On the morning of June 25, VN-Index slipped to 1,861.84 after closing at 1,878.02 in the previous session. On the surface, that is still a strong enough level to make the market look healthy. But if you are a new investor opening your app and wondering why your portfolio still feels heavy, that reaction is not irrational at all.

The simplest way to frame it is this: VN-Index measures the weight of large-cap stocks, while many retail portfolios are concentrated in mid-caps, smaller names, or stock-specific stories. When those parts of the market do not rise together, the index can look strong even as real portfolios struggle to recover. The issue is not that the market is “fake.” It is that investors are using a highly aggregated benchmark to judge a very personal P/L experience.

The central thesis is straightforward. The market is not weak, but the upside is still concentrated in a narrow slice of the board. That is why retail investors who rely on VN-Index alone can easily misread the market’s true tone and set expectations that do not match the stocks they actually own.

Why the index can rise while your account does not

The first point to remember is that VN-Index is not built like an equally weighted portfolio. The larger the company, the more power it has to move the benchmark, so a sharp gain in one heavyweight can offset a long list of flat or mildly negative stocks elsewhere. A useful analogy is a class average: VN-Index is the class score, while your portfolio is the result in only a few subjects. A green benchmark therefore does not mean most of the market is moving in your favor.

Mechanism one: Index gains are concentrated in a few heavyweights

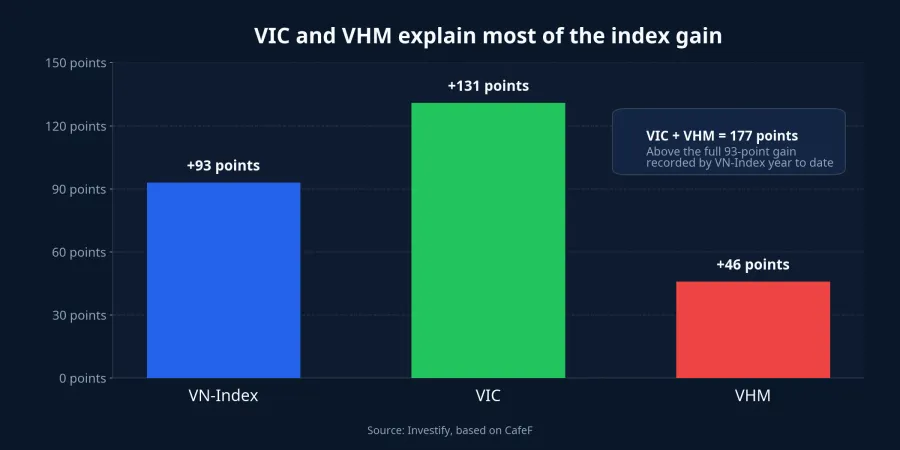

CafeF reported that from the start of the year to June 24, VN-Index gained 93 points. But VIC alone contributed 131 points, while VHM added another 46 points. Together, those two stocks accounted for 177 points, more than the full rise of the benchmark itself.CafeF

For newer investors, the takeaway is simple. The cleanest part of the headline is being created by a very narrow cluster of stocks. If you owned the right heavyweights, the year may look comfortable. If your holdings sit outside that zone, your lived experience can be very different even while you are looking at the same VN-Index.

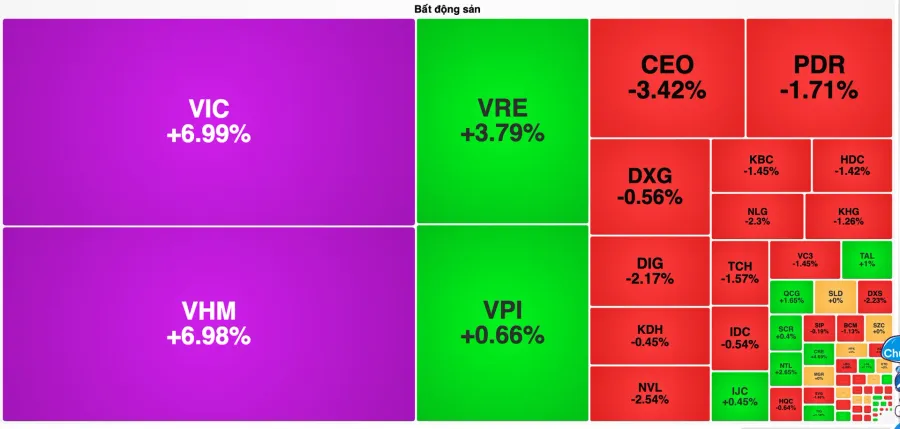

CafeF also noted that after VIC and VHM, other major contributors such as BSR, LPB, GAS, VCB, and GVR added only around 10 to 15 points each year to date.CafeF That gap shows just how concentrated index leadership has become. A headline that says “the market is up” may be factually correct at the benchmark level while still missing the reality inside many portfolios.

Mechanism two: Market breadth still does not confirm a broad advance

If the index tells you where the heavyweights are going, market breadth tells you how many stocks are actually moving with them. For retail investors, that is often the more useful indicator because it sits much closer to day-to-day portfolio experience.

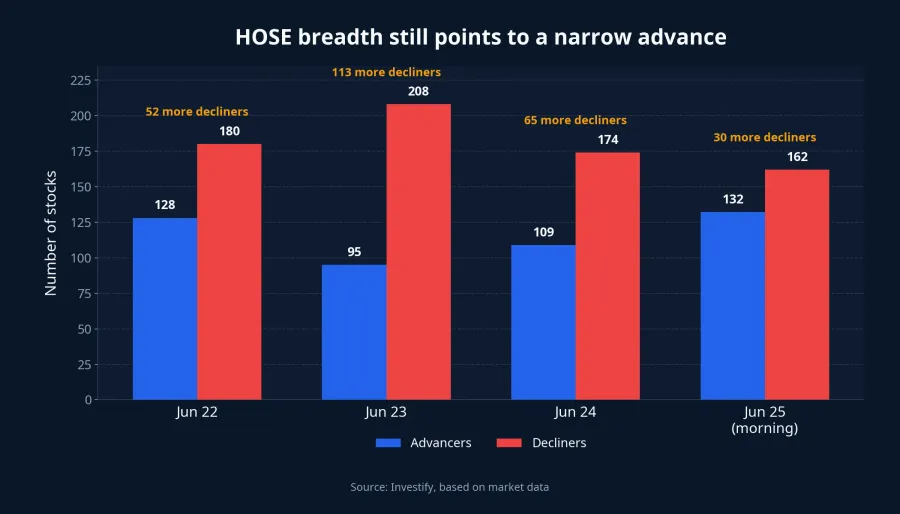

The last three sessions before the morning of June 25 show that breadth remains skewed. On June 22, VN-Index rose to 1,857.91, yet HOSE still had 180 decliners against 128 advancers. On June 23, the index edged up to 1,869.04 while decliners reached 208 and advancers were only 95. By June 24, VN-Index closed at 1,878.02, but HOSE recorded just 109 advancers against 174 decliners. On the morning of June 25, the index eased to 1,861.84 with 132 advancers and 162 decliners.

Those numbers matter because they explain why the board can feel disconnected from the headlines. A genuinely broad-based market usually comes with advancers outnumbering decliners, stronger liquidity across sectors, and recoveries that show up beyond a handful of mega-caps. When the index rises while decliners still dominate, the move is more likely being driven by leaders than by a market-wide expansion in risk appetite.

This is where many first-time investors get tripped up. They see a green benchmark and assume the whole market is healthy, then expect their own portfolio to reflect that strength. But when breadth does not support the move, the more accurate reading is that money remains selective. The market may be stable at the index level without being easy at the stock-picking level.

Mechanism three: Your reference point is different from the index’s

There is also a psychological mismatch at work. Financial headlines compare the market to a benchmark level, while investors compare their portfolios to their own entry price. If you bought stocks during a more euphoric phase, you do not really care how many points VN-Index has rebounded from a recent low. You care whether your holdings have reclaimed your cost basis, whether liquidity is improving, and whether money is actually returning to your segment of the market. That is why investors can read positive news about the index and still feel no real relief in their accounts.

What retail investors should watch beyond VN-Index

The first indicator is the balance between advancers and decliners. If the index is green but decliners still dominate, you are likely looking at leadership from a few heavyweights rather than a healthy market across the board. The next two are sector liquidity and point contribution. Is capital spreading into brokers, steel, retailers, and second-tier property names, or is it still circling only around a few leaders? When a handful of stocks create most of the benchmark’s movement, VN-Index still matters for overall sentiment, but it is not enough on its own.

The final indicator is the condition of the stocks you actually own. A name that has gone sideways for weeks while liquidity fades does not become healthy just because the benchmark adds a few more points. By contrast, a stock reclaiming an old base on better turnover may tell you more about your own money than the benchmark’s intraday move does.

A more useful way to read this market

It helps to think of the current market as a two-story building. The top floor is the index, where large-cap names are still creating a relatively constructive picture. The lower floor is breadth, where a much larger part of the market has yet to receive the same support. If you only stand on the top floor, the view looks brighter than the reality experienced by many accounts.

That is why the cleaner conclusion is not that the market is weak, but that it remains narrow. The upside has not disappeared, yet it is still concentrated in a limited set of leaders and has not spread widely enough to feel comfortable for most retail investors. In other words, the important question is not simply how close VN-Index is to a peak. It is whether the rest of the board has started to move with it.

Over the short term, the signals worth tracking are still breadth, liquidity spread, and the point contribution of the major leaders. If those three improve together, retail portfolios have a better chance of catching up to the optimistic story the benchmark is telling. If the index keeps rising while breadth stays weak, the gap between market headlines and investor experience will remain in place.