Vietnam's State Treasury had completed only 33.7% of its 2026 government bond issuance plan as of June 15.Báo Chính phủ Read in isolation, that number can sound like a warning that demand for safe assets is fading. In reality, government bond issuance does not work like equities, where capital can reverse course in a single session.

The better question is not simply whether investors are buying. It is whether the state budget needs to borrow aggressively right now, and what yield the Treasury is willing to lock in if it does. Once you frame the problem that way, a slower issuance pace stops looking like a verdict on investor appetite and starts looking like a funding decision.

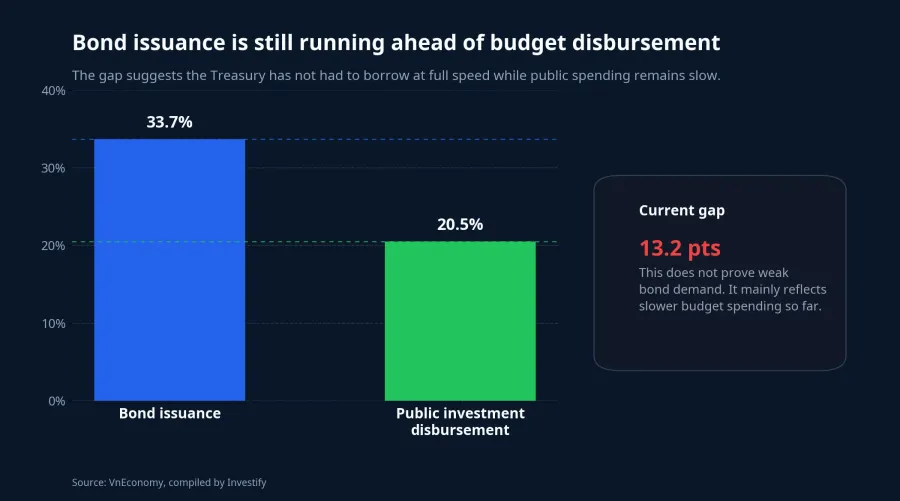

What the 33.7% figure actually tells us

By mid-June, the State Treasury had issued VND 168,501 billion of government bonds against a full-year target of VND 500,000 billion.Báo Chính phủ On the surface, one-third of the plan after nearly half a year looks slow. But annual funding plans are not meant to be executed in a straight line month by month. Borrowing accelerates when spending accelerates.

That is why the disbursement side matters. VnEconomy reported that public investment payments processed through the Treasury had reached only VND 188,832.3 billion by June 15, equal to 20.5% of the annual plan.VnEconomy In other words, budget outflows themselves were still running behind pace.

That context changes the interpretation. Slower bond issuance does not by itself prove that buyers are stepping away from safe assets. A more defensible reading is that the budget has not yet needed to raise cash at full speed because actual spending has not accelerated enough to force that move.

When the budget is spending slowly, the Treasury can wait

For newer investors, the instinct is often to treat any slower pace as a red flag. In this case, that is too simplistic. If public investment disbursement is still subdued, the Treasury has little reason to front-load borrowing while yields are already edging higher. Waiting can be a cost-management choice rather than a sign of market stress.

That is also where government bonds differ from the equity market mindset. Stocks are repriced every day, often on sentiment alone. Government bonds are tied to a slower chain of decisions: how much to borrow, when to borrow, what tenor to issue, and what funding cost is acceptable without creating unnecessary pressure on the debt structure.

Seen through that lens, the current pace is not inherently negative. It mostly says the government has not yet entered a stage where it must sprint to raise capital. If public spending speeds up in the second half, issuance pressure is likely to become much more visible.

Funding cost is rising, and that is the more useful signal

Another important data point is the average issuance yield. As of mid-June, the average yield on government bond issuance had risen to 4.09% a year, up 0.83 percentage points from the 2025 average.Báo Chính phủ At the same time, average tenor reached 9.38 years, while the average remaining maturity of the debt portfolio was held at 8.28 years.Báo Chính phủ

That combination tells a clear story. The Treasury is accepting a higher yield environment while extending the maturity profile of its borrowing. The trade-off is straightforward: longer-dated funding reduces near-term refinancing pressure, but it also locks in a higher cost of capital than in the cheaper-money period investors had grown used to.

That matters far beyond the bond market itself. Government bonds serve as a near risk-free reference point for the local market. When that benchmark yield moves higher, other assets have to reprice around it. Corporate bonds need to offer a wider spread. Fixed-income products need a stronger case for why they deserve investor capital. Even equities face a tougher valuation test when safe yields are no longer exceptionally low.

Safe money does not live in one place

A common mistake is to treat all defensive capital as one pool. In practice, safe money has several homes: bank deposits, government bonds, bond funds, fixed-income products, and cash waiting on the sidelines. Those pools do not shift in perfect sync, and a slower bond issuance pace does not mean money has suddenly abandoned the safe-asset complex.

Thời báo Tài chính Việt Nam reported on June 16 that six-month deposit rates at several banks were still being quoted at 6.85%, 6.8%, and 6.6% a year.TBTCO That is high enough to keep part of defensive capital parked in deposits, especially for savers who value visible rates and clear withdrawal terms. Meanwhile, the VN-Index was at 1,824.53, down 0.32% in Investify system data, which suggests equities are still not an obvious home for every conservative investor.

So the better picture is not one of money "leaving" government bonds for somewhere else. It is a picture of selective waiting. Some capital remains in deposits because the rate is transparent and immediate. Some stays out of equities because the payoff is still uncertain. Some may be waiting for government bond yields or other fixed-income products to become compelling enough relative to the alternatives.

The real test comes in the second half

The first-half picture is coherent. Government bond issuance has reached only one-third of the annual target, but public investment disbursement is running even slower; average issuance yields are higher, while borrowing tenor has been extended to ease shorter-term repayment pressure.Báo Chính phủVnEconomy The most consistent takeaway is that the slow pace of issuance reflects spending timing and funding cost more than any collapse in demand for safe assets.

There is an obvious counterpoint. If public investment disbursement accelerates sharply in the second half, the Treasury may have to issue more aggressively in a market where funding is already less cheap than before. At that point, the story would shift from "no need to borrow quickly yet" to "how much will it cost to borrow quickly now". That is a real risk to monitor, but it does not overturn the current reading.

For individual investors, the practical lesson is not to panic over the 33.7% figure. The more useful lesson is that safe yields are edging higher, and defensive capital is still being allocated selectively across deposits, fixed income, and equities. The signals worth tracking over the next two weeks are new government bond issuance volume, the pace of public investment disbursement, and deposit rate trends. If all three rise together, the market will be moving into a clearer higher-cost-of-capital phase. If not, safe money is likely to remain in wait-and-see mode.