When a new ETF hits the screen, the natural instinct is to focus on the label and ask whether the theme sounds compelling. For first-time investors, that is the wrong starting point. The safer order is to look beneath the label and study the index basket first. If you do not know which index the fund tracks, how that index screens stocks, and how the fund trades on the exchange, you are still making a buy decision in the dark.

On June 16, 2026, VinaCapital listed two strategic ETFs on HOSE: VINACAPITAL VNMITECH under ticker FUEMITEC and VINACAPITAL VN50 GROWTH under ticker FUEVN50G. The important point is not simply that the market has two more fund products. The more useful point for investors is that neither fund is built as a plain “buy the whole market” vehicle. Both track indices that have already been filtered by theme or by growth style.CafeF

That distinction matters because it changes the kind of risk you are buying. A broad-market ETF is closer to moving with the market’s baseline. A thematic ETF tilts your portfolio toward a narrower slice of the economy. When the market is rewarding that slice, the fund can outperform the benchmark. When leadership rotates and valuation preferences change, the same tilt can widen drawdowns and make the ride less comfortable.

Strong early performance is not the whole answer

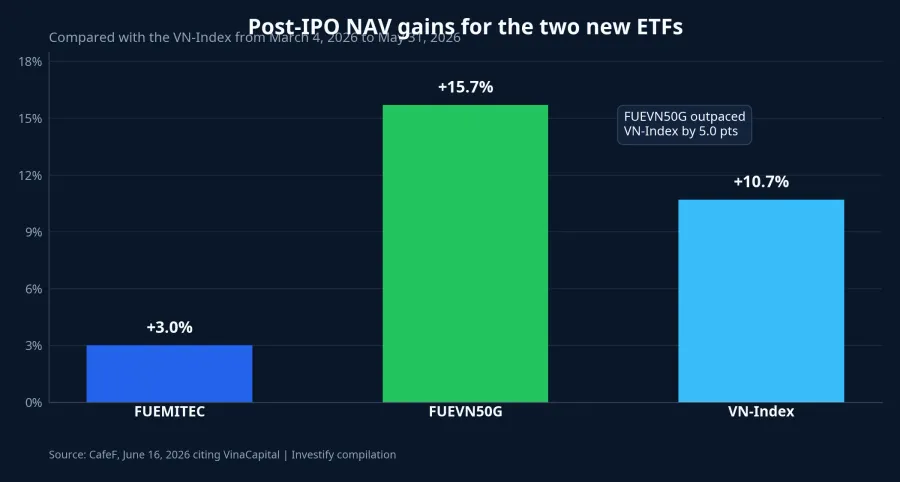

CafeF reported that from the end of the IPO on March 4, 2026 to May 31, 2026, FUEMITEC’s NAV per fund certificate rose by about 3.0%, FUEVN50G gained about 15.7%, and the VN-Index rose 10.7% over the same period.CafeF On the surface, FUEVN50G is the more eye-catching name because it beat the VN-Index in its first post-IPO stretch. For a new investor, though, that is a prompt to read further, not a conclusion to buy.

The reason is straightforward. Short-run ETF performance always reflects several layers at once. Part of it may come from the index design. Part of it may simply reflect a window when growth names are being rewarded more generously than the rest of the market. If you have not separated those forces, it is easy to turn one good number into a false impression that the fund is somehow safer or easier than it really is.

An ETF is not a savings product with better packaging. It is still a stock exposure vehicle, only packaged through a rules-based basket. The rules are what define the risk.

Read the index before you read the story

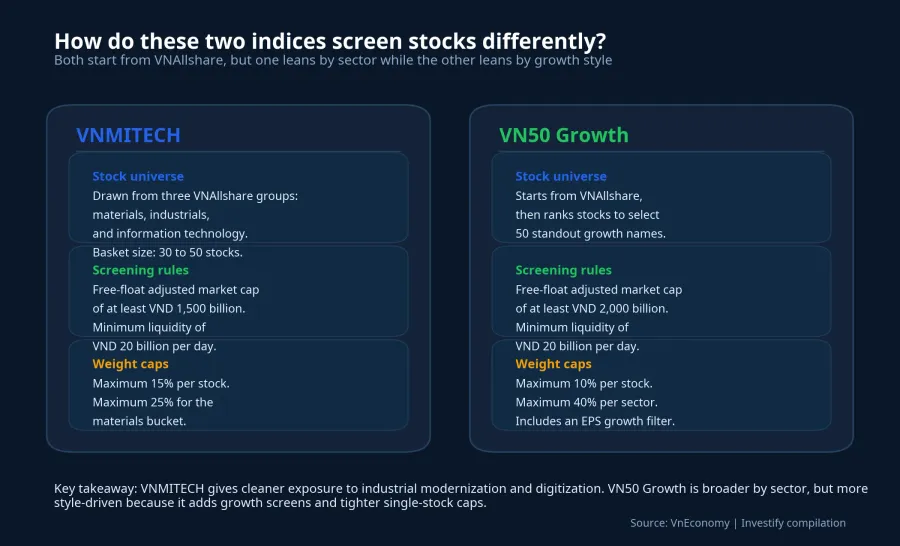

FUEMITEC tracks the VNMITECH index. According to VnEconomy, that index draws from three VNAllshare groups: materials, industrials, and information technology. It holds between 30 and 50 stocks, requires at least VND 1,500 billion in free-float adjusted market capitalization, requires at least VND 20 billion in matched trading value per day, and caps individual stock weight at 15% and the materials bucket at 25%.VnEconomy

That means the “technology” label can easily mislead a newcomer into expecting a narrow pure-tech basket. In practice, the exposure is broader. You are buying into a modernization theme that includes industrial production, materials, infrastructure, and digitization. If you think you are buying only a concentrated software-style story, your expectation is already off before the trade begins.

FUEVN50G tracks the VN50 Growth index. VnEconomy says that index selects 50 stocks from VNAllshare, requires at least VND 2,000 billion in free-float adjusted market capitalization, requires at least VND 20 billion in matched trading value per day, caps a single stock at 10%, and caps a sector at 40%.VnEconomy In plain English, this is not just a large-cap basket. It is a basket tilted toward companies that score better on growth characteristics.

That difference matters because it answers the most basic portfolio question: what exactly am I buying? VNMITECH gives cleaner exposure to three groups linked to industrial modernization. VN50 Growth is broader by sector, but more style-driven because it leans harder into growth filters. A sector tilt and a style tilt can both work in the same rally, yet they carry different risks once the market changes what it wants to pay for.

Because ETFs trade on exchange, NAV is only part of the picture

Many first-time investors hear the word “fund” and assume the experience will feel similar to an open-end fund. That is where confusion starts. In an open-end fund, the main reference point is usually NAV and the dealing cycle. An ETF trades intraday on the exchange like a stock, so investors face not only the fund’s NAV but also the market price available when the order is placed.

That affects real-world outcomes more than beginners often expect. A newly listed ETF may not have a deep order book right away. If the bid and ask side are still thin, even a modest order can move the execution price more than expected. At that point, the investor is not simply “buying a fund.” They are also dealing with liquidity, order-book depth, and the spread between bid and ask.

Put simply, NAV is the underlying net asset value per fund certificate, while the execution price is the market’s tradable price at that moment. Those numbers can be close, but they are not automatically identical. In the first weeks after listing, the more useful things to monitor are whether bid-ask spreads tighten, whether traded price tends to stay close to NAV, and whether matched volume becomes consistent enough for investors to enter and exit without friction.

This is why a thematic ETF is not always “easier than stocks.” It is true that you do not have to build the basket yourself one stock at a time. But in exchange, you need to understand the trading mechanics of the certificate itself. The simplicity is in the portfolio packaging, not in ignoring liquidity.

When a thematic ETF fits better than a broad ETF or an open-end fund

A thematic ETF usually fits investors who already have a clear view on a particular slice of the economy. Maybe they want more exposure to industrial modernization, digitization, or a cluster of companies the market is rewarding on growth metrics. In that case, the fund offers a rules-based basket instead of forcing the investor to assemble the position one ticker at a time.

If the goal is simply to move with the market, reduce sector concentration, and avoid dependence on one narrative, a broad-market ETF is often easier to understand. If the goal is to delegate stock selection to an active management team and accept NAV-based dealing instead of intraday trading, an open-end fund is the more natural fit.

The key point is that these products should not be treated as interchangeable just because one of them posted a better two-month number. They differ in basket construction, trading mechanics, and the type of risk the buyer accepts. Skip those layers, and a new investor is likely to carry the same expectation into thematic ETFs, broad ETFs, and open-end funds, then wonder why the real experience feels different.

Bottom line: worth watching, but not a shortcut

VinaCapital’s two new ETFs are a useful sign that Vietnam’s fund-certificate market is offering investors more ways to target specific themes without handpicking every stock.CafeF But the more important takeaway is not that the products are new. It is that a thematic ETF only becomes genuinely useful when the buyer understands where the basket is tilted and how that basket trades on the exchange.

For first-time investors, the best things to watch in the early weeks are not whether the fund feels fashionable or whether the label sounds exciting. The better checklist is more practical: which part of the market the index is actually selecting, whether the gap between traded price and NAV is narrowing, and whether liquidity on the screen is strong enough to support clean execution. Once those questions are answered, a decision on a newly listed ETF starts to rest on real ground.