The Fed has finished its annual stress test for 32 large US banks, and within hours JPMorganChase unveiled a new USD 50 billion share repurchase program. Those two headlines belong together: when capital remains comfortably above the safety floor even after an extreme downturn scenario, the market stops asking whether banks can survive and starts asking how much excess capital can be returned to shareholders.FedJPMorgan

For newer investors, this is a useful case study in how bank stocks are actually read. A supervisory release from the Fed can sound remote and technical, but the equity implication is straightforward: will capital requirements tighten, can dividends rise, and is there still enough room for buybacks. Once you read the story through that lens, a Wall Street regulatory update becomes much easier to connect to price action.

What the Fed stress test is really measuring

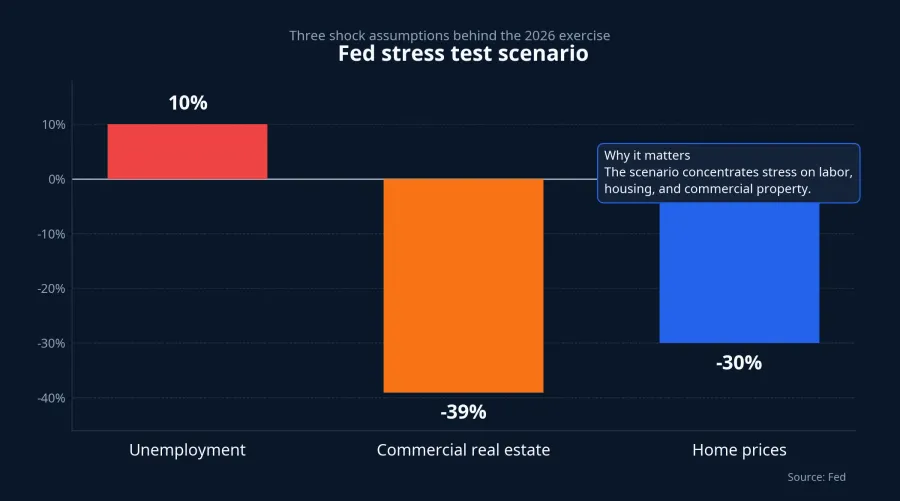

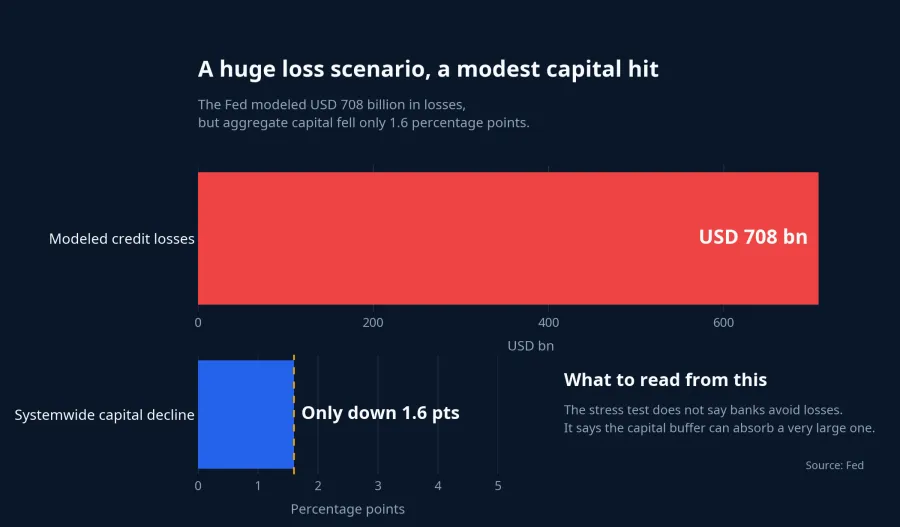

At its core, the exercise is a simulation of a deep recession designed to test whether the banking system can keep standing. The 2026 scenario pushes unemployment to 10%, assumes a 39% drop in commercial real estate prices, a 30% decline in home prices, and more than USD 708 billion in total credit losses across the system.Fed This is not the Fed's official forecast for the US economy. It is a deliberately harsh balance-sheet stress scenario.

The key takeaway is where the exercise ends. The Fed said all 32 banks remained above their minimum common equity tier 1 requirements even after the modeled shock, while aggregate capital across the group fell only 1.6 percentage points.Fed That does not mean banks would avoid losses in a real downturn. It means the capital buffer still looks thick enough to absorb a very large one.

That distinction matters because banks are not priced like ordinary companies. A manufacturer can suffer weak earnings for a few quarters without immediately sparking fears about its ability to function. Banks operate with leverage and confidence at the center of the business model. Once investors begin to doubt the quality of assets or the ability to absorb losses, pressure can build quickly. That is why stress-test results are read as a measure of capital depth, not just as another regulatory box-checking exercise.

Why the market immediately looks at buybacks

If the story stopped at “all banks passed,” it would mainly be about system safety. What makes the result relevant to equity investors is the next question: after meeting capital requirements, how much is left to return to shareholders. JPMorganChase answered quickly by raising its quarterly dividend from USD 1.50 to USD 1.65 per share and authorizing a new USD 50 billion buyback program effective July 1, 2026.JPMorgan

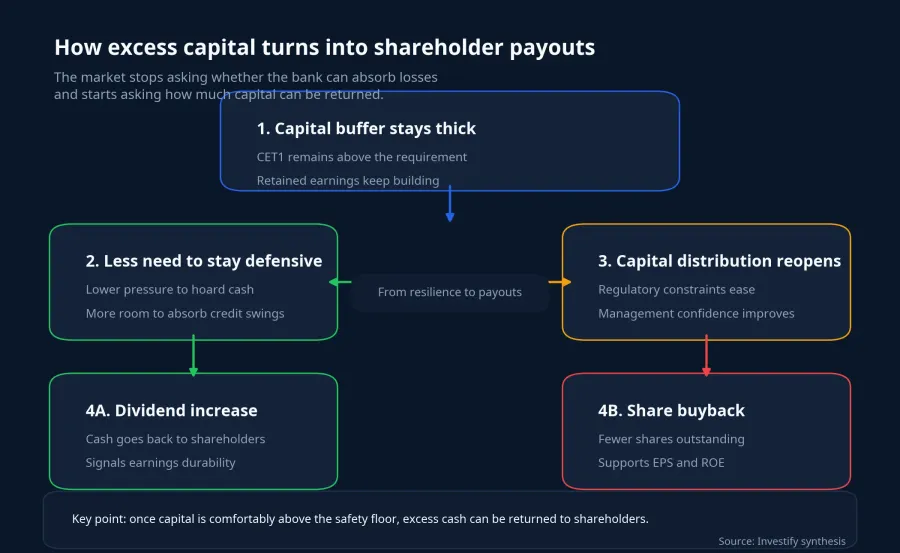

The mechanism is simple. When a bank passes the test but has only a thin surplus above regulatory needs, management usually stays defensive: retain more earnings, move slowly on dividend growth, or limit repurchases. When the surplus is wider, the conversation changes. More room opens up for shareholder distributions, and that transition from capital preservation to capital return is the part the market tends to price.

Buybacks can sound abstract, but their effect is close to the economics investors care about. If the share count comes down while profits stay broadly stable, earnings per share get support. Just as important, a repurchase announcement sends a signal about confidence. Management is effectively telling the market that, after keeping enough capital to satisfy regulators, there is still meaningful cash left to return.

This is also where it helps to avoid inference creep. The source material supports the link between a favorable capital outcome and a larger capital return plan. It does not prove that JPMorgan's stock must rally sharply because of the new authorization alone. Market reaction will still depend on what had already been priced in, where valuations stand, and what peer banks announce next.

The quieter but critical detail: capital requirements were not tightened

Another layer of the story is easy to miss. The Fed said this year's results will not immediately change capital requirements for large banks, with the current framework staying in place until 2027 while a revised model continues through the public feedback process.Fed JPMorganChase also said its stress capital buffer remains at 2.5% through September 30, 2027, and that its standardized CET1 requirement, including regulatory buffers, stays at 11.5%.JPMorgan

That detail matters because bank stocks do not move only on whether institutions pass or fail. Investors also look at whether regulators force banks to hold more capital afterward. If the requirement rises, the room for dividends and buybacks narrows immediately. If the requirement stays stable, shareholder distribution plans become easier to underwrite, and that predictability is often rewarded by the market.

For less experienced investors, this is often the part that gets skipped. “All 32 banks passed” sounds like a complete story, but it is only the first sentence. The next one matters more for equities: after the test, does the bank have to trap more capital on the balance sheet, or can it keep operating with the same regulatory target. That answer tells you how much future earnings may remain locked inside the institution and how much can plausibly flow back to owners.

What investors in Vietnam should take from this

This is not a direct call to buy US bank stocks. A more useful read-through is to treat the news as a signal about global risk appetite ahead of the next trading day in Asia. When the largest US bank feels comfortable announcing a USD 50 billion capital return plan right after the stress-test outcome, the message is that the immediate concern is not a capital shortfall or a sudden regulatory squeeze.JPMorgan

That can support sentiment toward financials and risky assets more broadly, but it should not be stretched into a universal conclusion. The stress test is a model, not a macro forecast. The Fed explicitly says the variables in the scenario should not be interpreted as forecasts by the Fed or the FOMC.Fed A real shock could still come from elsewhere, whether that is liquidity, geopolitics, private credit, technology, or a confidence event that this specific framework does not capture.

The right way to use the headline, then, is as one piece of a larger picture. If other large banks also move quickly with dividend and buyback plans, the “excess capital can be returned” narrative strengthens. If share-price reactions stay muted, that may suggest the market had already priced in much of the result. The same set of facts can therefore tell two different stories, depending on how investors absorb them.

The real signal is not pass or fail

The clearest thesis from this episode is that the 2026 stress test reinforces a market view that large US banks are still in capital-distribution mode rather than sliding back into a defensive crouch. JPMorganChase's dividend increase and USD 50 billion buyback are not a separate story sitting next to the Fed result. They are evidence that, after a severe regulatory test, the bank's capital base still looks strong enough to put shareholders back at the front of the conversation.FedJPMorgan

That is why the next signals to watch are fairly specific. First, how aggressively peer banks update their own payout plans. Second, whether the market rewards the surplus-capital angle or shrugs because it had already anticipated the result. Third, whether the Fed maintains the same transparent and stable approach to capital requirements through 2027. Those markers will do a better job of telling investors whether this was just a good-looking overnight headline or a more durable confirmation of risk appetite in US financials.