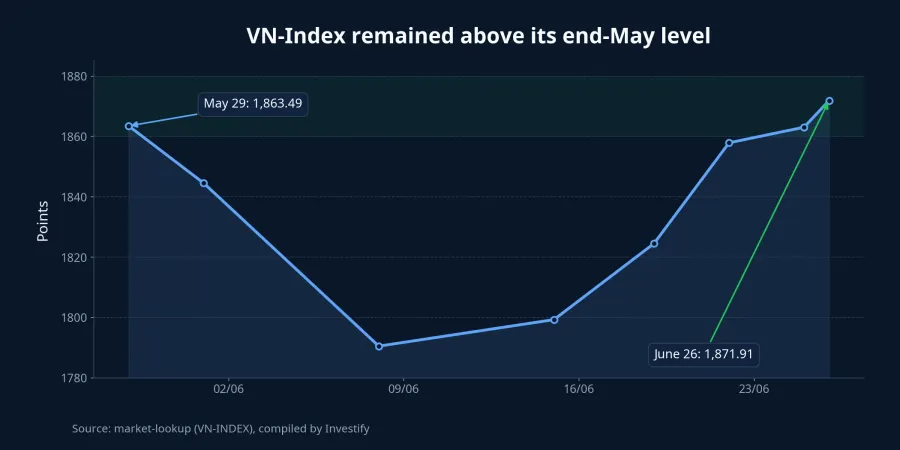

The recent market backdrop makes that point clearer. VN-Index closed at 1,863.49 on May 29 and stood at 1,871.91 on June 26, so the benchmark was still above its end-May level after an early-June pullback. That is not the profile of a market collapse. It is the profile of a selective market, where headline index resilience can coexist with weakness in large parts of the underlying universe.

That distinction matters. The useful question is not “Why are funds red if the index is still elevated?” A better question is whether the fund is lagging because of broad market weakness, because its holdings differ from the sectors lifting the index, or because the strategy itself is misfiring. Those are three very different diagnoses, and only one of them points to a real product problem.

Redemptions reflect investor behavior before they reflect product quality

The VND 1.8 trillion-plus withdrawn from equity funds is a real signal, but it is not automatically a quality judgment. Outflows start as investor decisions, and investor decisions are often driven by discomfort. When the NAV turns negative, short-term holders want relief. When safer assets look easier to hold, capital rotates away from products that ask for more patience.

That dynamic is especially relevant for new investors. Many buy funds because they want professional management but still expect a smoother ride than direct stock ownership. The first half of that belief is reasonable. The second half is where trouble starts. A good fund manager is not someone who prevents every drawdown. A good manager is someone who runs a consistent process that produces a sensible result over a long enough horizon.

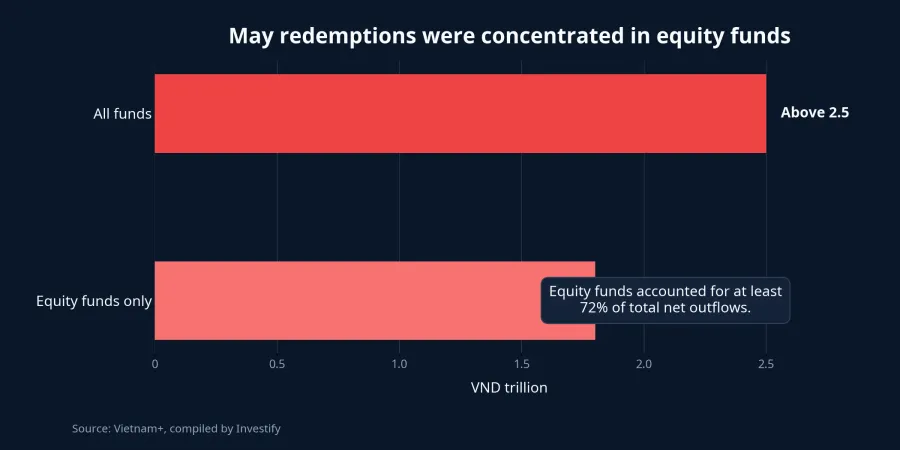

Vietnam+ reported that total fund-market outflows exceeded VND 2.5 trillion in May, with equity funds accounting for more than VND 1.8 trillion of that amount.Vietnam+ When the most volatile category absorbs most of the withdrawals, the cleanest explanation is not “funds failed.” It is that holders are cutting their own risk tolerance after a weak stretch.

That does not mean outflows should be ignored. If one fund is losing assets much faster than peers over several months while also lagging its benchmark and its peer group, that is a genuine warning sign. But that is a different test. It requires persistence, comparison, and context. A single bad month is too thin a record to support a broad verdict.

The benchmark has to match the product

The simplest way to frame the issue is this: each fund category has a different job. Equity funds are built for long-term growth and therefore come with larger short-term fluctuations. Bond funds are designed for more stability, with a different return profile. Balanced funds sit somewhere in the middle, blending growth and defense rather than maximizing either one.

The problem is that many new investors ask the same question of all three: “Was it red this month?” If that becomes the only scorecard, equity funds are almost guaranteed to disappoint at some point. A negative month in an equity strategy can be entirely normal. The more relevant test is whether the fund is doing what it said it would do relative to its stated mandate, its benchmark, and its peers.

For equity funds, four checks matter. First, is the intended holding period long enough? Investors who enter an equity fund expecting stability within three to six months are setting themselves up for frustration.Vietnam+ Second, is the fund genuinely underperforming its benchmark, or merely failing to meet the investor's emotional expectation of smoothness? Third, do the portfolio holdings match the investor's actual tolerance for sector and style risk? Fourth, is the decision to redeem driven by a real change in financial goals, or just by the discomfort of a temporary drawdown?

Once those questions are answered honestly, fund decisions become much less reactive. An investor who needs cash in the near term, or who realizes that equity volatility is simply too hard to hold, may be right to reduce exposure. But redeeming solely because one monthly report was negative, while the whole category is under pressure, is usually a behavioral response rather than a disciplined investment review.

What the data is really saying

The core takeaway is straightforward: May did not prove that the fund channel is getting worse. It showed that many investors entered equity funds with expectations that looked closer to deposits or low-volatility savings products than to long-horizon equity allocation. That expectation gap matters more than one weak month.

So the evidence points in one direction. Negative returns and continued outflows deserve monitoring, but they are not enough to condemn the product category. A more serious warning would require several quarters of weak results, repeated benchmark underperformance, or a visible breakdown between stated strategy and actual portfolio behavior. That is not what the current evidence establishes.

For beginners, the most durable framework remains basic but effective: understand the fund's objective, choose a holding period that matches the product, and compare performance with the right benchmark. If those three elements still line up, a red month in NAV is something to interpret, not an automatic exit signal. The next useful checkpoints are simple: how the fund performs over the next few months, whether it tracks its benchmark more consistently, and whether redemptions remain concentrated in equity funds.