At first glance, a 6.5% annual loan rate sounds like exactly the kind of policy that could bring home ownership closer for younger buyers. That reaction is understandable. From July 1, 2026 through December 31, 2026, borrowers under 35 who buy social housing will receive a 6.5% annual rate in the first five years from the initial disbursement date; for the next 10 years, the applicable rate will be 7.5% annually.VOV But a cheaper loan is only the price of money, not a guarantee that a buyer can actually get a unit. In practice, three gates still have to open in sequence: an eligible project, compliant paperwork and bank approval.Vietnam.vn

The policy clearly changes one variable: Funding cost

The first point is worth stating plainly: this is not a cosmetic adjustment. The 6.5% annual rate in the first five years is 2 percentage points below the average medium- and long-term VND lending rate at Agribank, BIDV, Vietcombank and VietinBank. The 7.5% annual rate in the following 10 years is 1 percentage point lower.VOV For actual buyers, that matters because it lowers the monthly repayment burden during the most fragile stage of the borrowing cycle.

Many younger households do not fail the home-buying test because they have no income at all. They fail because their monthly cash flow does not look stable enough for a bank to believe the loan can be serviced over a long period. Lower rates ease part of that pressure, but they do not automatically loosen project availability, eligibility checks or approval timelines.

Disbursement data shows the bottleneck lies elsewhere

If rates were the main obstacle, a large headline credit package should have moved much faster already. According to a Tuổi Trẻ report republished by Vietnam.vn, as of January 31, 2026, only about VND 8,293 billion had been disbursed from the VND 145,000 billion social housing credit package, equal to roughly 5.7% of the total package size.Vietnam.vn That ratio alone forces a more useful question: if the money exists, why is the flow still so slow?

The answer is that social housing disbursement does not work like a broad consumer credit promotion. Buyers must first find a project that is legally available for sale, prove that they qualify for the policy, complete housing and income paperwork, and then pass bank credit review like any other home loan applicant.LuatVietnam Slow disbursement does not automatically mean the policy lacks appeal; it means the path from policy design to a signed apartment contract still contains a lot of friction.

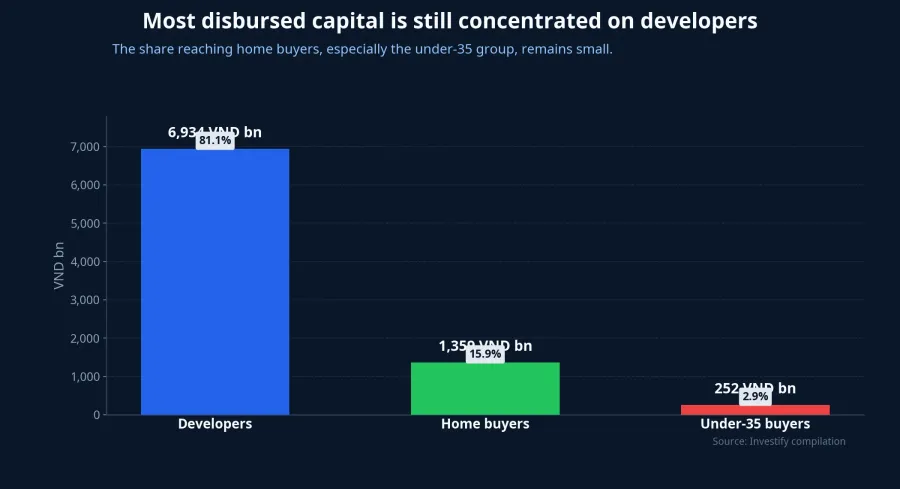

Most of the money is still flowing to developers

One layer deeper, the structure of disbursement tells an equally important story. Out of the roughly VND 8,293 billion already disbursed, about VND 6,934 billion went to developers, around VND 1,359 billion went to homebuyers, and only about VND 252 billion reached the under-35 segment.Vietnam.vn

That matters for anyone waiting for the July 1 policy start. Capital going to developers is necessary because projects need financing before homes exist, but from the buyer's point of view, access widens only when a project is eligible for sale, the file is complete, and the bank signs off. The under-35 disbursement figure of roughly VND 252 billion suggests many younger applicants still get stuck on initial savings, credit history or income stability.

Supply is still the first gate

Many prospective buyers instinctively start with the question, "How much can I borrow?" In social housing, the more useful first question is, "Is there an eligible project where I actually live or work?" VietnamNet reported that Hanoi's Department of Construction has just published a list of 13 proposed social housing projects with more than 54 hectares of land in total. The same report said the Ministry of Construction has urged local authorities to speed up land allocation, funding and the launch of at least one budget-backed rental housing project during June 2026.VietnamNet

That is a constructive signal, but the timing still matters. A proposed project is not the same thing as an apartment ready for contract signing, and a groundbreaking is not the same thing as a live sales phase. If that gap does not narrow, the emotional effect of a lower rate will run much faster than real transactions.

That is why buyers should track supply as closely as they track interest rates. A cheaper loan creates value only when it meets enough supply in the right locations at the right stage of development.

Paperwork and bank review remain the last gates

Under the current rules summarized by LuatVietnam, social housing buyers must belong to an eligible beneficiary group, meet the housing conditions, and complete the required documentation. On the housing-status side, the applicant must not own a home in the locality where the project is located and must not previously have bought or rent-purchased social housing. If the household already has housing, the average usable floor area must not exceed 15 square meters per person.LuatVietnam

The process itself is also not short. The developer prepares a list of expected buyers and submits it to the local Department of Construction for review. If there is no response after 20 working days, the buyer can then be notified to sign the contract. Each household or individual may register for only one project.LuatVietnam In practice, that means buyers need not only to be eligible, but to prepare a clean file from the start so they do not lose time or miss the window.

After paperwork comes credit review. Banks will still examine actual income, current debt obligations, credit history and income stability. A lower rate makes the monthly repayment lighter, but it does not replace the core requirement that the borrower must still prove the loan can be repaid over many years.

What matters after July 1

If the whole story has to be reduced to one line, it is this: 6.5% is a better key, but not yet a wider door. The new policy meaningfully lowers financing cost, and that is a real improvement. But the available evidence still points to eligible project supply, buyer paperwork quality and bank readiness to disburse as the factors that will decide how quickly access actually improves.

For anyone weighing a purchase, the next few weeks should not be judged by the rate table alone. The more important signals are how many projects truly move into the application stage, whether local processing time becomes shorter, and whether the share of disbursement going to end buyers rises materially after July 1. If those three indicators improve together, the 6.5% rate will start to deliver its full meaning. If the rate changes while everything else stays in place, the feeling that homes are more reachable will still arrive more slowly than the headlines suggest.