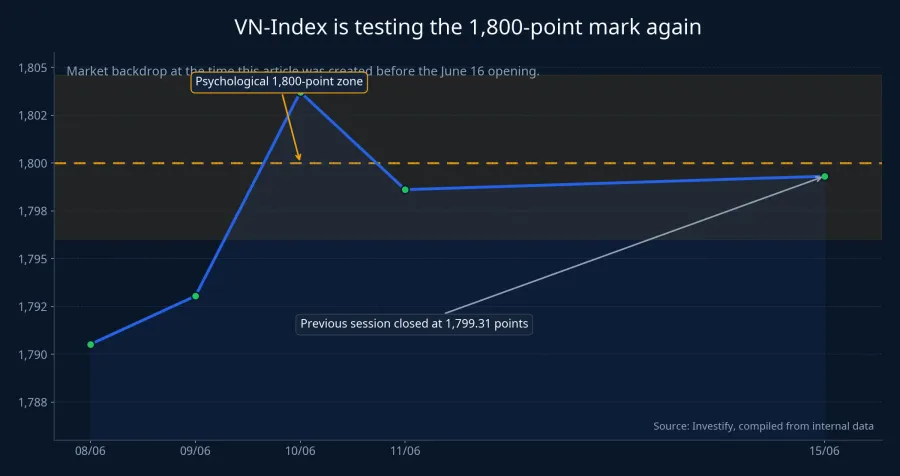

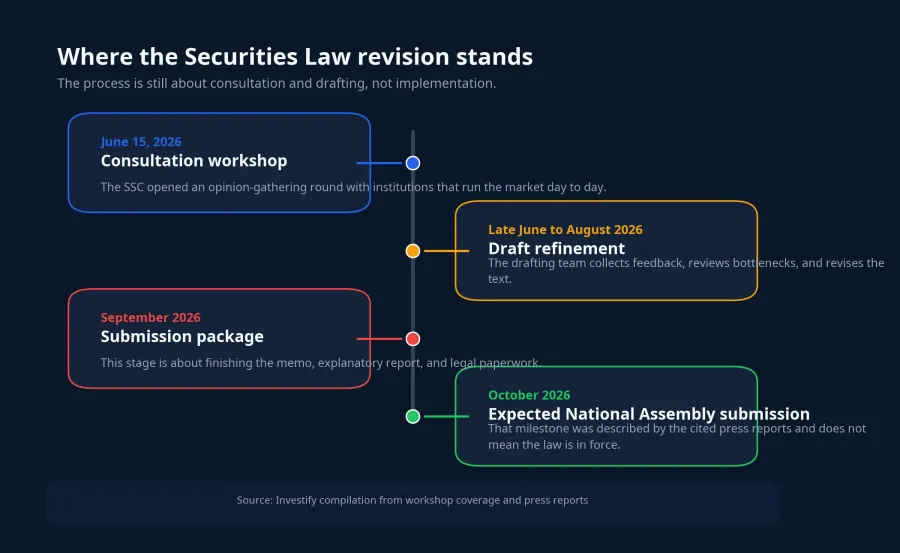

The VN-Index is sitting just below the 1,800-point mark after the previous session closed at 1,799.31. For many new investors, that is exactly the kind of number that pulls all attention toward the screen: the board looks greener, confidence rises quickly, and the next trade starts to feel urgent. Yet while the market is focused on that visible layer, a more important story for beginners is unfolding underneath it: Vietnam’s State Securities Commission held a consultation workshop on the draft revision of the Securities Law on June 15.VnEconomy

What matters here is not simply that a meeting took place. According to Tạp chí Kinh tế Tài chính, the workshop drew more than 100 delegates from public companies, securities firms, fund managers, custodian banks, supervisory banks, and related institutions.KTTC Put plainly, the people who run the market every day were invited to identify the places where the system remains harder to trust, harder to read, and less safe than it should be for newcomers.

The 1,800-point mark is only the surface

The easiest way to frame this is simple: the tape tells you about short-term emotion, while the law tells you about long-term market quality. An index can clear a psychological level for any number of short-term reasons, from a sector-led rebound to a burst of trading liquidity. But if disclosure remains fragmented, listed products still mix high-quality and low-quality issuers too loosely, and the market’s plumbing is not keeping up with trading scale, the people who usually pay the highest price are the retail investors arriving last.

Why the law is being revised now

The 2019 Securities Law remains the main framework for Vietnam’s market today. But after more than five years in operation, the market itself has changed: electronic trading is more widespread, social-media stock advice is more complicated, the retail investor base is larger, and the push for a market upgrade now demands higher operating standards.Báo Đầu tư The existing framework is not necessarily broken, but parts of it are no longer clear enough or tight enough for the market Vietnam now has.

Báo Đầu tư reported that the Ministry of Finance has submitted a proposal to the government to add the draft law to the 2026 legislative program, with the current timetable pointing to a submission to the 16th National Assembly at its second session in October 2026.Báo Đầu tư That detail sets the stage correctly: the process is still in consultation and draft refinement, not implementation. Its first effect sits in expectations around medium-term market quality, not in a trading cue for the next session.

First layer: information has to become easier to trust

For beginners, the biggest risk is not always a lack of chart-reading skill or a weak grasp of financial statements. A bigger risk is not knowing which information deserves trust in the first place. If companies disclose late, disclose incompletely, or force investors to piece together essential facts across multiple channels, late-arriving investors start from a structural disadvantage.

That is why the draft’s focus on disclosure, e-trading, and securities practitioners deserves close attention. VnEconomy reported that the draft is aimed at simplifying business conditions and administrative procedures while also adding legal foundations for areas such as regulatory sandboxes, bond payment guarantors, electronic trading, and securities practitioners.VnEconomy If account opening, verification, audit trails, and dispute resolution all sit inside a clearer legal framework, the market becomes less dependent on hearsay and recommendations that leave no trace.

Second layer: the products listed on the market have to be screened more tightly

A healthy market is not defined only by the number of listed names or the amount of capital raised. New investors need product quality more than they need product quantity. If an issuer raises money with weak documentation, unclear use-of-proceeds language, or loose accountability after issuance, the first party to absorb that risk is the person providing the capital.

In that sense, Decree 200/2026/ND-CP is a recent example of how regulation is already moving toward tighter post-fundraising accountability. Báo Chính phủ reported that the decree was issued on June 5, 2026, with 8 chapters and 51 articles covering domestic private placements of corporate bonds, secondary trading, and overseas offerings.Báo Chính phủ The decree requires issuers to use proceeds for the stated purpose, segregate bond proceeds, and take responsibility for the accuracy, honesty, and completeness of issuance documents.Báo Chính phủ

One detail that first-time investors should remember is the 65% approval threshold. If an issuer wants to change terms, conditions, or the purpose of a domestic bond issue, it needs consent from bondholders representing at least 65% of the outstanding bonds of that type.Báo Chính phủ That is not just a bond-market detail. It reflects a broader regulatory direction: anyone raising money from investors should be tied more tightly to disclosure, explanation, and accountability after the money has been collected.

Third layer: infrastructure shapes whether the market feels safe

Many investors think of law mainly as a tool for punishment. In reality, law also determines what happens after you hit buy or sell: who holds the assets, who clears the trade, who supervises the process, what data are recorded, and who bears responsibility when a failure occurs. For people who trade regularly, that part may attract less attention on daily news feeds, but it directly affects how safe the market feels to join.

Báo Đầu tư noted that the law revision is tied to international integration and Vietnam’s goal of moving its stock market into a higher classification.Báo Đầu tư To meet that standard, the market needs more than fresh capital. It also needs trading and post-trade mechanisms that investors can trust. For beginners, this is the layer that reduces the cost of entering a market that still contains too many blind spots.

What first-time investors should watch through October

Between now and the expected October 2026 submission point, there are three signals worth watching closely. First, does the final draft keep its focus on disclosure, electronic trading, and standards for market practitioners? Second, are the duties of securities intermediaries and fundraising issuers written clearly enough to narrow the market’s gray zones? Third, do the rules around infrastructure, custody, and supervision move from broad policy goals into operational mechanisms that investors can actually rely on?VnEconomyBáo Đầu tư

One point is worth stating plainly: the issue is not whether a revised law automatically produces a better market overnight. The real effect will depend on the details of the draft and on how the final rules are enforced. But the direction is already clear enough to support a firm conclusion. While many investors are watching whether the VN-Index can clear 1,800, first-time investors would gain more from watching whether the market’s foundation is being reinforced in a way that makes it easier to read and easier to trust.