At first glance, this looks like a dry regulatory tweak. In practice, it touches one of the most sensitive parts of a bank's balance sheet: how much short-term funding can be used to support medium- and long-term loans. On June 17, the State Bank of Vietnam released a draft amendment to Circular 22/2019 that would raise that cap from 30% to 40%.VietnamFinance

The first point to keep straight is legal status. This is still a draft, not an effective rule. The right reading is not that banks have already been granted more room, but that they could face less pressure to secure long-term funding if the proposal is eventually issued.CafeF

What the 30% cap is really constraining

The basic mismatch is simple. Depositors usually lend to banks for a much shorter period than mortgage borrowers, infrastructure developers or companies investing in equipment. Banks therefore live with a constant maturity mismatch, using shorter-duration liabilities to fund longer-duration assets.

The short-term funding ratio for medium- and long-term lending is designed to limit that mismatch. With the cap at 30%, banks can only use a narrower share of their short-term funding base for longer-tenor loans. If they want to expand housing, infrastructure or other longer-cycle credit, they need to find more stable long-term funding through longer deposits, certificates of deposit, bank bonds or equity.VietnamFinance

That matters because long-term funding is usually more expensive than short-term funding. Once several banks are competing for the same longer-tenor deposits, funding costs begin to rise. So this ratio is not just a safety metric. It feeds directly into funding costs, net interest margin pressure and how aggressively banks can extend long-duration credit.CafeF

Why a return to 40% matters

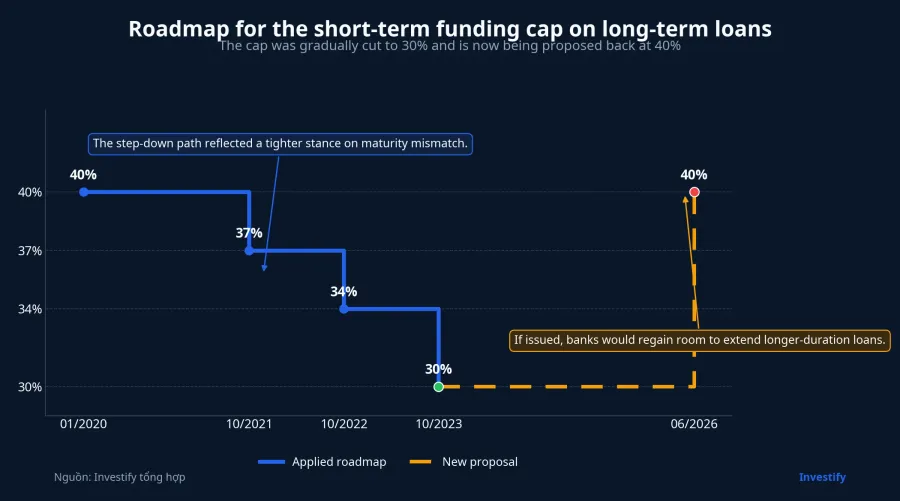

The 40% level is not unprecedented. Under the previous roadmap, the ratio stood at 40% from January 2020 through September 2021, then stepped down to 37%, then 34%, and finally to 30% from October 1, 2023.VietnamFinance

That sequence shows a multi-year tightening path aimed at reducing maturity mismatch risk. If the new draft is issued, it would not create an entirely new framework. It would restore the system to a looser setting that existed before, at a time when demand for longer-duration credit remains significant.CafeF

For less experienced investors, this is easy to miss because bank stories are often reduced to stock prices or listed deposit rates. But a technical ratio like this can reshape how banks fund themselves, how much they must pay for long-tenor liabilities and how much room they retain to lend into longer-duration projects without crushing margins.

How the proposal could flow into funding costs

If the cap stays at 30%, a bank that wants to expand medium- and long-term lending usually has to secure more long-term funding first. The most direct tools are raising long-tenor deposit rates or issuing funding instruments. When many banks do that at once, system-wide funding costs are hard to keep contained.

If the cap moves to 40%, some of that pressure could ease. Banks would gain more room to work with their existing funding base instead of paying up for every additional unit of long-term money. That does not guarantee lower deposit rates, but it would make it easier for long-tenor funding costs to stabilize rather than climb solely because of balance-sheet pressure.VietnamFinance

There is still a trade-off. A higher cap also means banks are allowed to fund more long-duration assets with short-duration liabilities. If liquidity management is weak, a reversal in rates or faster deposit withdrawals would expose that mismatch more quickly. In other words, the draft can make the funding problem easier, but it cannot replace discipline at the bank level.

The benefit is unlikely to be uniform

This is where many retail investors could overread the story as a sector-wide positive. It is not that simple. Banks with larger housing, infrastructure, real estate or other long-duration lending books have more reason to use the extra room than lenders focused on shorter-cycle credit.

Even inside that group, the advantage depends on funding structure. Banks with sticky retail deposits, lower funding costs and less dependence on rate-sensitive money are better positioned to turn regulatory flexibility into durable earnings support. Banks that constantly need to defend deposits with higher rates will not automatically convert a looser cap into sustainable profitability.

CafeF also reported that the draft would adjust how deposits are counted for the LDR calculation. Non-term deposits from the State Treasury would continue to be excluded, while only 80% of term deposits from the Treasury would be excluded, or another ratio set by the SBV Governor.CafeF

That should not be stretched into a blanket positive for the whole sector. It matters most for banks with meaningful Treasury deposits in their funding mix. The practical lesson is that policy needs to be read through the balance sheet, not just through headlines.

June 17 showed a split market reaction

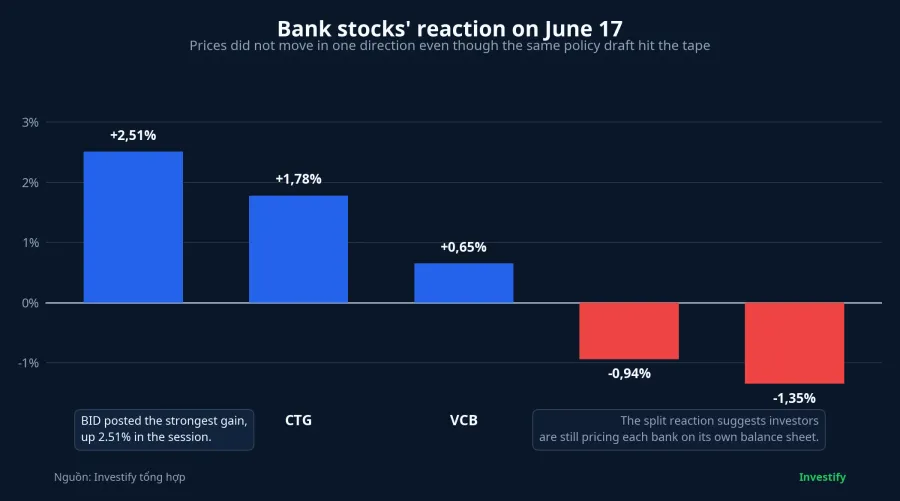

The market action on June 17 reflected that nuance. The VN-Index closed at 1,806.20, down 0.10%. Among large bank names, BID rose 2.51% to VND 42,950 per share, CTG gained 1.78% to VND 34,300, and VCB added 0.65% to VND 62,200. TCB, however, fell 0.94% to VND 31,450 and ACB slipped 1.35% to VND 22,000.

Those numbers are not enough to prove that the draft directly caused each move. The market was also pricing asset quality, credit growth, capital pressure and earnings expectations bank by bank. What the evidence does support is a non-uniform reaction, which fits the idea that any eventual benefit from the proposal would be selective rather than broad-based.

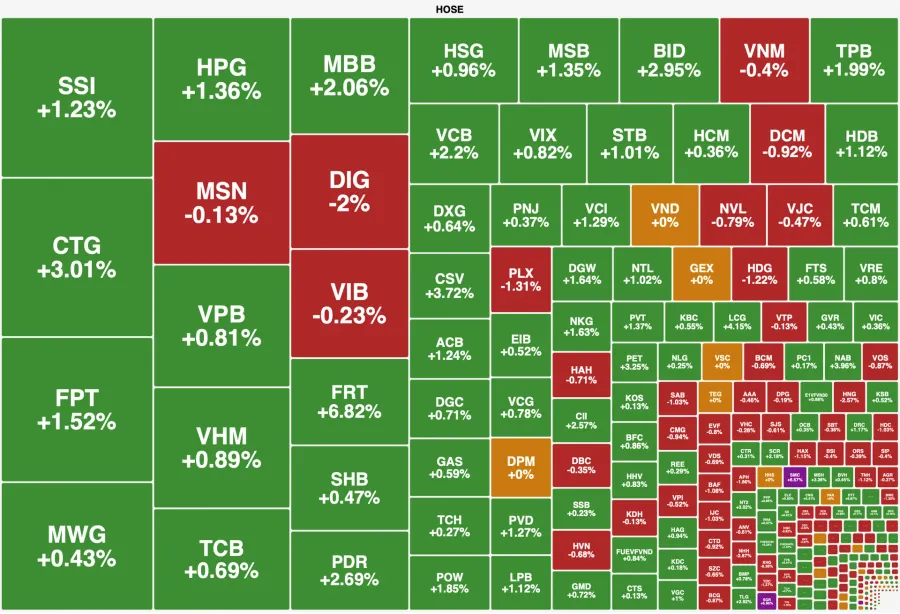

The broader market board told the same story. Financial names were not moving as one block. For newer investors, that is a useful reminder that a single macro or policy headline rarely translates into identical upside for every stock in the same sector.

Conclusion: real relief, but only durable for strong funders

The core thesis is straightforward. If the draft is eventually issued, it could ease pressure on banks to secure expensive long-term funding, and that would be a genuine support for longer-duration credit growth. But the more durable upside would likely accrue to banks with stable funding bases, lower costs of funds and tighter liquidity discipline, not to every lender simply because it sits inside the banking sector.

That is why the better follow-up is not which ticker benefits immediately. The more useful checklist has three items. First, monitor the legal progress of the draft, because for now the impact is still conditional. Second, watch long-tenor deposit rates, which are the clearest transmission channel. Third, track each bank's funding quality and loan mix in upcoming reports.

If those three signals move in a supportive direction, the 40% reset could become more than a technical footnote. It could materially reduce long-term funding strain for part of the system. If not, and if funding remains fragile while the race for long-term deposits continues, the extra room would look more like temporary relief than a lasting advantage.