Two straight limit-up sessions can easily tempt newer investors into a very simple reading: good news arrived, the stock jumped, end of story. With HVN, that is only the surface. The move on June 15 and June 16 came just ahead of Vietnam Airlines’ 2026 annual general meeting, at a moment when the market was also processing fresh signals on earnings, international routes and input costs.Dân trí

What makes that more important is that HVN is not some anonymous speculative ticker. As of the end of 2025, Vietnam Airlines had 27,203 shareholders, with nearly 98% of them domestic. When a company with that many retail holders heads into an AGM packed with key agenda items, the stock usually starts pricing not only near-term profit expectations, but also how credible the next leg of the restructuring story looks.Dân trí

Three layers of expectation are moving together

Break the story apart and the market appears to be combining at least three pieces into one trade. The first is the price action itself moving ahead of a clear corporate milestone. Dân trí reported that HVN closed limit-up at VND 24,150 per share on June 16, with trading volume above 4.2 million shares, after already posting another limit-up session the day before.Dân trí

The second is that the corporate calendar is now close enough that the market has to price it in before the event. Vietnam Airlines said its 2026 AGM is scheduled for June 28, and the meeting materials include updates on restructuring through end-2025, the first phase of the charter-capital increase, and the 2026 business plan.Vietnam Airlines

The third is that supporting signals arrived at the right time. As Q1 earnings were recirculated in the press on June 17 and the direct Hanoi-Amsterdam route had just launched on June 16, investors gained a reason to stitch those pieces into a broader narrative: the national carrier is not only restoring revenue, but also trying to reclaim margin-bearing international routes.Báo PLCAA

Read that chart carefully and the point is not just the last two sessions. The market is effectively testing a higher valuation band before the AGM even begins, as if it is asking the company a harder question in advance: if the recovery story is real, what else can you prove over the next ten days?

Q1 earnings make the recovery base harder to dismiss

The strongest layer of expectation still sits in operating results. The Doanh nhân & Pháp luật section of Báo Pháp luật Việt Nam reported that Vietnam Airlines posted consolidated revenue of more than VND 37.5 trillion and net profit of VND 4,514 billion in the first quarter of 2026.Báo PL

For newer investors, that matters because it changes the way the market can talk about HVN. A company emerging from years of restructuring and once again generating profit on a multi-trillion-dong scale stops looking like a ticker waiting to be rescued. At that point, the market starts asking the harder follow-up: can this level of profitability repeat?

That is also what makes this rally different from a short-lived event trade. Without the Q1 profit base, Amsterdam and the shareholder meeting would be catalysts and little more. With that profit base back in view, every new development has more room to amplify expectations.

That still calls for discipline. One strong quarter is not enough to declare every legacy issue solved. It is enough, though, to show that the company has reached a phase where the stock can start reflecting the quality of the recovery rather than simply the hope that the company can survive its hardest stretch.

Amsterdam strengthens the international leg of the thesis

If Q1 profit is the foundation, the Hanoi-Amsterdam route is the expansion layer that makes the story more compelling. The Civil Aviation Authority of Vietnam said Vietnam Airlines officially launched the direct route on June 16; the inaugural VN83 flight departed Nội Bài at 3:50 a.m. with nearly 300 passengers, operated by an Airbus A350, and will run three round trips per week.CAA

What the market cares about is not the ceremony, but what this route means inside the wider international network. SGGP reported that after adding Amsterdam, Vietnam Airlines now operates 12 direct routes between Vietnam and Europe, linking eight destinations.SGGP For a flag carrier, the number of destinations is not just a branding metric. It affects feed traffic, passenger mix and the ability to hold yields on long-haul routes.

This is also where causal discipline matters. It would be too strong to say HVN hit limit-up because of Amsterdam alone. The price move may be reflecting several things at once: Q1 results being pulled back into circulation, pre-AGM positioning, short-term money chasing a clear narrative, and the positive backdrop from falling oil. What Amsterdam does show is that the airline’s international strategy is still being pushed forward rather than merely defended.

Put differently, the new route makes the recovery thesis more tangible. The market is not only looking at the fact that Vietnam Airlines is profitable again. It is also watching how the airline uses that restored profitability. If the answer is deeper exposure to higher-value international corridors, the stock has a case to be priced as a company rebuilding growth, not just repairing its balance sheet.

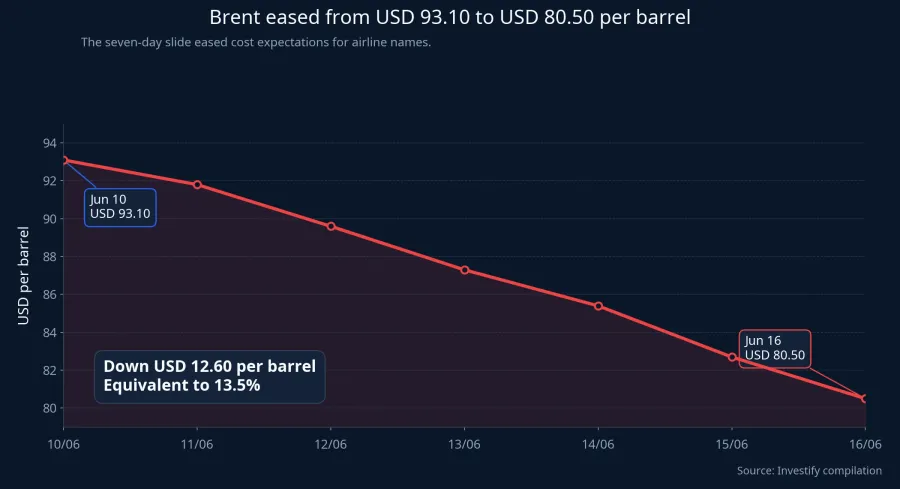

Cheaper oil is a catalyst, not a full explanation

Over the same stretch, internal data show Brent falling from USD 93.10 per barrel on June 10 to USD 80.50 on June 16, a decline of about 13.5% in seven days. For airline stocks, that clearly helps sentiment because it opens the door to lower fuel-cost expectations in the near term.

But it would be a leap to treat that as the full answer for HVN. If oil were the whole story, the reaction should be broader and more even across transport names, rather than concentrating so sharply in a stock heading into its AGM and a newly launched European route. Lower oil makes the macro backdrop less hostile; it does not create a corporate recovery thesis by itself.

Newer investors often get pulled toward a single trigger because one cause is easier to remember and easier to repeat. Markets rarely work that neatly. In HVN’s case, the better reading is that cheaper oil makes an existing story easier to believe. It does not replace the proof the company still needs to provide through operating results and capital plans.

The real test sits beyond June 28

The current move only holds if the AGM answers three questions. The first is how far restructuring has actually progressed after the 2025 phase, and how much of that progress has translated into a cleaner picture on capital, debt and cash flow for shareholders to read.Vietnam Airlines

The second is how the international leg will prove itself in operating terms. An inaugural flight with nearly 300 passengers is a good sign, but the real economics only show up if the airline can sustain load factors, ticket pricing and connection traffic on long-haul routes. If Amsterdam looks strong only on day one, the market will strip that expectation back out very quickly.CAA

The third is whether the return of profitability can withstand volatile inputs. Oil has fallen over one week, but fuel and FX can both reverse quickly. An airline truly enters a more durable recovery phase only when profit is no longer easily knocked off course by a single input swing.

That leaves the clearest thesis intact: the market is paying for a more credible recovery phase at HVN, not merely for two limit-up sessions. Q1 earnings, the Amsterdam route and lower oil are all supporting that thesis. But the deciding factor is still whether Vietnam Airlines can turn those expectations into a more convincing balance sheet and a more durable growth path after the June 28 AGM. If the meeting sharpens that proof, the rally has a stronger base. If it does not, the market will have to reprice the enthusiasm that has already run ahead.