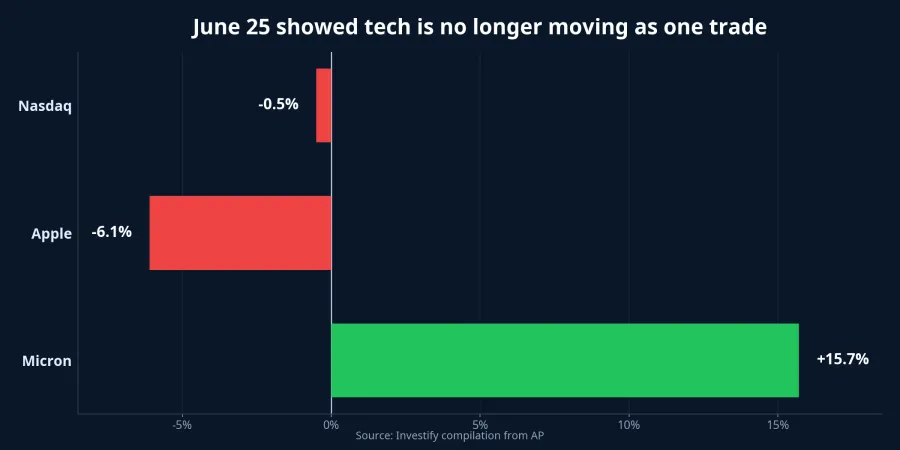

On June 25 in the U.S., Micron jumped 15.7%, Apple fell 6.1%, and the Nasdaq Composite still slipped 0.5%. APAP Those moves happened in the same trading window, so this is not a timing illusion. What the market is doing instead is separating technology into different business models: companies selling what the market urgently needs are being rewarded, while companies absorbing higher input costs are being repriced.

That matters because many retail investors still read “tech” as one growth trade. In looser market conditions, that shortcut can work for a while. Once valuations are high and investors become less generous, the questions change. Where is the profit showing up right now? Where is the cost pressure landing? And which companies can pass that pressure on without damaging demand?

Why Micron was rewarded

At a basic level, Micron sits closer to the supply side of the boom. It sells memory and storage, the components data centers need immediately when AI infrastructure spending accelerates. That means investors are not only hearing a long-term story. They are seeing current-quarter proof that the story is already feeding through into revenue and profitability.

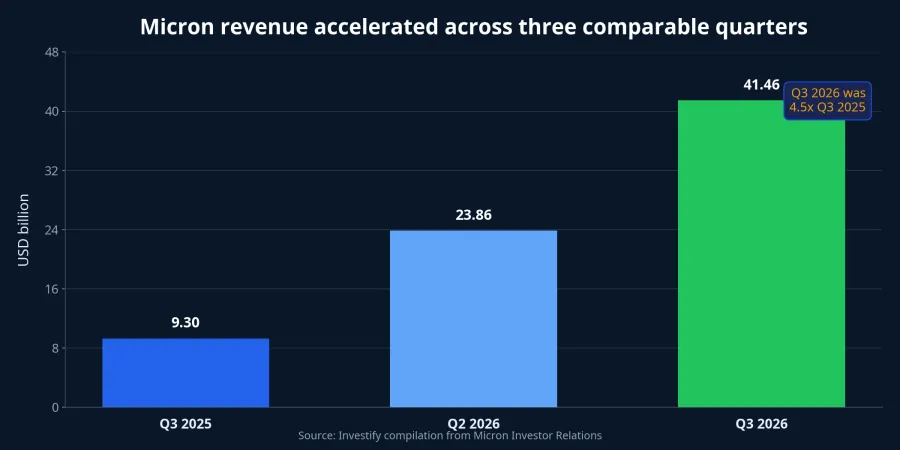

Micron reported fiscal third-quarter 2026 revenue of USD 41.46 billion for the quarter ended May 28, up from USD 23.86 billion in the prior quarter and USD 9.30 billion a year earlier.Micron GAAP net income came in at USD 28.24 billion, while adjusted EPS reached USD 25.11.Micron That gives investors a concrete basis for arguing that the stock’s rally is not resting on a vague promise alone.

The more important detail is the quality of the growth. Micron’s adjusted gross margin rose to 84.9%, up sharply from 39.0% in the same quarter last year.Micron When a company expands revenue and margins at the same time, the market treats that very differently from a company that grows sales while absorbing cost pressure.

For newer investors, this is the real lesson. A rising stock price does not automatically mean the market is bullish on an entire sector. In periods when valuations are under scrutiny, capital tends to flow toward the companies with the clearest near-term earnings visibility. Micron is being rewarded because the latest quarter gave investors hard evidence that the narrative is already producing cash and margins.

Why Apple was discounted

Apple sits on the other side of the same chain. It does not sell memory; it buys components, assembles devices, and sells them to consumers. When memory and storage costs rise, Apple faces a harder trade-off. If it holds prices steady, margins can compress. If it raises prices, demand may slow.

On June 25, Apple raised prices on a range of MacBook and iPad models. MacBook Air 512GB moved from USD 1,099 to USD 1,299, MacBook Pro 1TB from USD 1,699 to USD 1,999, iPad Air 128GB from USD 599 to USD 749, and the 256GB Wi-Fi version of the iPad Pro from USD 999 to USD 1,199.VietnamFinance From a pure accounting standpoint, higher prices help defend margin. In equity terms, however, the move introduces a bigger question: will customers accept the new price points without pulling back?

That is why Apple’s 6.1% drop should not be read as a reaction to a price sheet alone.AP The stock sold off because investors can now see pressure on both ends of the model. Without price increases, margin takes the hit. With price increases, demand becomes the risk, especially for consumer electronics that are often discretionary rather than essential.

This is where newer investors often over-simplify the logic. “Raising prices” does not automatically mean “good for profits.” In consumer hardware, purchasing behavior depends on replacement cycles, disposable income, and confidence. If any one of those weakens, a price increase can protect margins on paper while hurting unit demand in the following quarters.

The Nasdaq decline says the good news is not broad enough

If investors were still treating technology as a single block, Micron’s results might have been enough to lift overall sentiment. That is not what happened. The Nasdaq Composite dropped 118.03 points, or 0.5%, to 25,358.60, while the Dow Jones Industrial Average still added 71.72 points.AP In other words, strong numbers from one company were not enough to offset broader valuation pressure across the group.

For retail investors, that is a practical signal rather than a dramatic one. In a highly selective tape, sector labels lose forecasting power. Technology stocks are no longer being priced as one bundle that rises together because they share a macro theme. The market is pricing business models, supply-chain position, and the ability to convert top-line growth into durable earnings.

AP also reported stronger reactions in Asian markets with large semiconductor exposure, with South Korea’s Kospi up 5.4% as SK Hynix rose 13.1%, while Japan’s Nikkei 225 gained 4.6%. AP But that does not mean Vietnamese investors can import the same logic wholesale into domestic equities. Vietnam does not yet have a listed semiconductor structure large enough to mirror that response directly.

What Vietnamese investors should watch

On June 25, FPT closed at VND 71,000 per share, up 0.28%, while CMG ended at VND 27,050, down 0.18%. The VN-Index closed at 1,863.07 points, down 0.80%. Those figures do not prove that Vietnam’s technology names will follow either Micron or Apple, but they do reinforce an important point: the domestic market has its own rhythm, and each company still has to be read on its own numbers.

For newer investors, the better question is no longer “is tech still attractive?” The better questions are these. Which revenue has already been booked? Are margins holding? Do new contracts create near-term cash flow or mostly support a distant narrative? How much future growth is already embedded in the valuation, and is that expectation being supported by quarterly results?

In a more selective market, companies with a good story but no visible earnings are usually the first to be challenged. By contrast, companies that can already show orders, margins, or a clearer conversion from revenue to cash tend to have sturdier footing when global risk appetite turns choppy.

The more defensible conclusion is that technology itself has entered a more selective phase. When visible earnings supported Micron, the stock was rewarded. When cost pass-through became the issue for Apple, the stock was discounted. For Vietnamese investors, that is the useful reminder to carry into every growth name: sector identity is no longer enough to substitute for reading revenue, margins, and the resilience of final demand.

Over the next one to two weeks, the signals worth watching are the pace of quarterly reporting from major technology companies, how share prices react to each release, and whether consumers absorb higher device prices without a visible slowdown.