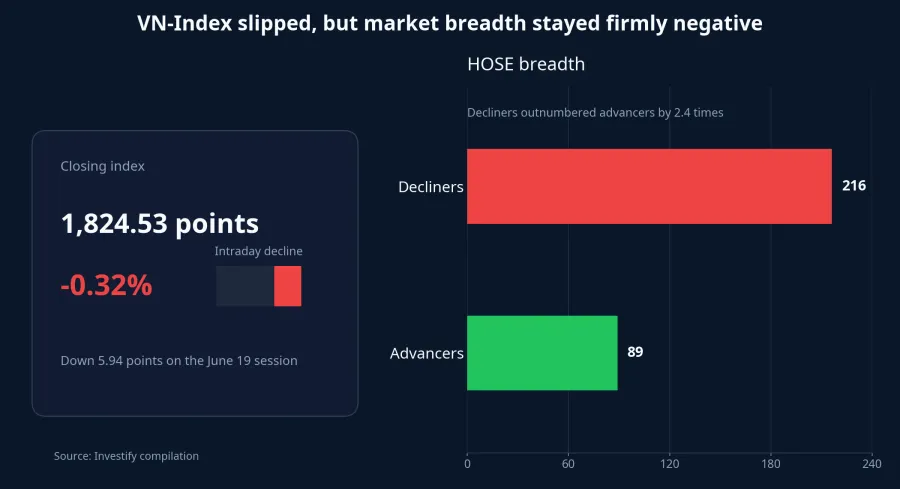

June 19 was the kind of session that can mislead newer investors. The VN-Index closed at 1,824.53 points, down 5.94 points or 0.32%, while HOSE recorded 216 decliners against just 89 advancers. In that kind of tape, a handful of large-cap property names holding their ground is enough to create the impression that money is rotating back into real estate.

But holding the tape together is not the same thing as launching a sector rally. What the market showed on this session was continued interest in property stocks, but in a highly selective way: money stayed close to index anchors, watched restructuring stories that still had room to develop, and tested names whose profit story sits more in future handovers than in current earnings. All three are meaningful. None of them, yet, is broad enough to stand in for the whole sector.

Holding the tape together is not the same as a broad move

The basic distinction is simple. A sector is truly in rally mode when strength stops being concentrated in a few familiar tickers and begins to spread across the rest of the basket. June 19 did not show that. The clearest signal was still the stabilizing role of a few large names, not a broad-based wave of buying across real estate.

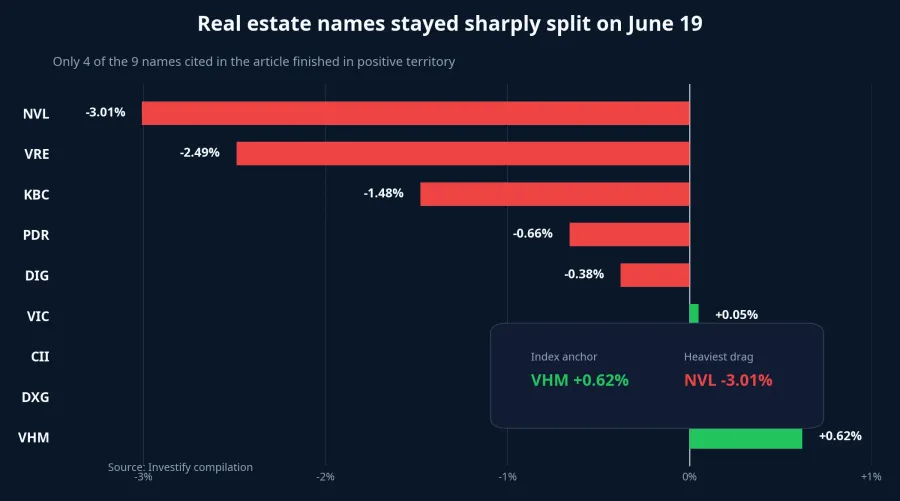

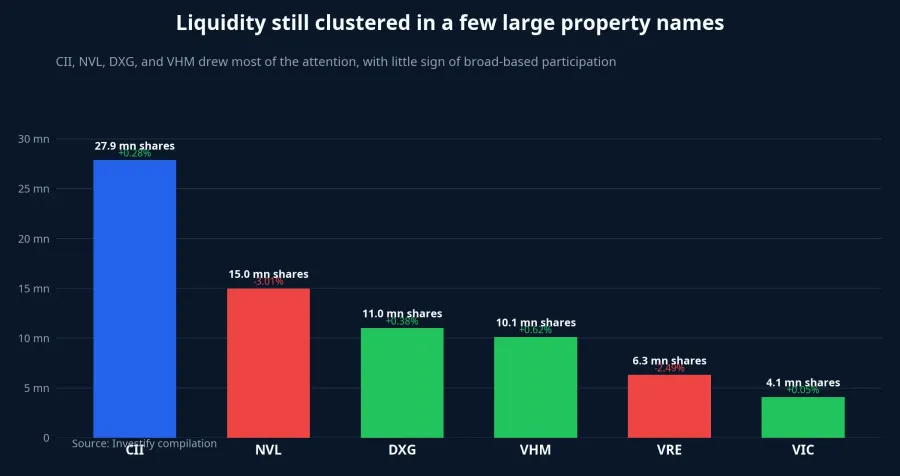

VHM was the clearest example. The stock closed at VND 145,300, up 0.62% on more than 10.1 million shares traded. A gain of less than 1% is not a breakout by itself, but VHM’s market value is large enough that even a modest rise can make the whole property group look better supported than it really is. VIC played a similar role, ending at VND 205,500, up just 0.05% after its much stronger June 18 session. That is price support, not sector leadership.

The rest of the screen told a different story. VRE fell 2.49%, NVL dropped 3.01%, KBC lost 1.48%, and both PDR and DIG finished below the reference price. If you focus only on the large caps or only on the sector index, it becomes easy to miss the fact that selling pressure was still present across several other property names.

By the numbers, this was a split tape rather than a unified one. Of the nine property names most discussed in the session, only four advanced, and even those gains were thin. When decliners still outnumber advancers inside the group, the more defensible read is that money is clustering around a few support points, not repricing the whole sector higher.

Money is chasing three different stories

This matters because investors who do not separate those stories can end up trading a mood instead of a setup. These are all property stocks, but the market is responding to them through three different lenses. One is index support. One is restructuring. One is deferred earnings power tied to future handovers.

For the index-support bucket, VHM and VIC were the obvious reference points on June 19. These names do not need huge percentage gains to change sentiment around the sector because investors often treat them as emotional proxies for property risk. When the anchors stay green, many market participants assume pressure is easing, even if the broader group has not confirmed that view.

For restructuring, NVL remains the name to watch, not the name to simplify. In an interview with Tuổi Trẻ, Dương Văn Bắc, Chief Executive Officer of Novaland Group (NVL), said the company had entered the third year of its restructuring process, was treating 2026 as the final year of that effort, and had already resolved around 70% of its retail bond debt, with the remainder still being handled.Tuổi Trẻ

He also said Novaland plans to launch more than 2,000 units in 2026, including around 1,000 in Ho Chi Minh City.Tuổi Trẻ That helps explain why NVL remains under close watch even though the stock itself fell 3.01% on June 19. In other words, the market has not abandoned Novaland’s recovery narrative, but it is not willing to price in a straight-line recovery either.

This is where newer investors need to stay disciplined about causality. Heavy turnover in NVL can reflect restructuring hopes, but it can also reflect short-term trading, position rotation, or attempts to test how the stock reacts after new headlines. The evidence in the source material is not enough to assign all of NVL’s move to the restructuring story alone, so the safer conclusion is that interest remains high while conviction is still being tested.

For the future-handover bucket, DXG is the cleaner example. In an updated report, Vietcap forecast 2026 net profit after minority interest at VND 239 billion, up 4%, before rising to VND 1.9 trillion in 2027, mainly on planned handovers at The Privé and a larger contribution from Gem Sky World.Vietcap

The key point here is that the market does not only price the present. It also tests whether it wants to pay ahead for a future delivery cycle. That is why DXG’s 0.38% gain on June 19 is not very informative on its own. Set against the 2027 earnings expectation, it becomes part of a larger question: how early is the market willing to pay for profits that still sit further down the road.

DIG, by contrast, brings balance-sheet risk back into the picture. According to VnEconomy, as of June 12, 2026, DIC Corp had disbursed only VND 715.38 billion from its follow-on share issuance, leaving VND 1,084.18 billion still unused. The same report said first-quarter 2026 net revenue fell 5.41% to just over VND 144.5 billion, while the company still posted a net loss of nearly VND 10 billion.VnEconomy

Undeployed cash is not automatically bullish. The real question is how quickly that cash can be put to work and whether it genuinely relieves financial pressure or merely extends the waiting period. That makes DIG’s 0.38% decline on June 19 a logical reaction: the market still wants harder evidence that capital can turn into projects and that projects can turn into real cash flow.

The more reliable signal is breadth

If there is one lesson to take from June 19, it is this: do not let a few green property stocks stand in for the whole sector. The broader picture says money has not abandoned real estate, but it is still behaving in a highly selective way. That is very different from saying the group has entered a true upward phase.

For newer investors, the next-session checklist should not begin and end with whether VHM or VIC stays green. The more reliable test is breadth: whether gains spread into names such as KDH, NLG, KBC, PDR, or DIG; whether turnover remains trapped in a few familiar leaders or begins to appear across multiple names at once; and whether story-driven stocks like NVL and DXG can hold buying support after the first wave of headlines has already been partly reflected in price.

The cleanest thesis for now is that real estate has localized support, not yet a convincing sector-wide move. The bigger risk for newer investors is not missing a rally. It is mistaking a narrow concentration trade for a full-sector reversal. What would change that picture is straightforward: breadth has to improve for real, rather than relying on a few heavyweight anchors and a few isolated narratives.