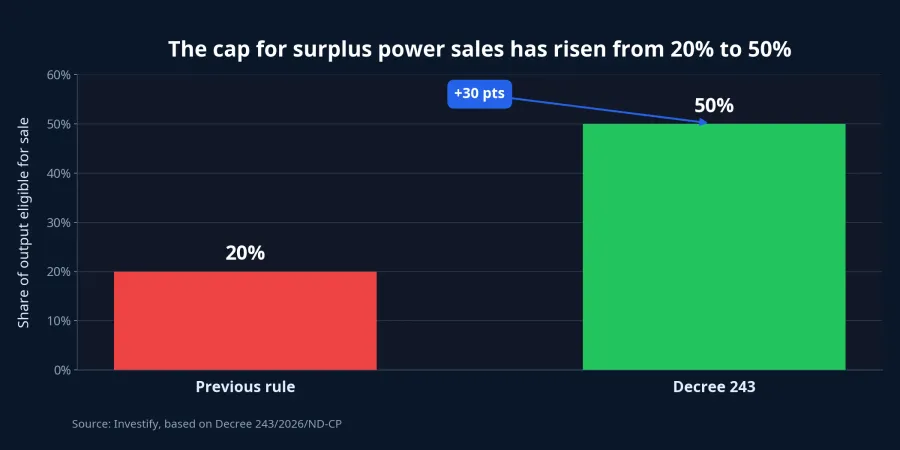

The 50% figure in Decree 243/2026/ND-CP is the kind of number that can instantly change investor sentiment. If surplus rooftop solar power used to be capped at 20% of output for grid sales and can now go up to 50%, the intuitive conclusion is simple: payback periods should fall sharply. That conclusion is directionally right, but only partly so.VOV

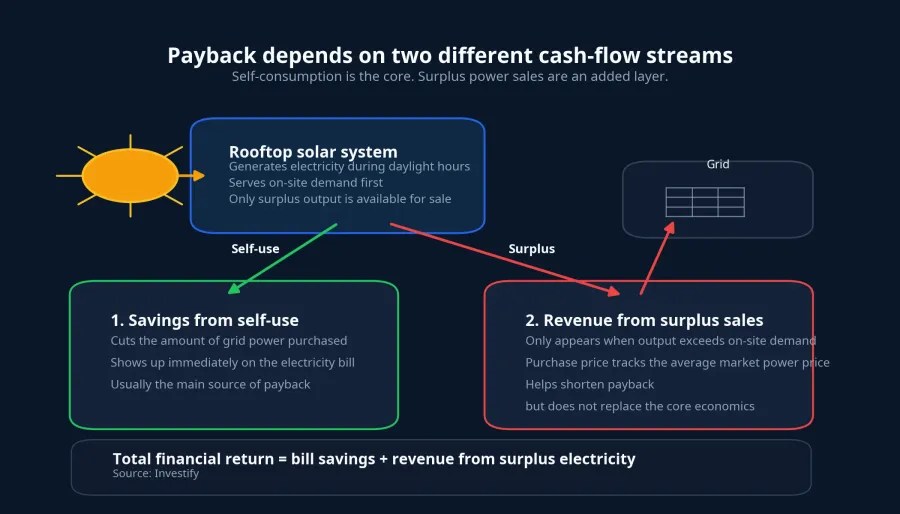

What has changed is the margin of safety in the investment math. What has not changed is the core engine of returns. Rooftop solar designed for self-consumption still makes the most money by reducing electricity purchased from the grid. Selling excess power helps. It does not replace that logic.

What Decree 243 Actually Changed

The headline change is straightforward. Under the new framework, self-produced and self-consumed rooftop solar systems can sell surplus output equal to as much as 50% of generated electricity at the point of output, up from the previous 20% cap.VOV For someone who has never modeled a rooftop solar installation, that may sound technical. For a household with a heavy power bill or a factory operating during daylight hours, it goes directly to capital recovery.

Under the old 20% ceiling, system sizing had to be conservative. Oversizing a rooftop meant a higher chance that midday output would exceed on-site demand and leave too much electricity stranded. A 50% ceiling gives owners more room to size a system slightly above current daytime usage without wasting as much surplus generation.

But the policy is still built around self-consumption first and sales second. That hierarchy matters. If readers interpret Decree 243 as a return to a “build to sell power” rooftop model, they are reading a different policy from the one actually published.VOV

Why a 50% Ceiling Does Not Automatically Transform Payback

The biggest source of confusion is the phrase “more surplus can be sold.” More saleable power does not mean every extra kilowatt-hour is worth as much as a kilowatt-hour used on site. Those are two different cash-flow streams.

When power is consumed on site, it displaces electricity that would otherwise have been bought from the grid. The benefit shows up directly in the electricity bill. When power is exported, it generates revenue under the surplus power purchase formula. That is why self-consumption remains the center of the payback equation even after the sales ceiling moves from 20% to 50%.

There is another important point: Vietnam is not returning to the old fixed feed-in tariff regime that powered the earlier rooftop solar boom. According to Thanh Nien, the purchase price for surplus electricity is tied to the previous year's average market power price, with the 2025 benchmark at VND 844.8/kWh for use in 2026.Thanh Niên That means exported power is a supplemental revenue stream, not an exceptionally rich one.

Another report notes that if the average market power price is above the maximum level in the pricing framework for ground-mounted solar without storage, the purchase price for surplus rooftop power is capped at that maximum, excluding value-added tax.Người Đưa Tin In plain English, surplus sales improve returns, but they come with a formula and a ceiling. That makes the project math better, not magically easy.

Who Benefits First

If you start from cash flow rather than headlines, the clearest winners are not necessarily those with the biggest roofs. The more attractive use cases are the ones that combine three features at once: enough roof area, strong daytime electricity demand and a workable grid connection.

Factories are the cleanest example. If machinery runs through the day, much of the solar output is consumed immediately on site. In that case, the main financial gain comes from lower grid purchases. If there is still excess output, the 50% threshold gives the project another layer of support and can shorten payback further. That is why the same policy can look far more compelling for an industrial user than for a household.

The opposite case is also important. A household that is empty for most of the day may generate a meaningful amount of excess power during peak sunlight hours. In that scenario, returns depend more heavily on the purchase price for surplus electricity and on whether the local system can absorb the power. The number of panels matters, but the consumption pattern matters more.

This is where new investors often misread the story. Many people instinctively treat every asset as if the goal were simply to find the one that “goes up faster.” Rooftop solar is closer to a cost-saving project with an attached revenue tail than to a speculative trade. The stronger the daytime self-use profile, the sturdier the payback case.

The Real Bottleneck Is Still the Grid

Decree 243 also leaves room for flexibility. From the effective date of the decree through December 31, 2030, parties may negotiate surplus sales above 50% if the local grid can absorb the power and if the arrangement meets grid safety and system operation conditions.VOV

At first glance, that sounds like an even more bullish provision. In practice, the conditions matter more than the headline. The right to sell more power depends not only on the rooftop system itself, but on the receiving capacity of the local grid. If many systems export heavily at the same time, grid constraints can become the binding factor.

That is the difference between a more favorable policy and a guaranteed economic outcome. The decree expands the opportunity set. It does not promise that every location can use the full opportunity immediately. For investors, the disciplined reading is to treat 50% as an improved condition, not as a guaranteed result.

Do Not Turn a Policy Story Into a Stock Story Too Quickly

Markets have a habit of turning any new rule into an instant hunt for listed winners. In this case, that shortcut can obscure the more important point: different businesses benefit through very different channels.

Installers, equipment distributors, industrial parks trying to lower energy costs and firms with large factory-owner customer bases may all gain from the decree, but not in the same way and not on the same timeline. Some only benefit if orders rise. Others need margin expansion. Some require proof that installations are actually accelerating on the ground before the earnings story changes in a material way.

That is why the jump from a new decree to “solar stocks will all rerate” remains unsupported. The source article does not establish that any specific company has already secured more orders or stronger profitability because of the new rules. The safer conclusion is narrower: Decree 243 improves the investment case for rooftop solar systems, while the equity impact still needs operating evidence.

Bottom Line

If this needs to be reduced to one sentence, Decree 243 makes rooftop solar financially easier to justify, but it does not make every project equally good. The key improvement is that more surplus output can now be monetized. The factor that still decides whether payback is fast or slow is how much electricity is consumed on site, during which hours and at what connection point.

For newer investors, the better question is not “who gets the first trading wave,” but “which operating model produces the most reliable cash flow.” Three signals are worth watching next: actual installation activity among factories, how surplus power pricing is implemented in contracts and how much receiving capacity local grids really have. Those are the variables that will determine whether the better policy framework becomes better real-world economics.