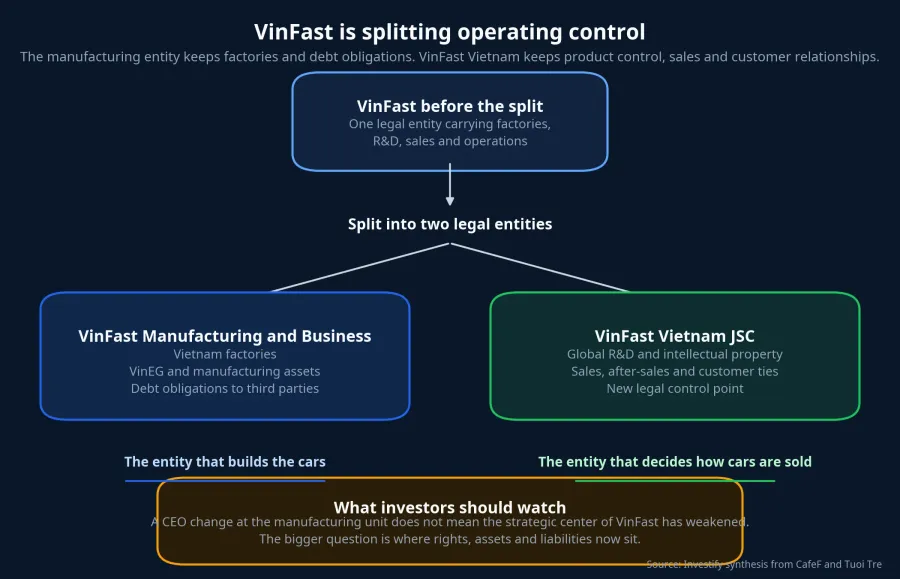

News that Pham Nhat Vuong has left the top executive seat at one VinFast entity can easily look like a management shuffle. But if investors stop at who left and who replaced him, they miss the more important story: after the split, the key question is not who runs the factory entity, but which legal entity now controls product development, sales, customer relationships and financial obligations.

Put simply, this is not a classic "change of generals in mid-battle" story. It is a restructuring move that separates the part of VinFast that builds vehicles from the part that decides how those vehicles are designed, sold and supported. Read that way, Vuong's exit from the CEO seat at VinFast Manufacturing and Business is surface-level news. The real substance is the new map of control after the split.CafeF

The seat changed at the factory, not at the strategic center

On June 22, Pham Nhat Vuong, CEO and legal representative of VinFast Vietnam JSC, was removed from the CEO post at VinFast Manufacturing and Business JSC. His replacement was Trinh Van Ngan, CEO of VinFast Manufacturing and Business JSC, who had previously served as the unit's deputy CEO for manufacturing.CafeFNgười Đưa Tin

The key detail is that Vuong is not stepping away from VinFast in the strategic sense. Local reports say he remains VinFast's global CEO while also retaining his role as CEO and legal representative of VinFast Vietnam JSC.Tuổi Trẻ That makes it misleading to read the headline as a retreat by the group's main decision-maker.

A useful way to think about it is this: in a large corporate structure, the same title can carry very different weight depending on the legal entity attached to it. The CEO seat at the manufacturing unit is tied mainly to factory execution. The executive role at the entity holding R&D, intellectual property, sales and customer relationships is closer to the real strategic steering wheel.

The two legal entities now hold two very different halves of VinFast

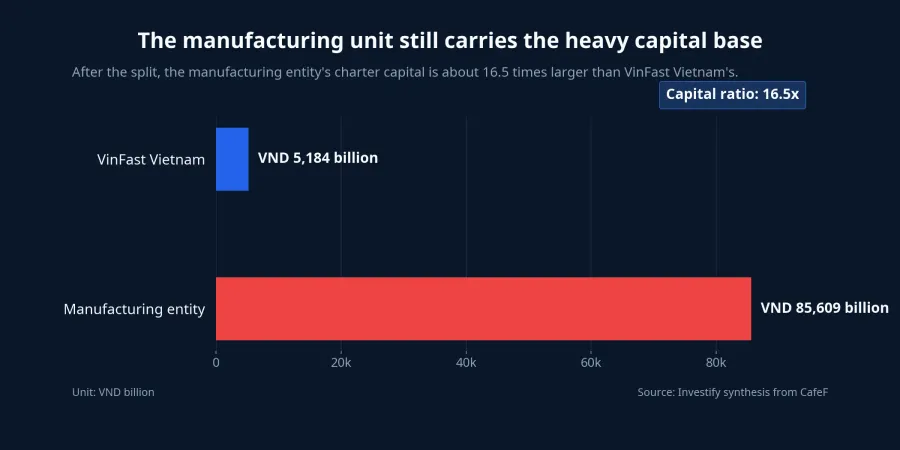

According to the split details cited by CafeF, VinFast Vietnam JSC was formed with charter capital of nearly VND 5,184 billion. After the separation, the manufacturing entity was left with VND 85,609 billion in charter capital.CafeF Those two numbers alone show that this is not cosmetic restructuring. VinFast is dividing a capital-heavy asset block from a commercial control block.

What stayed with VinFast Manufacturing and Business JSC includes the Vietnam factory, the stake in VinEG, production infrastructure and financial obligations to third-party creditors.CafeF In plain terms, this is the heavy side of the business: large capital requirements, depreciation, fixed-cost pressure and day-to-day factory execution.

What moved to VinFast Vietnam JSC is more strategically sensitive: global R&D, intellectual property, after-sales service, vehicle sales and the offshore commercial network, including interests in VinFast Commercial and Services Trading, VinFast Engineering Australia and VinFast Germany.Tuổi Trẻ That is the entity that decides how products are developed, where they are sold, who serves the customer and how the brand is monetized.

For newer investors, the simplest takeaway is that the factory no longer represents the whole VinFast story. The factory builds the vehicles. Another entity now carries the rights that determine the commercial life of those vehicles. That is why the CEO change in manufacturing is better read as a completion of a new structure than as a change in command over the full business.

Capital is still concentrated in manufacturing, but control is not

The charter-capital numbers show that manufacturing remains the heaviest block in the current structure. At VND 85,609 billion, the production entity is about 16.5 times larger than VinFast Vietnam in capital terms.CafeF That reflects the economics of the EV business: factories, tooling and supply chains consume far more capital than pure commercial operations.

But more capital does not automatically mean more strategic control. In an industrial company, especially one still expanding its market footprint, consolidated earnings are shaped not only by factory utilization but also by sales momentum, after-sales costs, new product spending and how efficiently capital turns across markets. That is why the entity holding the heavy assets can remain the largest block while the strategic control point moves elsewhere.

Seen through that lens, Vuong's exit from the manufacturing CEO seat looks more like a cleaner internal division of labor than a withdrawal. The factory entity needs an operator focused on execution. The role Vuong still keeps at VinFast Vietnam is tied to the broader questions: technology, brand, market expansion and the legal architecture of the group.

The transfer deal is the market's real point of focus

The second major development, and arguably the more important one, is the plan to transfer all interests in the manufacturing entity to an investor group led by Future Research and Development Investment JSC. The deal value was disclosed at approximately VND 13,309.6 billion, or about USD 530 million.CafeF

If that transfer is completed, the manufacturing entity would operate as a contract manufacturer for VinFast Vietnam. CafeF reported that the two sides are expected to sign a manufacturing agreement under which the production entity would continue making VinFast vehicles in Vietnam using designs and technical standards supplied by VinFast Vietnam.CafeF That would separate direct ownership of heavy assets from control over the brand and the market interface.

That structure is not automatically positive or negative. What it does show is that VinFast is testing a more flexible model, one in which factory ownership and brand control do not have to sit in the same legal vehicle. The constructive scenario is that VinFast reduces direct exposure to heavy assets while keeping control over product strategy and customer relationships. The less favorable scenario is that valuation, cost allocation and coordination across the two entities make consolidated reporting more complex. The source material does not provide enough evidence to assign a clear probability to either outcome, so the disciplined reading is to track execution rather than pre-label the move as good or bad.

Debt obligations are the real stress test of the restructuring

Whenever a company splits entities, investors usually worry first about whether old obligations are being pushed elsewhere. Here, the reporting is fairly explicit: after the corporate registration, VinFast and the separated company would remain jointly responsible for unpaid debts, labor contracts and other property obligations arising before the split, unless the relevant parties agree otherwise in a way that complies with the law.CafeF

The company also said the split does not change the terms of outstanding bonds, does not trigger early repurchase requirements and does not introduce information that would impair bond repayment capacity.CafeFNgười Đưa Tin That distinction matters. A corporate split is not the same thing as shedding obligations. It is a reallocation of assets, operating rights and responsibilities across legal entities.

For listed-market investors, the practical consequence will not be found in the resignation headline itself. It will show up in the way the new structure flows into consolidated financial statements and operating cash flow. If manufacturing runs smoothly under contract and VinFast Vietnam keeps sales and service execution on track, the new structure could create cleaner role separation. If the transfer drags on, asset valuation becomes contentious or coordination costs rise, the pressure will surface in profit and cash flow rather than in management headlines.

What comes next matters more than the headline

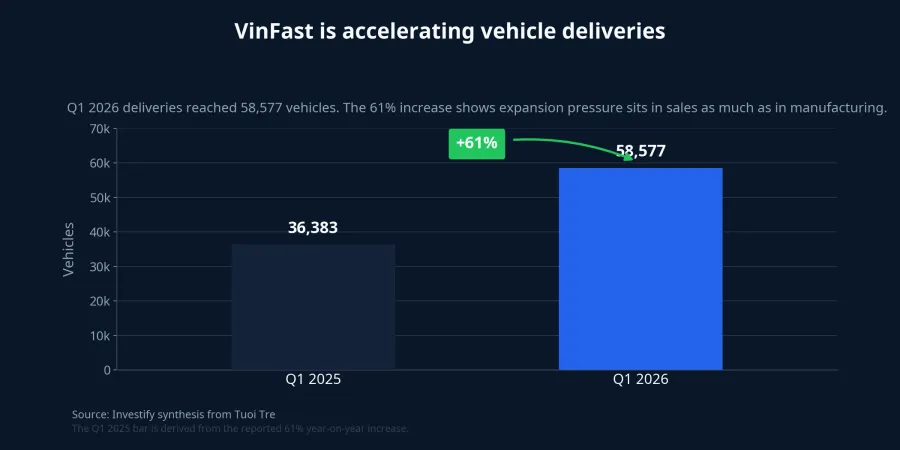

In Q1 2026, VinFast delivered 58,577 vehicles, up 61% year on year, with international markets accounting for about 8% of total deliveries.Tuổi Trẻ That number reinforces an important point: VinFast's challenge is no longer just about keeping factory capacity busy. The company is moving into a phase where delivery growth, after-sales service and international market execution do more to determine group-wide efficiency.

That leads to the clearest conclusion from the current developments: VinFast is not simply changing personnel at the manufacturing arm. It is relocating the strategic center of gravity inside its corporate structure. As long as R&D, intellectual property, sales and customer relationships remain with VinFast Vietnam, Vuong's exit from the manufacturing CEO seat is not enough on its own to justify a bullish or bearish call on the full story. The next signals worth tracking are the transfer timeline, the terms and execution of the manufacturing agreement, and how the new structure affects consolidated reporting and cash flow.