Japan has just done something much of Asia had stopped treating as imminent: it lifted its short-term policy rate to 1.0%, the highest level since 1995.BoJTrading Economics The larger takeaway is not confined to Tokyo. When the economy most associated with deflation, a weak yen, and ultra-cheap capital starts to normalize more decisively, investors across Asia have to rethink how they price risk.

This story should not be read as "Japan hikes, markets panic." The Bank of Japan only added 0.25 percentage points, taking the policy rate from 0.75% to 1.0%.AP But after years of near-free money, 1.0% matters less as a technical increment and more as a regime marker.

From negative rates to positive territory

To understand why 1.0% matters, it helps to revisit the starting point. On January 29, 2016, the BoJ pushed Japan into the era of negative rates with a -0.1% setting, part of a broader easing push meant to fight deflation and lift inflation expectations.BoJTrading Economics Back then, the goal was not to cool the economy. It was to force capital out of inertia and back into lending, investment, and spending.

Japan did not leave negative rates until March 2024, when the short-term policy range returned to 0-0.1%.BoJAP That means the June 16, 2026 decision was not the first turn, but it was the first moment in this cycle when markets had to admit the normalization process had moved into a new gear. Once policy is no longer merely above zero but at 1.0%, the signal to the rest of Asia becomes harder to ignore: ultra-cheap capital is no longer a standing assumption.

Why the BoJ kept moving

At first glance, some investors may wonder why the BoJ kept tightening when inflation is not obviously running away. In its June 16 statement, the central bank said core CPI was running around 1.5%, still below its 2% target.BoJ But the issue is not only the latest headline figure. The BoJ is increasingly focused on whether energy and input costs keep passing through into consumer prices while medium- and long-term inflation expectations continue to edge higher.

That is why the Japanese policy problem now looks different from the one investors got used to for years. The old fear was chronically weak inflation, timid corporate pricing power, and consumers with little reason to spend sooner rather than later. The newer risk is that price increases become more persistent if companies start passing along raw-material, energy, and wage costs more systematically.

This also explains the BoJ's measured tone. The statement still says financial conditions remain broadly supportive, but it also makes clear that rates can keep rising if economic, price, and financial data evolve in line with its outlook.BoJ For new investors, that is the key distinction: the BoJ is not suddenly slamming the brakes, but it is no longer defending a world of permanently cheap money.

Why the yen did not surge

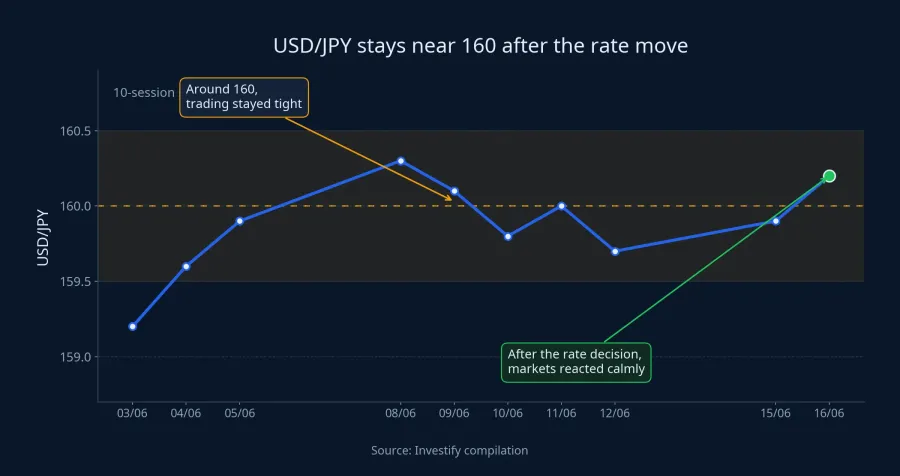

A major policy shift on paper does not always translate into a dramatic first-day market move. After the BoJ decision, the U.S. dollar barely moved against the yen, slipping from JPY 160.33 to JPY 160.32 according to AP.AP Investify's internal data also show USD/JPY at 160.21 on June 15, only modestly below the 160.35 area seen on June 10.

That calm reaction has at least three plausible explanations. First, the move had already been priced in: a Reuters poll cited by FXStreet showed 94% of economists expected the BoJ to raise rates to 1.0% in June.FXStreet Second, the Japan-U.S. rate differential remains wide, so one BoJ move is not enough to instantly rewrite how currency markets price the yen. Third, the BoJ left the door open to further hikes without signaling an aggressive sprint, giving traders little reason to price in a sharp policy break.

Put differently, the yen is not weak only because the BoJ was passive, and it will not strengthen on headlines alone. It reflects rate differentials, growth expectations, demand for U.S. dollars, and the attractiveness of borrowing yen to buy higher-yielding assets elsewhere. When one link in that chain starts to shift, the impact usually arrives in layers rather than in a straight line.

Japanese equities did not behave like a panicked market

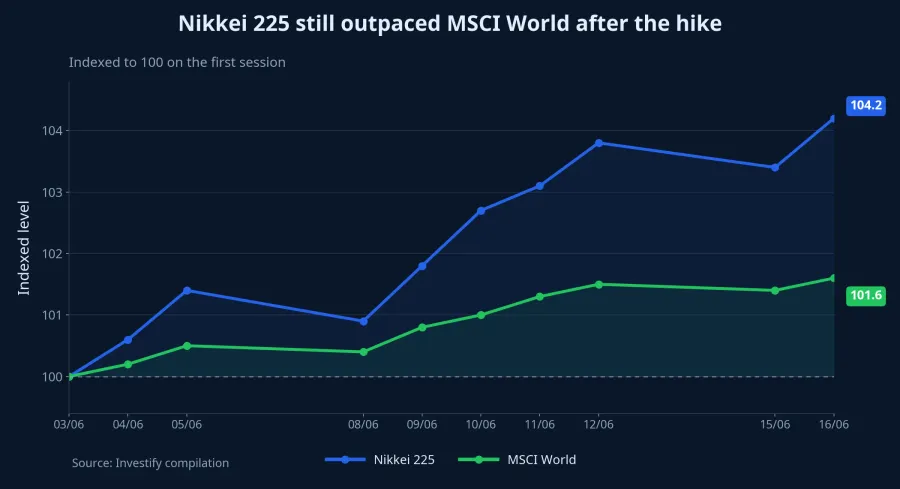

If investors had truly read the BoJ move as an abrupt brake on risk assets, Japanese equities would have traded very differently. On June 16, the Nikkei 225 briefly moved above 70,000 before closing at 69,404.50, up 0.1% on the day according to AP.AP Investify's internal data put the index at 69,466 the same day, down 0.1% in the session but still up 8.2% from a week earlier.

That tells us the Japanese equity market is reading the rate decision through a more nuanced lens than the reflexive "higher rates are bad." As an economy moves away from a world of excessively cheap capital, the upside is that investors can have more confidence in nominal growth, corporate earnings, and companies' ability to sustain higher pricing. The negative response only becomes more acute if rates rise too fast or begin to damage profits directly.

By global standards, Japan is still nowhere near a truly restrictive rate regime. MSCI World stood at 4,865.20 on June 16 in Investify's internal data, up 1.2% in a single day. The current setup therefore fits the thesis of a gradual repricing in the cost of capital far better than it fits a story about global money fleeing risk assets outright.

What Vietnamese investors should actually monitor

For retail investors in Vietnam, the right question is not whether the VN-Index will open green or red tomorrow because Japan hiked rates. The more relevant link runs through funding costs, exchange rates, and global risk appetite. Japan has long been one of the world's major sources of cheap capital; as rates rise there, borrowing yen to chase higher yields elsewhere gradually becomes less comfortable.

That does not mean capital will immediately reverse out of Vietnamese equities or Asian corporate bonds. It does mean investors need to be clearer about which assets were lifted mainly by cheap liquidity and which ones have cash flow strong enough to hold up under a less forgiving funding backdrop. Stocks supported only by distant narratives are more exposed than companies with visible earnings, healthy balance sheets, and resilient margins.

At a deeper level, the BoJ decision is also a reminder that there are fewer and fewer central banks willing to preserve cheap money simply to protect market sentiment. If the economy that spent the longest defending ultra-low rates is now moving away from that stance, valuations across gold, bonds, growth stocks, and Asian currencies will eventually have to reflect that reality. The process may be slow, but the direction is clearer than it was before.

Conclusion: the role change matters more than the one-day move

The central thesis here is not about a one-session swing in the yen or the Nikkei 225. It is about the fact that Asia's last major symbol of ultra-cheap capital is stepping out of its old role. With the BoJ now at 1.0%, markets are not panicking, but expectations around the cost of capital have already started to shift.

In the next few weeks, the variables worth watching are Japan's inflation path, the response in Japanese bond yields, and whether USD/JPY remains anchored near 160. If those signals keep supporting the normalization story, investors will need to price assets on a different assumption: cheap capital still exists, but it is no longer as cheap as it used to be, and it is certainly no longer guaranteed.