A trade deficit of nearly USD 14 billion is large enough to trigger an immediate reaction from newer investors. The instinct is simple: if Vietnam is buying more goods from abroad than it sells, demand for dollars should rise and USD/VND should eventually jump. That logic works at the first layer, but it misses a more important one: foreign-currency inflows and the way expectations are being managed in the market.

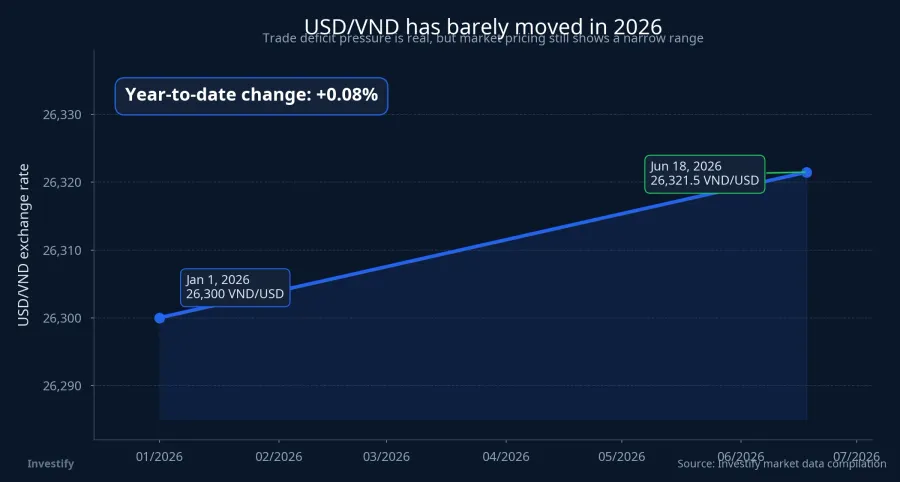

Put differently, a trade deficit is pressure, not a verdict. In the first five months of 2026, Vietnam posted a trade deficit of USD 13.81 billion, yet market data from the start of the year to June 18 showed USD/VND moving only from 26,300 to 26,321.5, or roughly 0.08%. On June 19, the State Bank of Vietnam set the central rate at VND 25,181 per dollar.CafeFSBV If the trade deficit headline were the full story, that price action would be hard to explain.

The key distinction is that the goods balance is not the same thing as the full foreign-exchange balance. Dollars leaving the country to pay for imports are only one leg of the picture. At the same time, there are FDI disbursements, export proceeds returning home, remittances, portfolio flows, and commercial banks' own FX positioning. As long as those channels still absorb part of the pressure, the exchange rate can drift rather than break higher.

This deficit is being driven largely by production inputs

For investors, not all trade deficits mean the same thing. A deficit caused by households rushing to buy imported consumer goods carries a different signal from one driven by companies importing raw materials and machinery to fulfill future orders. The first case usually looks more threatening for the currency because dollars go out without a clear timetable for coming back. The second still creates near-term demand for dollars, but it also leaves open the possibility that those dollars return later through exports.

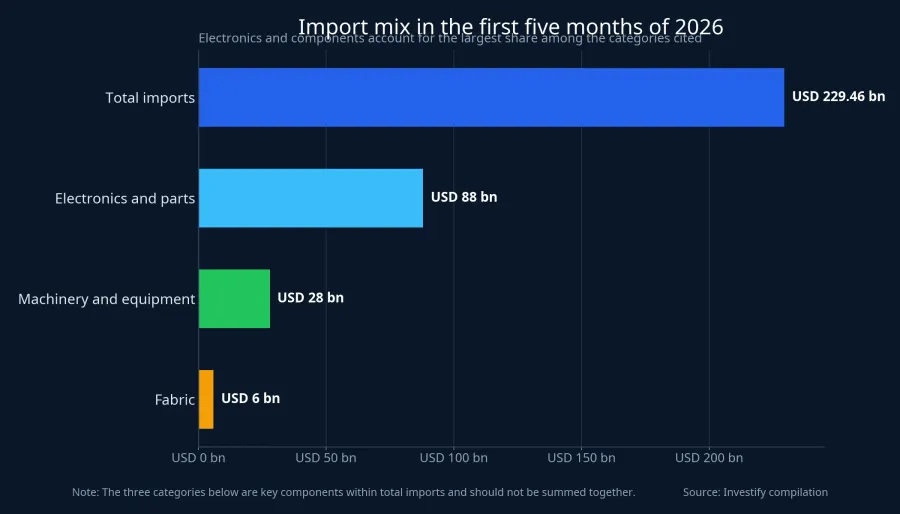

The first five months of 2026 look much closer to the second case. Total trade turnover reached USD 445.12 billion, up 25.0% year on year. Exports rose 19.5%, while imports climbed 30.8%. Total imports came in at USD 229.46 billion, with computers, electronics and components alone accounting for more than USD 88 billion. Machinery, equipment, tools and spare parts reached nearly USD 28 billion, while fabric imports exceeded USD 6 billion.CafeF

That mix matters more than the headline number. The strongest growth is concentrated in inputs used to make things, not simply in final imported consumption. In other words, dollars are leaving Vietnam to buy components, machines and materials rather than just to finance a burst of imported shopping.

That does not make the trade deficit good news. It changes how it should be read. If those imported inputs are turned into export orders over the next few months, part of the FX pressure will naturally be offset. If companies keep importing inputs but export momentum fails to catch up, the same deficit can shift from a sign of expanding production into a genuine exchange-rate problem.

So the right question is not whether a trade deficit is scary in the abstract. The better question is whether the current surge in imports is creating future export capacity and future dollar inflows. For less experienced investors, that distinction is critical because the same trade-deficit figure can point to very different investment implications.

Realized FDI is offsetting part of the dollar demand

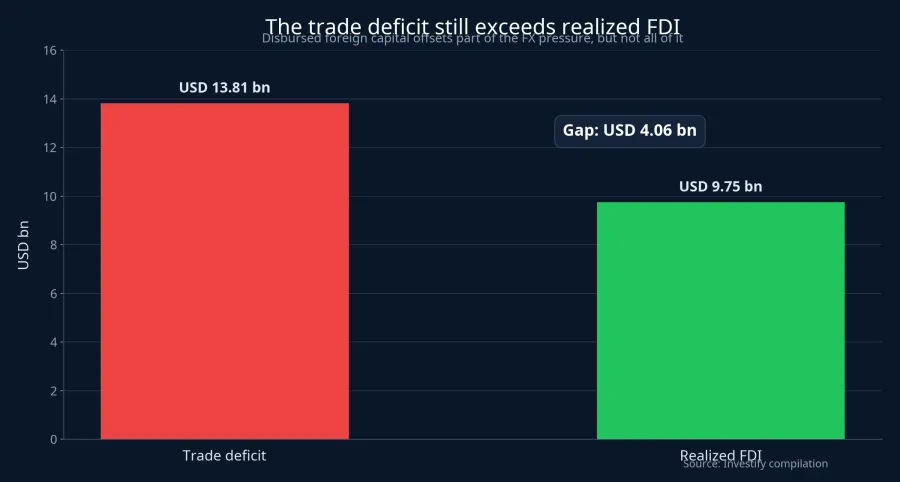

One reason USD/VND has not reacted aggressively is the supply side of the FX market. Realized FDI continues to come in at a healthy pace. According to National Statistics Office data cited by CafeF on June 14, total registered FDI in the first five months of the year was nearly USD 25 billion, up almost 35% from a year earlier. More importantly for the currency market, realized FDI reached USD 9.75 billion, up 9.6% and the highest level for the same period in five years. Manufacturing and processing accounted for more than USD 8 billion, or 82.7% of total disbursed FDI.CafeF

That USD 9.75 billion obviously does not erase a USD 13.81 billion trade deficit. But it does show why the FX market cannot be reduced to a one-line story in which dollars go out and the exchange rate must immediately spike. The FDI sector is currently one of the largest importers of machinery and components, but it is also a major source of hard-currency inflows through project disbursements and, later, export revenue. Ignore that loop and the pressure on the currency becomes easy to misread.

It is also worth being disciplined about causality. The evidence does not support the claim that FDI alone is keeping the exchange rate stable. The broader picture still includes rate differentials, the global dollar trend, energy prices, and the way commercial banks manage their FX books. But with the evidence now available, realized FDI is clearly one of the most important offsetting flows, and it helps explain why a large trade deficit has not yet turned into a sharp USD/VND move.

Set the two figures side by side and the picture becomes more grounded: the trade deficit still exceeds realized FDI by about USD 4.06 billion. That means the pressure has not disappeared, but it also has not become a one-way imbalance. For investors reading the market before the open, this is a signal to stay alert, not a signal to panic.

The market is still being anchored by expectations

Beyond actual flows, the FX market is driven heavily by expectations. That is the part many newer investors underestimate. Exchange rates do not just reflect how many dollars are available today. They also reflect what the market believes about the direction of dollar supply and demand over the next several weeks.

According to analysis relayed by Thoi bao Tai chinh Viet Nam from UOB, the VND has been more stable in recent weeks, trading within a 26,291 to 26,372 range in April and May. UOB also said that intervention through cancellable 180-day forward contracts at VND 26,850 per dollar helped anchor market expectations.TBTCO

The phrase "helped anchor" matters here. There is not enough evidence to say a single policy tool fully determined the path of the exchange rate. But the current evidence does support a more limited conclusion: the market is not trading in panic. If Vietnam were facing a true FX shock, price moves would likely be larger, trading bands would widen more quickly, and expectations would deteriorate far more visibly.

That is also why the current forecasts still look orderly. UOB projects USD/VND at 26,500 in Q3 2026, 26,400 in Q4 2026, 26,300 in Q1 2027 and 26,100 in Q2 2027.TBTCO That is a controlled depreciation path in the near term, not a call for an exchange-rate dislocation.

What investors should monitor before the next session

For equity investors, the exchange rate is not an abstract macro topic. It feeds directly into company-level valuation. A weaker VND raises sensitivity for businesses with dollar debt, imported inputs or sizeable foreign-currency costs. Exporters with dollar revenue may benefit, but the actual earnings effect still depends on hedging contracts, input costs and how much pricing power they have in their end markets.

The better framework is not to read the currency through a single trade-deficit headline. A more useful checklist has four layers. First, is the deficit coming from consumer imports or from production inputs. Second, is realized FDI still strong enough to offset part of the demand for dollars. Third, are exports absorbing the imported inputs now entering the system. Fourth, are policy signals and market expectations staying as stable as they have been in recent weeks.

That leads to a fairly clear thesis. A trade deficit of nearly USD 14 billion is a yellow light for the exchange rate, but it is still not enough to conclude that USD/VND is about to break higher. The bigger risk would emerge only if several offsetting layers weakened at the same time, for example if FDI disbursement slowed, exports failed to catch up with imported inputs, and market expectations began to drift away from the range now being anchored. Those are the signals worth watching over the next few weeks, rather than using one trade-deficit figure to explain the entire currency story.