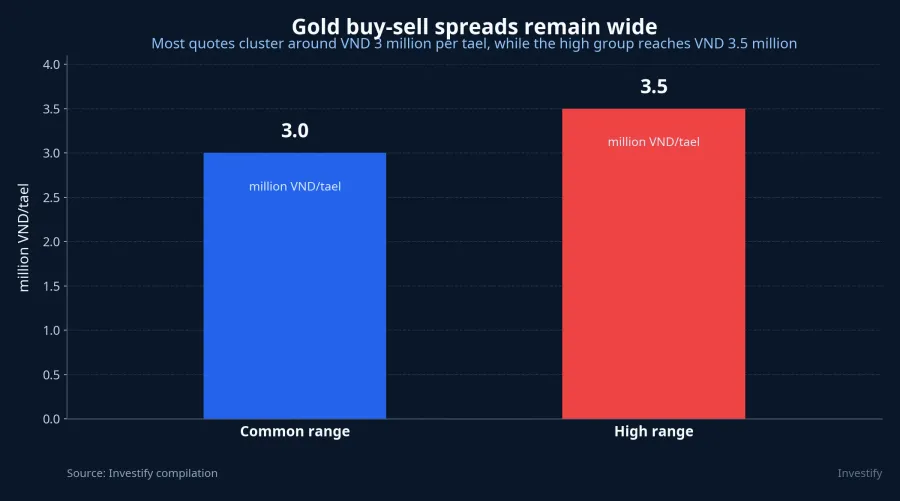

A falling gold price does not automatically reduce risk for new buyers. On June 19, the more important signal was not just that domestic quotes cooled, but that the buy-sell spread in the physical market still sat around VND 3 million per tael and reached VND 3.5 million at some dealers.VnEconomy

In plain terms, gold risk is not only about whether prices rise or fall. It also depends on how the asset is bought, stored, and sold back into the market. That is why the June 19 discussion around a potential gold ETF matters. The real issue is not whether a new product would push gold prices higher, but whether it could make the cost structure and risk profile of holding gold more transparent.Người Quan Sát

The core thesis is straightforward: if a gold ETF is introduced under a robust framework, it would not remove gold price risk, but it could move risk away from opaque frictions in buying, selling, and custody toward fees and processes that are disclosed more clearly. For first-time investors, that distinction matters more than simply watching whether gold is up or down on the day.

The first risk is not price, but the spread

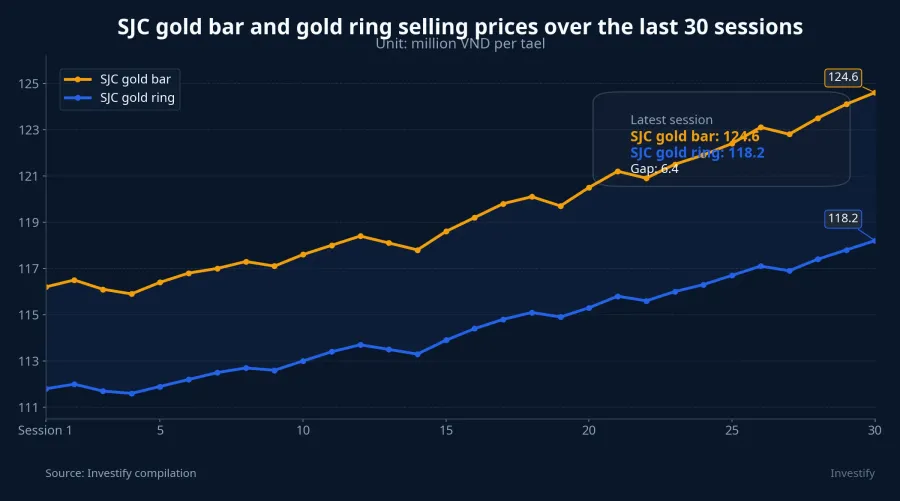

According to VnEconomy, SJC gold bar quotes at major dealers on the morning of June 19 fell to a range of VND 143.7 million to VND 146.7 million per tael. Investify's internal data also shows SJC gold bar selling prices at VND 146.7 million per tael on June 19, while SJC gold rings were at VND 145.1 million per tael. That marked a meaningful pullback from the previous day and confirmed that the market had adjusted quickly.VnEconomy

But the picture changes once the perspective shifts from watching quotes to actually buying and reselling. The same source said the buy-sell spread for SJC gold bars and 9999 gold rings was still commonly around VND 3 million per tael on June 19. At some names, including Bao Tin Minh Chau, Bao Tin Manh Hai, and Ngoc Tham, the spread for gold rings reached VND 3.5 million per tael.VnEconomy

That hits investors in a very direct way. If someone buys and then needs to sell back soon after, they can lose money even if global gold prices barely move, simply because the entry and exit spread is so wide. In other words, physical gold holders are paying an effective access cost that may not appear as a separate fee line, but still shows up in real returns.

For new investors, this is the easiest part to miss because physical gold feels safe. You can hold it, lock it away, and pass it on, so the instinct is to assume risk must be lower. In practice, that sense of safety often comes bundled with other costs: buy-sell spreads, storage costs, loss risk, verification risk, and the chance that dealers widen spreads when volatility rises.

What a gold ETF changes

A gold ETF is not a risk-free version of gold. In simple terms, it is a listed fund certificate, while the fund structure is designed to track the gold price within the legal framework that applies. Investors do not hold bars in hand; they hold an instrument that gives them exposure to gold price movements through market infrastructure.

The biggest difference is structural. With physical gold, buyers have to manage the entry point, the exit point, and custody themselves. With a gold ETF, those functions move to the fund, the custodian, and the exchange-based trading system. Investors give up the comfort of direct possession, but they may gain a clearer framework for fees, execution, and settlement.

That idea was highlighted in Người Quan Sát on June 19. Luong Thi My Hanh, Director of Domestic Asset Management at Dragon Capital Vietnam, said a gold ETF could bring part of the gold held by households into the fund system and connect a traditional savings habit with a more modern investment structure. The same article said Vietnam's market currently has more than 60 open-end funds and around 20 ETFs, with meaningful overlap across many portfolios.Người Quan Sát

The real point is not that the market needs just one more fund. The point is that a gold ETF, if launched, would create a different ownership format for an asset Vietnamese investors have long preferred to hold physically. That makes the key question less about novelty and more about which cost layers it removes and which risks it leaves in place.

More transparent does not always mean cheaper

In markets where comparable products already exist, the main benefit of a gold ETF is usually standardized access. Investors do not need to store gold themselves, verify each unit on resale, or rely entirely on retail dealer quotes. That is a structural advantage, not a promise of higher returns.State Street

SPDR Gold Shares, ticker GLD, had assets under management of USD 138,959.40 million as of June 18, 2026, with a 0.40% gross expense ratio. State Street also notes that for many investors, the cost of buying GLD in the secondary market and paying the fund's ongoing expenses may be lower than the cost of buying, storing, and insuring physical gold in a traditional bullion account.State Street

iShares Gold Trust, ticker IAU, carries a 0.25% annual expense ratio, lower than GLD from a fund-fee perspective.iShares But that still does not mean every gold ETF is cheaper than physical gold in every setting. Physical holders do not see an explicit annual management fee, but they pay through spreads and other hidden frictions. ETF holders pay more visible fees in exchange for lower custody burden and exchange-based trading.

So this is a trade-off, not a total replacement. If the goal is to accumulate physical gold, lock it away, and keep it as a long-term store of value, gold bars and rings still have their own role. If the goal is to add gold price exposure to an investment portfolio, a gold ETF could be a more compact structure if it is designed transparently and operated under tight standards.

The real issue for new investors is risk structure

The bigger picture points to a better question than whether gold has fallen enough. The better question is what kind of risk the investor is paying for. With physical gold, that cost usually sits in the spread, custody, and the resale process. With a gold ETF, it is more likely to show up in management fees, trading costs, and acceptance of a more centralized custody model.

That is also why there is not enough evidence to turn a potential gold ETF into a simple bullish story for gold itself. The June 19 Người Quan Sát article only frames it as an expected product and discusses what role it could play in channeling household gold into formal investment structures.Người Quan Sát In other words, this is a market-structure story worth watching, not a regulatory change already in force.

That is where the conclusion should stay. A lower gold price is not enough to say risk has fallen, because for real buyers, risk also sits in the holding format itself. If a gold ETF is launched under the right standards, it may not make gold safer in any absolute sense, but it could make the costs and process far easier to see. The signals worth tracking next are whether the product clearly defines its pricing benchmark, who the custodian is, and whether the fee schedule is transparent enough for retail investors to compare directly with physical gold.