A bond sale can still unwind after the money has been raised if the proceeds go somewhere they were never supposed to go. That is the real lesson in the DIC Corp case, where regulators fined the company and ordered corrective action on a VND 600 billion bond lot. For first-time investors, this is not a niche legal story. It is a concrete example of why private placement bond risk does not end once the issuance closes.MarketTimes

The headline number, on its own, is easy to dismiss: a VND 175 million administrative fine. The more important part is the remedy. DIC Corp was required to recover the securities it had offered and refund investors the bond purchase amount, plus accrued interest based on the bond’s stated rate. That changes the story from a compliance footnote into a direct investor-protection issue.TBTC VN

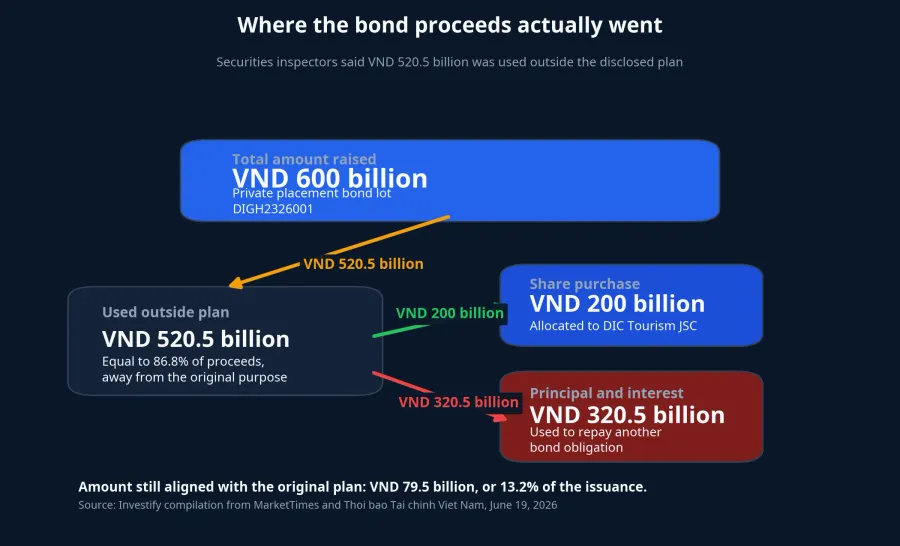

What happened to the bond proceeds

According to reports published on June 19, DIC Corp was penalized for using money from a private securities offering in a way that did not match the plan approved by its board and disclosed to investors. The bond lot in question totaled VND 600 billion, yet VND 520.5 billion was used outside that original plan. Of that amount, VND 200 billion went into a share purchase in DIC Tourism JSC, while VND 320.5 billion was used to pay principal and interest on another bond lot.MarketTimes

The key point is not whether those uses sounded commercially reasonable in isolation. The key point is that they did not match the path investors were originally told to expect. Thoi bao Tai chinh Viet Nam reported that the initial plan was to direct the money to the Long Tan urban tourism project in Dong Nai. Once the actual cash path drifts away from the disclosed plan, investors are no longer dealing only with credit risk. They are also dealing with commitment risk.TBTC VN

Why the coupon rate is not enough

New investors naturally gravitate toward the easiest number to remember: the yield. That is understandable. Coupon rates are visible and marketable, while issuance files, use-of-proceeds reports, and post-issuance amendments are harder to read and rarely show up in sales pitches. But the DIC Corp case makes one point clear: the risk in a private bond continues to evolve after the issuer has already taken the money.

The simpler way to frame it is this: a private bond should be read like a contract about the use of capital. One side of the contract is the promise to pay interest and principal. The other side is the promise to use the proceeds for the disclosed purpose, keep investors informed, and stay accountable if the money is redirected. If you read only the first side, you are evaluating the instrument with half the picture missing.

That matters even more in Vietnam’s private corporate bond market, where Decree 65/2022 lays out rules on issuance files, stated issuance purposes, disclosure obligations, and the definition of a professional investor. Those rules do not make every deal safe. What they do provide is a framework investors can use to inspect the deal before relying on its promised return.Thư viện PL

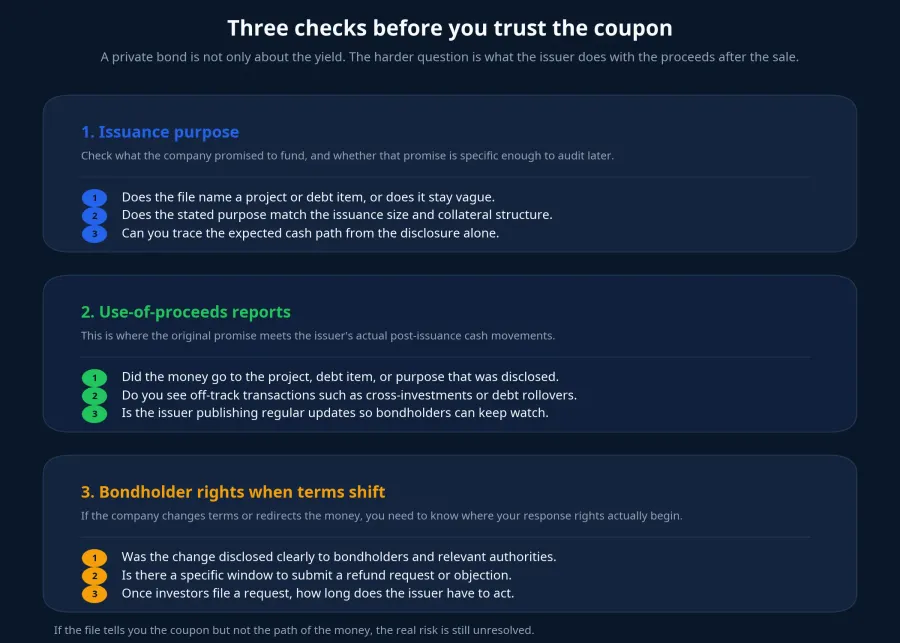

Three checks before committing money

The first check is the issuance purpose itself. Is the file specific enough to tell you which project, debt item, or funding need is being financed, or does it stay vague with language such as working capital or business operations. The more specific the purpose, the easier it is for investors to compare the original promise with what happens later.

The second check is the use-of-proceeds report. This is the most revealing part of the file because it tells you where the money actually went. If the original plan points to a project but later reporting shows cross-investments, repayment of other obligations, or transactions that do not connect back to the initial plan, caution should rise immediately. The DIC Corp case is not abstract on this point. The problem was not weak storytelling. The problem was a break between the disclosed plan and the observed use of cash.MarketTimes

The third check is what bondholders can actually do if terms change or the money is redirected. Under Decree 65/2022, any change to the terms and conditions of a domestically issued bond must be approved by the competent corporate authority and accepted by bondholders representing at least 65% of the outstanding amount of that bond type. That is not a technical detail for lawyers to worry about later. It tells investors that when the issuer wants to rewrite the deal, there is a formal process and bondholders should pay attention to it.Thư viện PL

Not everyone is meant to buy this product

For non-convertible private corporate bonds without warrants, the target buyers are professional securities investors. For individuals, one common condition is an average market value of at least VND 2 billion in listed or registered securities holdings over at least the previous 180 days, with the investor certification remaining valid for three months. That point matters because it reminds first-time investors that this is not a mass-market savings substitute.Thư viện PL

If a product is being pitched as if anyone can easily buy it, that is already a reason to slow down. It does not prove the deal is bad. It does suggest that part of the legal risk filter is being blurred in the marketing process. For new investors, understanding whether they even belong in the target buyer group is part of risk management, not an annoying formality.

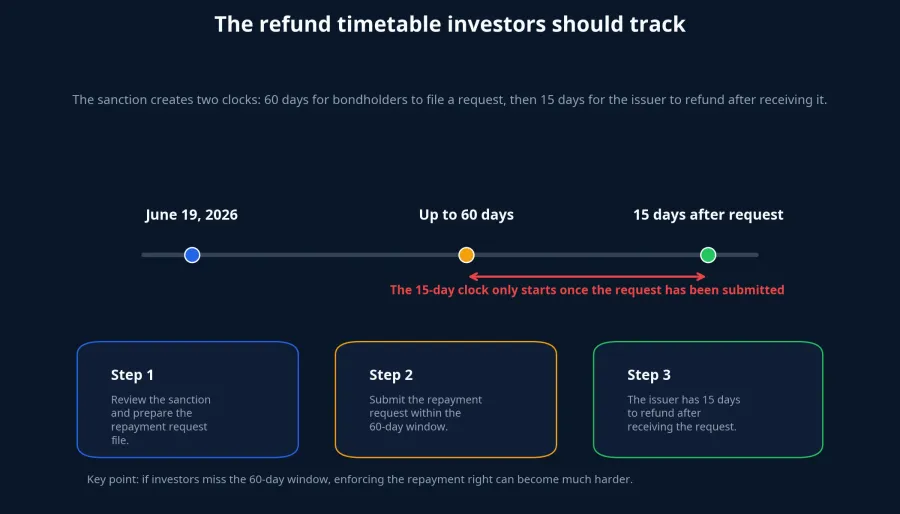

The 60-day window matters more than it sounds

The corrective action in the DIC Corp case creates two time clocks investors should remember. First, investors have up to 60 days from the effective date of the sanction decision to submit a refund request. Second, once the issuer receives that request, it has 15 days to refund the bond purchase amount or deposit, if any, together with accrued interest. Those clocks do not start at the same time. The 15-day countdown begins only after the investor’s request has been filed.MarketTimes

That is the kind of detail first-time investors often miss. Many assume a sanction order automatically triggers repayment for every bondholder. In practice, investor rights are often tied to timely action: monitoring the case, preparing the required documents, submitting the request, and keeping a record of the process. Miss that window and a right that looks strong on paper can become far harder to enforce in real life.

Conclusion: bond safety starts with the cash path

The DIC Corp case does not prove that every real-estate bond is dangerous, and it does not prove that every high coupon is a trap. The stronger conclusion is narrower and more useful: in the private bond market, yield is only the promised reward. The real test of safety begins with whether investors can verify where the money goes after issuance.

For a new investor, the simplest rule is to move past the question of “how much does it pay.” The next questions matter more: what was the money supposed to fund, did it actually go there, and what rights do bondholders have if the issuer changes course. Those questions do not make a bond automatically safe. They do make the actual risk visible before the market is forced to discover it the hard way.