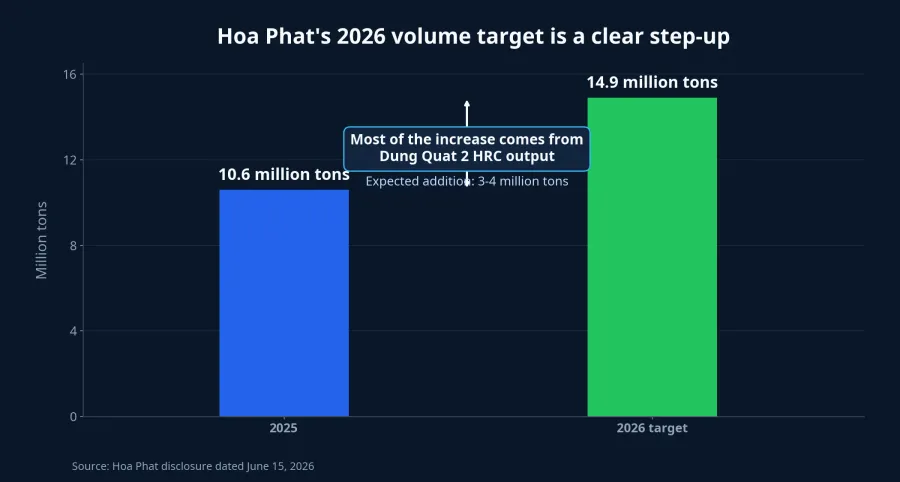

Hoa Phat's nearly 15 million ton steel target for 2026 is the kind of number that can dominate a headline. For HPG shareholders, though, this should not be read as a simple volume story. The important detail in the company's latest disclosure is that most of the incremental output is expected to come from HRC once Dung Quat 2 operates steadily, not from a broad-based expansion that automatically lifts every profit line.Hòa Phát

The headline numbers are straightforward. Hoa Phat is targeting nearly 14.9 million tons of steel output in 2026, roughly 40% above the prior year. In the same June 15 disclosure, the group said it sold 10.6 million tons in 2025, and that most of this year's increase should come from HRC produced at Dung Quat 2, with an expected contribution of about 3-4 million additional tons.Hòa Phát That alone changes how the story should be framed: the right question is no longer whether output is large, but whether HRC can be sold at the right price and with the right earnings quality.

A bigger number is not the conclusion

Newer investors often fall into a linear reading of industrial growth: capacity rises, revenue rises, profit follows. In steel, that logic usually misses half the picture. Shareholders are not paid on installed capacity or on nominal output. They are paid on margin structure, inventory discipline, and the company's ability to turn accounting earnings into actual cash.

That is why Hoa Phat's 2026 target needs to be read through the product mix. HRC is different from conventional construction steel because its downstream demand links into manufacturing chains such as machinery, autos, shipbuilding, oil and gas, steel structures, and energy. When Hoa Phat says the incremental volume will mainly come from HRC, it is signaling something more important than scale. It is pointing to a growth phase with a different economic profile from a cycle driven primarily by housing and civil construction demand.Hòa Phát

The company also says it is currently supplying roughly 1.2 million tons of steel products per month. In the same disclosure, management described construction steel demand as benefiting from recovering infrastructure, transport, housing, and nationwide building projects; in the first 5 months of the year, construction steel sales reached 2.3 million tons.Hòa Phát The point is that the demand base is broader than residential property alone. That matters because new capacity only becomes valuable when the market can absorb it.

HRC is the part that deserves a valuation premium

If there is one lens through which to read Hoa Phat in 2026, it is HRC. The reason is simple: this is the link between new capacity and earnings quality. A steelmaker can raise output by adding furnaces, stabilizing a new line, or running a plant harder. The valuation investors are willing to pay, however, depends much more on whether the product mix moves up the value chain.

Hoa Phat says anti-dumping duties on imported HRC from China and India apply only to products sold into the domestic market, while imported HRC used for export manufacturing is not subject to those duties. The company also says domestic HRC sales have already increased noticeably, helped both by trade-defense policy and by new supply from Dung Quat 2. Management expects to fill the group's 9 million ton annual HRC capacity within the next 1-2 years.Hòa Phát That is an important data point because it suggests the HRC story is not just about capacity addition. It is also about deepening Hoa Phat's position in the domestic industrial supply chain.

For a retail investor, the mechanism is easier to understand than it first appears. Construction steel is more visible because it tracks swings in housing and public works. HRC is harder to read, but it says more about whether the company is becoming structurally more relevant to manufacturing. If Hoa Phat can place more HRC with domestic downstream producers, it does not just become larger. It becomes less dependent on one of the most cyclical corners of the steel market.

That still does not mean HRC automatically equals higher profit. This is where analytical discipline matters. HRC only helps shareholders if the extra volume reaches the market at acceptable pricing, fixed costs are absorbed more efficiently, and inventories do not build faster than demand. Selling more tons at weak realized prices is not a quality growth story. It is just a larger operating footprint with thinner economics.

Margins have to be read together with raw materials

One encouraging feature of Hoa Phat's June 15 disclosure is that management still uses restrained language on profit. The group is targeting VND 210 trillion in revenue and VND 22 trillion in net profit for 2026, equivalent to a net margin of around 9-10%. That is close to the 2025 base rather than a dramatic jump.Hòa Phát The message is clear enough: Hoa Phat is pursuing scale growth, but it is not assuming margins will suddenly widen just because capacity is larger.

First-quarter results fit that logic. The company reported more than VND 53.3 trillion in revenue and VND 9.056 trillion in net profit, equivalent to 41% of the full-year profit plan.Hòa Phát That is strong enough to support the case for 2026, but it should not be read as proof that the rest of the year will move in a straight line. For an integrated steel producer, the market variable always comes back to the spread between selling prices and input costs.

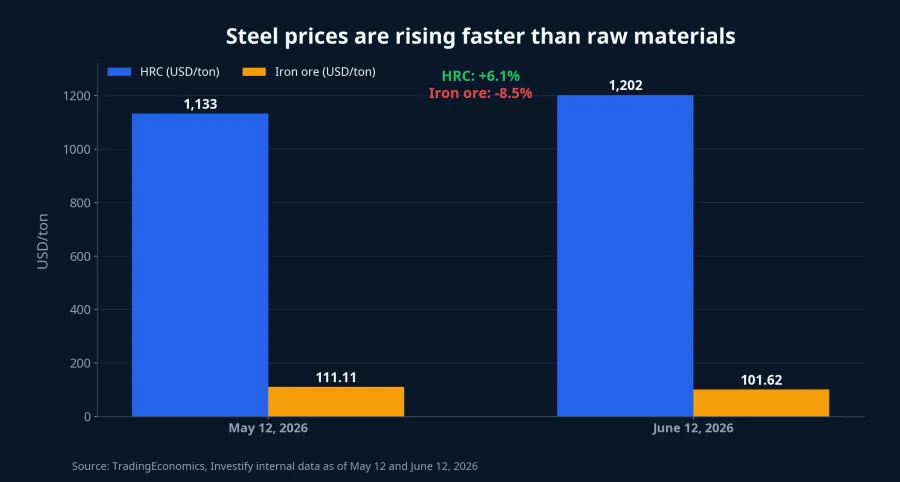

Investify's internal data as of June 12 shows HRC prices rising from USD 1,133 per ton to USD 1,202 per ton over one month, while iron ore fell from USD 111.11 per ton to USD 101.62 per ton. Over the same period, coking coal edged up from USD 238 per ton to USD 244 per ton. On balance, that mix tilts more positive than negative for margins because the main selling price is improving faster than the key raw material input.TradingEconomicsTradingEconomicsTradingEconomics

Still, this is only a near-term snapshot of the margin setup. Hoa Phat's earnings do not depend on one pair of HRC and iron ore prices alone. They also depend on how efficiently Dung Quat 2 ramps, what financing costs look like after a large investment cycle, how stable domestic sell-through remains, and whether operating cash flow keeps pace with accounting profit. In other words, commodity data is opening a favorable window, but the company still has to execute through it.

What HPG shareholders should actually watch

For HPG, 2026 should be read as a quality-upgrade test rather than a pure expansion test. The thesis is straightforward: the nearly 15 million ton target only matters for shareholders if the incremental HRC output turns into revenue with defendable margins and clean cash generation. If that happens, Hoa Phat takes another step from being Vietnam's dominant construction-steel name toward becoming a deeper industrial steel platform.

From here to year-end, three signals matter most. First is actual HRC sell-through, especially in the domestic market. Second is the spread between HRC prices and major inputs such as iron ore and coking coal, because that is where margin math is decided. Third is the relationship between net profit and operating cash flow, because that is the clearest test of whether new capacity is creating real cash rather than just larger reported earnings.

The current setup gives Hoa Phat more support than it had a year ago: domestic demand looks broader, new supply is more tangible, and selling prices are moving in a friendlier direction than raw materials. But the investment conclusion should stay disciplined. What will define HPG in 2026 is not how many tons of steel the company can produce, but how many tons of HRC it can sell at margins strong enough to turn new scale into better earnings quality.