Vietnam's upgrade story has just gone through an important stress test. In its Global Market Accessibility Review released on June 18, 2026, MSCI kept Vietnam in the frontier-market bucket and did not change the way it scores the market's accessibility, despite the reform momentum investors had been watching.MSCI

That does not mean the reforms were dismissed. It means MSCI is applying a tougher standard: markets do not get a better score simply because new fixes have been announced. They move up only when those fixes produce a better real-world experience for global institutions trading, settling, receiving disclosures, and moving capital in and out.

That is where Vietnam now stands. Policy has opened the path, but operating proof still needs to accumulate. For anyone trying to read the MSCI story correctly, that is the core point.

MSCI does not score intentions. It scores lived market access

MSCI classifies markets using three broad sets of criteria: economic development, size and liquidity, and market accessibility.MSCI In Vietnam's case, the main bottleneck has not been sheer market size. The practical question is whether a foreign fund can enter the market, buy enough stock to match an index, receive information on time, and exit with acceptable friction.

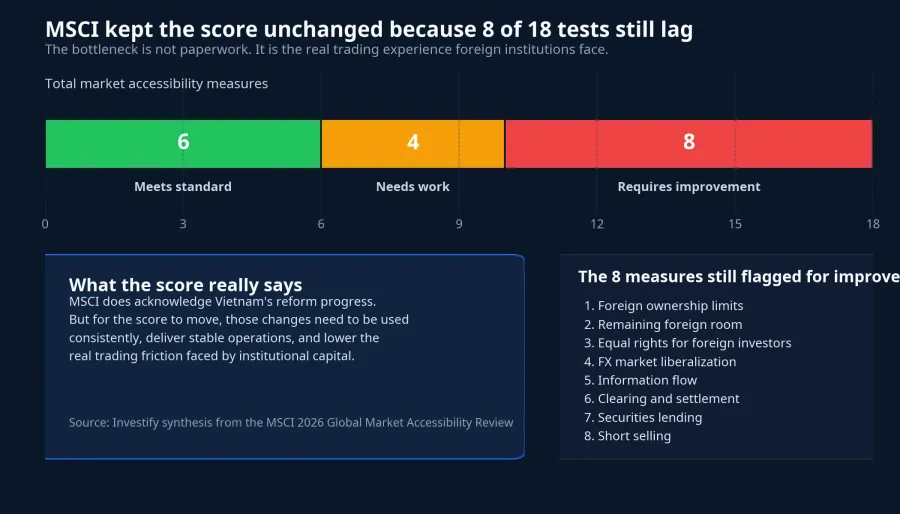

This year's review covered 79 markets and used 18 measures across 5 broad categories to judge accessibility.MSCI That is why a single positive rule change rarely shifts the score on its own. MSCI looks at the full operating chain, from foreign ownership room and FX access to disclosure quality and post-trade settlement.

Vietnam still has 8 of those 18 measures marked as "requires improvement" in MSCI's appendix. The weak spots are specific: foreign ownership limits, remaining foreign room, equal rights for foreign investors, FX-market liberalization, information flow, clearing and settlement, securities lending, and short selling.MSCI

From a policy perspective, that list matters because it shows what the market still needs to do, not just what it says it plans to fix. If an index-tracking fund still cannot buy a stock because foreign room is too tight, or still cannot get complete English-language disclosure at the same time as domestic investors, then the market experience still falls short of emerging-market standards.

What progress MSCI is already acknowledging

The constructive part of the review is that MSCI is not ignoring Vietnam's progress. The report notes ongoing capital-market reforms, including an omnibus-style brokerage model that lets foreign investors access the market without opening a domestic account, the formal establishment of a central counterparty with an early-2027 target date for operations, and the roadmap for broader English-language disclosure.MSCI

Those are the right building blocks. For a market trying to move up a classification ladder, post-trade infrastructure is always central because it shapes how secure large pools of capital feel. Once the central counterparty, or CCP, is operating reliably, counterparty risk can be managed through a clearer and more standardized framework. That is the kind of change MSCI can observe through live operating evidence rather than promises.

The Investor also summarized Vietnam's temporary removal of the full pre-funding requirement before buy orders. But the same report makes clear that an internationally stronger settlement framework only really arrives once the CCP structure is fully in place, which is currently targeted for early 2027.The Investor

Disclosure is another area where the direction is clear, but the finish line is still ahead. Citing MSCI, The Investor reported that the Ministry of Finance began a roadmap requiring public companies to disclose information in both Vietnamese and English from January 2025 through January 2028.The Investor For foreign institutions, that matters over the long term because they need translations that are timely, consistent, and detailed enough to support portfolio decisions.

Why the score is still stuck

The issue is that most of those changes are still mid-journey. The English-disclosure roadmap has begun, but it does not yet cover the market evenly. The temporary pre-funding fix removes one bottleneck, but the broader settlement framework is still waiting for the most important piece, the CCP, to go live. Put simply, reform progress exists, but the operating data are not deep enough yet.

Foreign exchange is an even harder constraint. According to The Investor's summary of the MSCI review, Vietnam still lacks an offshore Vietnamese dong market, while onshore FX transactions remain tightly tied to securities-related purposes.The Investor For long-term international capital, FX flexibility matters almost as much as foreign room because it determines how smoothly a fund can enter and leave the market.

Foreign ownership limits are also more than an isolated technical issue. The Investor reported, again citing MSCI, that some conditional or sensitive sectors still cap foreign ownership at 0% to 7%, and that these restrictions affect more than 10% of Vietnam's equity market. In addition, more than 1% of the MSCI Vietnam IMI Index remains affected by limited remaining foreign room.The Investor

That "more than 10%" figure carries an important message. For MSCI, this is not about a handful of isolated cases. When the restriction is large enough to change how a fund replicates an index or allocates capital under a global process, it becomes a structural problem. That is why the argument that "the market has already reformed, so why has the score not improved?" misses the real issue.

Another reading to avoid is treating MSCI's unchanged score as evidence that the reforms failed. The available evidence supports a more measured conclusion: the reform direction is constructive, but it has not yet crossed the threshold where institutions can say the trading experience itself has materially changed. The real question is no longer how many measures were announced, but how far they have been implemented and how often the market is actually using them.

The next step will be decided by operating proof

From a policy angle, three milestones now matter most. First, the bilingual disclosure roadmap needs to keep moving through January 2028 and become consistent across listed companies, not just across a small group of large names.The Investor Second, the CCP needs to go live on its early-2027 schedule rather than slip again.MSCI Third, Vietnam needs tangible progress on the FX side and on tools that support foreign capital flows.

Those milestones matter because they produce the kind of proof MSCI actually needs. A market does not win an upgrade by saying mechanisms are being prepared. It needs to show that the daily operating frictions have been reduced, from the moment an order enters the system to the moment cash and securities are safely settled.

For retail investors, that distinction also has practical value. The upgrade story is often framed like a one-day catalyst, but in reality it is closer to a long validation process. When reading expectations around foreign inflows, new investors should focus on the quality of implementation in market infrastructure and regulation rather than headlines about reforms alone.

Conclusion: The reform case is alive, but not yet score-changing

The most important takeaway from this review cycle is that MSCI is not rejecting Vietnam's reform effort. It is asking for more evidence that those reforms have become a better real trading experience for international institutions. An unchanged score should therefore be read as a test of execution, not a vote against the reform path.

If there is one direction to commit to today, it is a constructive story that still lacks acceleration. The reforms are moving the right way and are already being recognized in MSCI's language. But the upgrade case only strengthens materially if the CCP launches on time, English disclosure becomes broader and more consistent, and the FX and foreign-room bottlenecks show real improvement. Unless those milestones slip again, that thesis still holds.