For a first-time investor, it is easy to hear the word "bond" and treat everything under that label as broadly similar: lower-volatility than stocks, periodic interest, principal returned at maturity. That view works only at the surface. Once you look at the structure underneath, Vietnam's government bonds and privately placed corporate bonds are different forms of lending, so they cannot be judged with the same risk lens.

That distinction became clearer in June. As of June 15, 2026, the State Treasury had issued VND 168,501 billion of government bonds, equal to 33.7% of its VND 500,000 billion issuance plan for 2026.Báo Chính phủ At the same time, Decree 200/2026/ND-CP on the offering and trading of privately placed corporate bonds took effect on June 5, 2026, resetting the disclosure and compliance framework for issuers.LuatVietnam

In plain terms, the same word "bond" is now covering two very different financial relationships. In one case, you are lending to the state. In the other, you are lending to a specific company, and your odds of receiving full interest and principal depend on that company's cash flow, assets, and disclosure discipline.

One Label, Two Borrowers

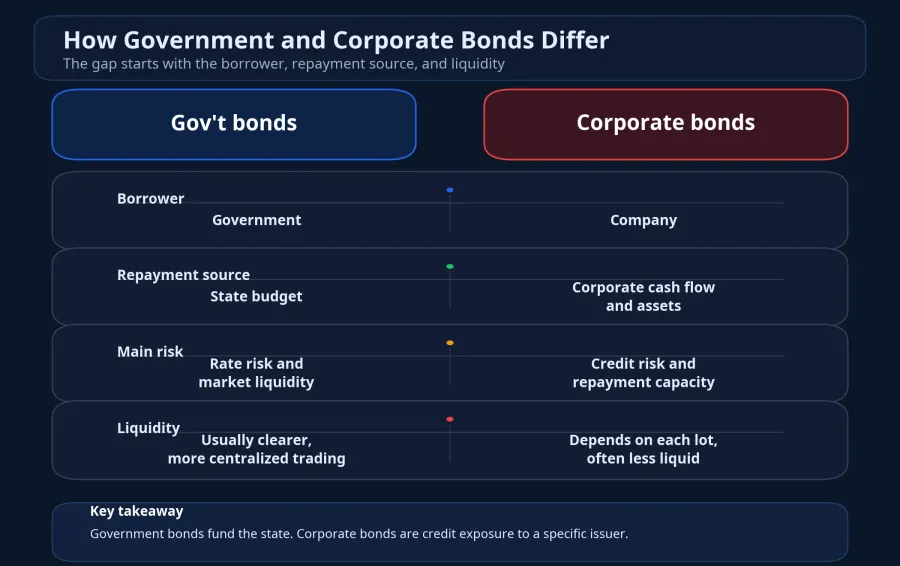

With government bonds, the borrower is the government through the State Treasury. Repayment is linked to the state budget, public debt management, and fiscal capacity. That is why many investors use government bonds as a reference point for lower-risk capital within the broader market, not merely as an instrument that pays periodic interest.

The way the state is borrowing also says something about debt management. As of June 15, all bond issuance this year had been conducted through auctions, with maturities ranging from 3 to 30 years. The average issuance tenor stood at 9.38 years, while the average remaining maturity of the government bond portfolio was 8.28 years.Báo Chính phủ For newer investors, those figures matter because they show the state is not simply borrowing for immediate spending needs. It is also extending the maturity profile of its debt to ease near-term repayment pressure.

Privately placed corporate bonds are the opposite in one important sense: the borrower is never "the market" in general, but a named company with its own balance sheet. A business with stable operating cash flow, credible collateral, and a manageable maturity schedule is one story. A business that needs constant refinancing or depends on asset sales to repay debt is another story entirely.

If you fail to separate the borrower first, you fall into the most common mistake among new investors: seeing two products labeled as bonds and assuming they carry the same baseline safety. That is the point where a higher coupon on corporate bonds starts to look like a bonus, when in reality it is compensation for credit risk that government bonds do not carry in the same way.

What the Money Is Meant to Fund

Government bonds fund budget balancing, deficit financing, principal repayment, and spending needs of the central budget. A State Treasury representative said the current funding raised still meets budget spending needs at a time when public investment disbursement remains slow.Báo Chính phủ Put simply, this is a cash-management and fiscal-timing story for the public sector.

Privately placed corporate bonds are much more issuer-specific. Under Decree 200, an issuer must borrow on its own responsibility, repay on its own responsibility, and bear full responsibility for how the funds are used and how the debt is serviced. The permitted purposes include investment projects, debt restructuring, and other lawful uses under sector-specific rules.Báo Chính phủ That language alone should remind new investors that a corporate bond is not backed by the same cushion as a government bond.

This difference changes how you should read the coupon. A lower-yielding government bond is not automatically less attractive in every case. It simply reflects lower risk. A higher-yielding corporate bond becomes worth considering only after the investor understands what the issuer is funding and what stream of cash is supposed to come back to service the debt.

Investor Protection Does Not Sit in the Same Place

When you own a government bond, you are in a market with clearer auction issuance and a more centralized trading framework. The main risks for a retail investor usually revolve around interest-rate moves, holding period, and personal liquidity needs. If you buy a long-duration bond and need cash early, you may face price risk when selling. But that is still a very different type of risk from an issuer weakening operationally.

With privately placed corporate bonds, investor protection does not come from the common label. It comes from the issuance file and the issuer's actual discipline. Decree 200 requires the issuer to take responsibility for the accuracy, honesty, and completeness of the offering documents, and to track and use the proceeds in line with the disclosed purpose.Báo Chính phủ In other words, tighter rules give investors a better basis for reading the file, but they do not turn corporate risk into sovereign risk.

This is where many new investors get confused. A new regulation does not make all corporate bonds equally safe. A stronger rulebook simply helps you see more clearly who is borrowing from you and what you are accepting in return. If the issuer weakens, the collateral proves hard to realize, or the project cash flow arrives late, the risk still lands where it always has: with the bondholder.

Where a New Investor Should Start

If this needs to be reduced to a practical checklist, the starting point is not the coupon but four questions. Who is borrowing your money. What will that money be used for. What source will repay interest and principal. If you need to exit early, how do you get out.

Those questions sound basic, but they block most beginner mistakes. When reading a government bond, you are mostly answering questions about tenor, your own liquidity needs, and the benchmark rate environment. When reading a privately placed corporate bond, you need to go one layer deeper: which company stands behind it, what its debt structure looks like, and whether current cash flow is enough to repay debt without leaning on a project that has not yet delivered.

One point is worth stating plainly to avoid over-reading the coupon. A high coupon does not prove a corporate bond is bad, and it does not prove it is attractive. It only tells you the issuer is paying more to raise money. The reason could be a solid project in a riskier industry, or it could be weaker credit quality that prevents the company from borrowing more cheaply. Without more evidence on cash flow and offering terms, investors should not turn the coupon into a conclusion.

This framework also helps avoid another mistake: applying the regularity of government bond issuance to corporate bonds. The fact that the State Treasury has already completed roughly one-third of its annual issuance plan by mid-June shows that state funding through bonds is moving along a visible track.Báo Chính phủ But that says nothing by itself about the quality of any individual corporate issuer, because the two sides do not borrow from the same balance sheet and do not repay from the same pool of money.

The Core Takeaway

The bond market is not one uniform block. Government bonds belong to the state funding story, where the key variables are the budget, debt maturity, and benchmark rates. Privately placed corporate bonds belong to the credit story of each issuer, where every deal needs to be read as a separate loan.

That leads to one clear conclusion. A new investor should not begin with "How much interest does this bond pay?" but with "Who am I lending to, and what source will repay me?" Once those two questions are answered, it becomes much easier to understand why government bonds and corporate bonds share the same label but should not be measured with the same yardstick. The signals worth watching next are government bond issuance progress in the second half of the year and how issuers comply with disclosure obligations under Decree 200.