On June 18, Brent crude slipped back to around USD 78.02 a barrel, yet spot gold did not fall with it and SJC gold bars still traded above VND 151.3 million per tael. At first glance, those three prices look out of sync. For new investors, though, this is a useful lesson: oil, global gold and SJC gold may all look defensive, but they are not answering the same market question.

The simplest way to read it is this. Oil measures fear around the physical flow of energy, especially when markets worry about supply routes through the Middle East. Spot gold captures a broader mix that includes geopolitical stress, interest-rate expectations and the US dollar. SJC adds another domestic layer on top of global gold, shaped by local supply-demand conditions, exchange rates and the premium embedded in Vietnam's market structure.

Three prices, three signals

If investors rely on a single reflex that says "risk is easing, so every safe-haven asset should fall," they are likely to misread the market. Prices do not only reflect fear. They also reflect which market is repricing fastest, which transmission channel is strongest and which instruments are still being held up by domestic frictions.

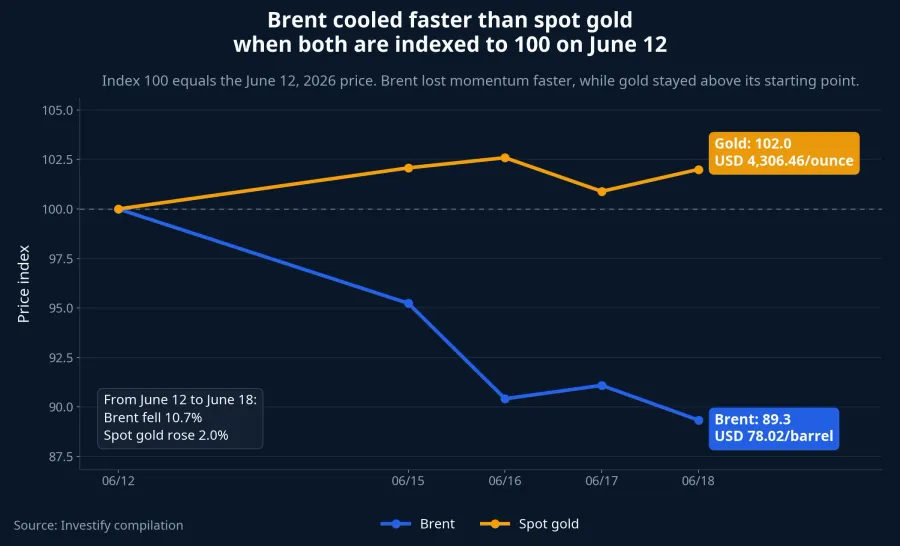

Brent is the clearest example. From June 12 to June 18, Brent dropped from USD 87.33 per barrel to USD 78.02, a decline of roughly 10.7%. Even if we narrow the window to June 15 through June 18, the contract still fell about 6.2%. That is large enough to say a meaningful part of the supply-disruption premium has already been taken out.

CafeF reported that oil lost more than USD 2 per barrel on June 18 after the US and Iran reached a temporary deal that reopened the Strait of Hormuz and eased immediate concern over Iranian crude flows.CafeF Oil typically reacts fast because it is a global market with deep liquidity and a direct link to shipping, inventories and physical supply expectations.

The market does not need every operational issue to be fully resolved before oil falls. It only needs the probability of disruption to decline. In practical terms, Brent behaves like a thermometer placed right next to the pipeline. When the risk of blockage eases, that thermometer cools first.

Why spot gold did not move in lockstep

Spot gold is also a defensive asset, but it is not driven by one variable alone. Over the same June 12 to June 18 period, gold rose from USD 4,222.00 per ounce to USD 4,306.46, an increase of about 2.0%. Over the shorter June 15 to June 18 window, it was almost flat, slipping just 0.07%. In other words, gold did not confirm the same pace of cooling that oil did.

That should not be read as a contradiction. Spot gold reflects interest-rate expectations, the direction of the dollar, bond yields and defensive demand from large pools of capital all at once. A headline that reduces concern over oil supply can push Brent down immediately, but it may not be strong enough to send gold lower if markets still think global rates will stay elevated or if investors still want portfolio protection.

This is where many first-time investors get tripped up. They treat oil and gold as two versions of the same risk gauge, one for energy and one for safe-haven demand. In reality, gold behaves more like a dashboard with several switches. One switch can turn down while the others keep the price supported.

That also helps explain why spot gold rose 1.10% during the June 18 session even as Brent fell 1.92%. The broader backdrop was the same, but the transmission channels were different. Oil responded to supply expectations, while gold kept trading within a wider monetary and defensive framework.

SJC is not a copy of world gold

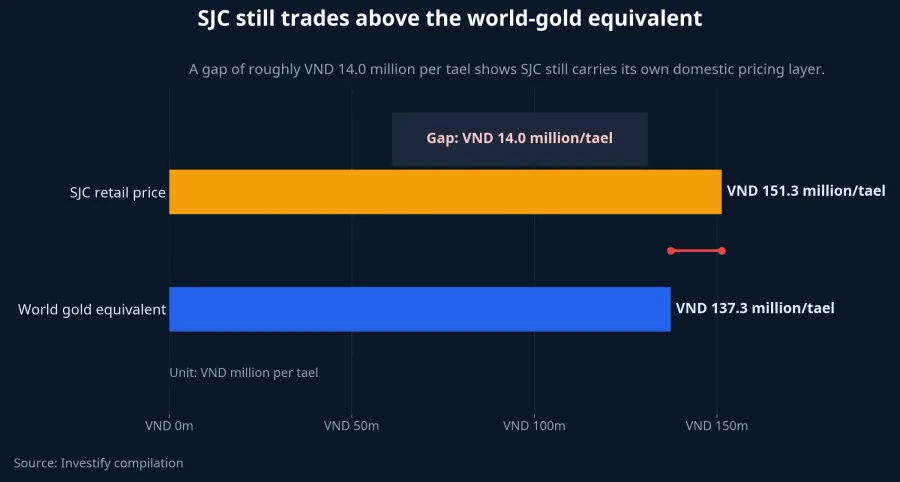

If oil and world gold are already different, SJC is a separate story again. On June 18, SJC's selling price stood at VND 151.3 million per tael, while the world-gold equivalent translated into Vietnam dong was around VND 137.3 million. That gap of nearly VND 14.0 million per tael is the number domestic buyers need to focus on, rather than assuming SJC will mirror international prices in real time.Báo Đà Nẵng

Báo Đà Nẵng said that as of 5 p.m. on June 18, several major dealers were quoting VND 148.8 million per tael to buy and VND 151.3 million to sell, leaving a buy-sell spread of about VND 2.5 million per tael.Báo Đà Nẵng That spread tells a practical story: SJC buyers are not paying only for the direction of world gold. They are also paying for local market structure and the safety margin that domestic dealers leave in the quote.

From June 15 to June 18, SJC's retail price even rose from VND 150.5 million per tael to VND 151.3 million, or about 0.5%. Over the same window, Brent fell sharply and spot gold was essentially flat. That is a fairly clean sign that SJC is being supported by a domestic layer of demand rather than simply echoing international pricing hour by hour.

The exchange rate adds another layer. Investify's internal data showed USD/VND at VND 26,318 on June 17. Vietnamnet also reported a free-market rate near VND 26,400 for buying and VND 26,420 for selling on the same day.Vietnamnet If the exchange rate does not ease meaningfully and the SJC premium remains wide, domestic retail prices can stay elevated even after oil has already repriced the geopolitical headline.

What new investors should take away

The key point is not simply that oil fell or that gold rose. The key point is that each price is measuring a different layer of risk. Brent tells us how much the market is still willing to pay for possible disruption in energy supply. Spot gold tells us how global capital is weighing rates and portfolio protection. SJC tells us how much extra domestic savers in Vietnam still have to pay for a local pricing layer.

That means the right question is not "if oil falls, should gold fall too?" The better question is this: how much of the oil supply-risk premium has already come out, what is still supporting world gold, and is the SJC premium over the converted global price narrowing or staying wide? Once those questions are separated, new investors are less likely to look at one price and assume it speaks for the whole market.

It is also important not to force every move into a single causal story. There is not enough evidence to say the US-Iran development alone explains all of spot gold or all of SJC. For global gold, rates and the dollar remain major parallel drivers. For SJC, local demand, dealer spreads and holding psychology are more plausible explanations for why retail prices are not moving in step with Brent. The relationship here is largely one of timing, not proof that one event mechanically drove every line on the board.

That leads to one clear thesis. As of June 18, oil-supply risk had cooled first, world gold was still being supported by other channels, and SJC still carried an additional domestic pricing layer. As long as the gap between SJC and the converted world-gold price stays wide, new investors should treat SJC as an asset with its own mechanism rather than a real-time mirror of spot gold.

The next few sessions should be watched through those same three layers. Does Brent keep falling below the USD 78 per barrel area. Does spot gold lose the USD 4,300 per ounce level if rate expectations shift. And most importantly for cash holders in Vietnam, does the SJC premium over the converted world price narrow, or does it stay stuck in the double-digit million-dong range per tael. Those questions will say far more than looking at one gold quote and trying to infer the mood of the entire market.