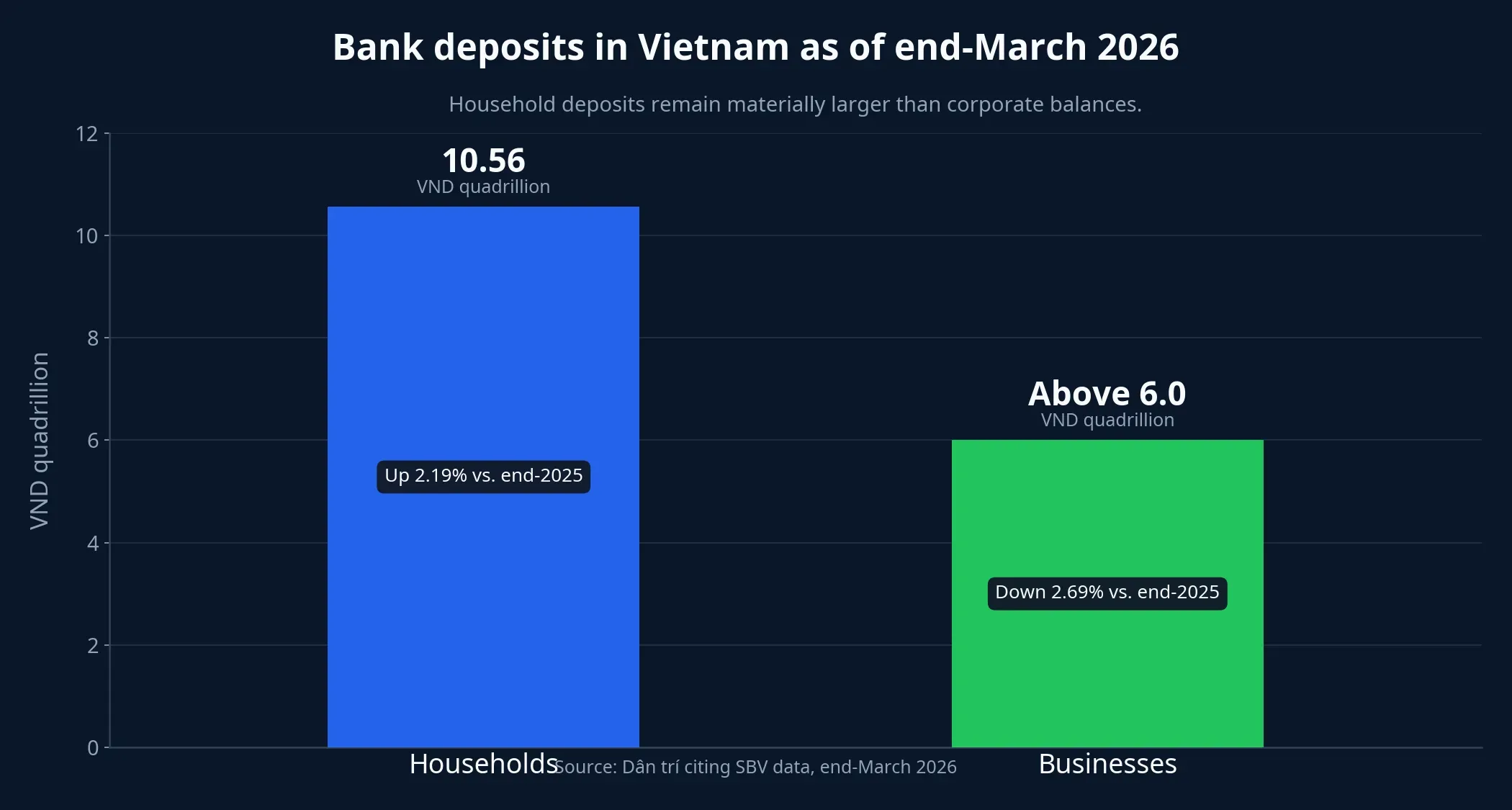

Household deposits in Vietnam’s banking system climbed above VND 10.56 quadrillion at the end of March 2026, up 2.19% from the end of last year, while deposits from businesses and economic organizations slipped to just above VND 6 quadrillion, down 2.69%. Total means of payment, excluding valuable papers, stood above VND 19.6 quadrillion.Dân trí

It is tempting to read those numbers as a simple risk-off signal from retail investors. That reading is not wrong, but it misses the deeper point. For many households, keeping money in a term deposit right now is less about chasing yield and more about preserving the option to wait while other assets still feel noisy, demanding and psychologically expensive.

That matters most for first-time investors. The hardest part is rarely the math alone. It is the daily pressure of watching prices move, tracking headlines and wondering whether every decision is being made at the wrong time. A bank deposit does not promise a fast path to wealth, but it does remove the burden of having to act under stress.

What the deposit record really says about household behavior

The easiest way to think about it is this: businesses and households use idle cash for different jobs. Companies need liquidity for inventory, payables, payroll and expansion plans. Households are more likely to treat cash as accumulated savings, emergency liquidity or future buying power waiting for a clearer moment.

That is why falling corporate deposits and rising household deposits are not contradictory. They show that banks remain the default storage place for family savings even as the menu of alternatives has grown, from online stock trading to gold, mutual funds and ETFs.

More importantly, the VND 10.56 quadrillion milestone should not be framed as a vote against investing. It works better as a gauge of risk tolerance. When the payoff in other assets is still uncertain, savers prefer to wait rather than reallocate capital too quickly.

Rates are not especially high, but they are easy to understand

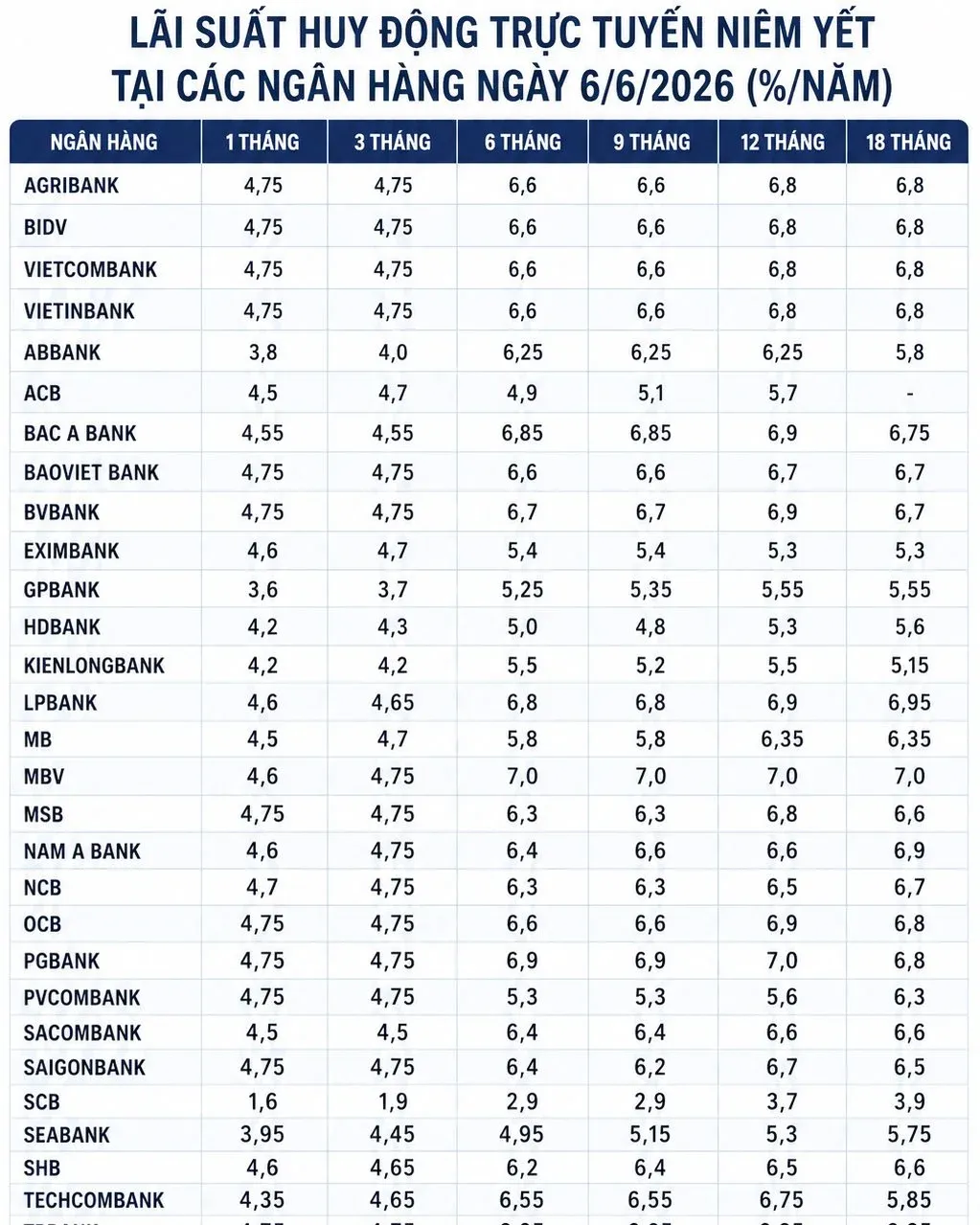

A common assumption is that people only save aggressively when deposit rates are very high. In reality, deposits can keep rising even when rates are nowhere near the stress levels seen in earlier tightening cycles. In March, Dân trí counted 20 banks that raised deposit rates, and annual yields of 7% on 12-month tenors were no longer unusual.Dân trí

By June 9, VietnamNet reported that BIDV’s online deposit rates were 6.6% a year for six to 11 months and 6.8% for 12 to 36 months. Over-the-counter deposits at BIDV were listed at 5.9% for 12 to 18 months and 6.0% for 24 to 36 months.VietnamNet

Those returns are not exciting in the way a rally in stocks or gold can be exciting. Their strength is that they are legible. Put money in for 12 months, know the maturity date, know the return, and avoid having to time an entry or explain a sharp drawdown a week later.

That is the part other assets still struggle to replace immediately. Stocks may offer higher long-term upside, mutual funds reduce the workload of picking names, and gold can move sharply in the right direction. But all three ask investors to absorb volatility first and trust that the reward will follow. For people not ready for that trade-off, a moderate but predictable rate is still easier to live with.

Why stocks have not yet pulled defensive money out of banks

The equity market is not short of opportunities. What savers need, however, is not just opportunity. They need the sense that the opportunity is broad, durable and does not require constant reaction. Recent market action still falls short on that test.

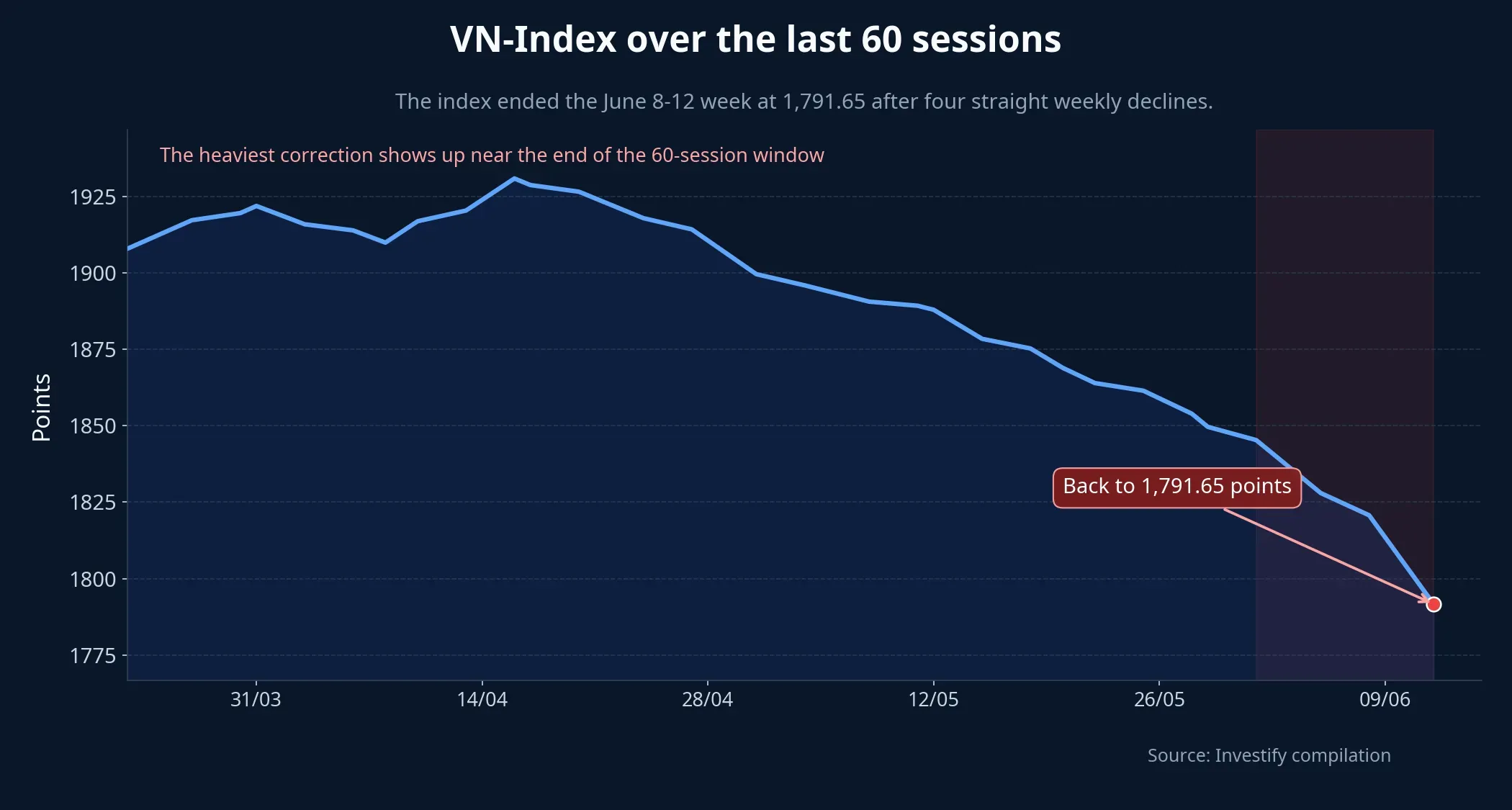

For the June 8-12 week, VN-Index closed at 1,791.65 points, down 2.57% from the previous week and marking a fourth consecutive weekly decline. Trading volume on HoSE was more than 2.92 billion shares, down 4.6%, while trading value was about VND 79,211 billion, down 13.2%.Kinh tế Tài chính

That data does not prove equities are unattractive over the long run. It says something narrower: the market has not yet sent a strong enough signal for idle household cash to abandon a defensive posture. A rebound concentrated in a few large caps is usually less persuasive than an advance backed by broader participation and improving liquidity.

For newer investors, volatility is also a psychological tax. Every red session brings more than a mark-to-market loss. It raises questions about whether to cut, average down or rethink the entire allocation. When the money sitting in a bank account does not create the same emotional demand, many households choose certainty over the possibility of higher returns.

Gold and funds are still being watched, not fully replacing deposits

Gold tells a similar story. On the morning of June 14, SJC gold bars were quoted around VND 144-147 million per tael. CafeF reported that the price was VND 2.2 million lower than the previous weekend on the buy side and VND 3.2 million lower on the sell side.CafeF

For savers used to fixed deposits, that kind of move is large enough to keep gold in the category of “watch for opportunities” rather than “replace idle cash entirely.” Buying gold means accepting that prices can shift hard over just a few days. That is very different from a deposit where the outcome is known at the start if the money stays to maturity.

Mutual funds and ETFs sit between those two extremes. They are friendlier than picking individual stocks, but they are still exposed to the underlying market. Put simply, a fund reduces the work; it does not eliminate market risk. That is why bank money tends to move into funds more decisively only when expected returns clearly exceed savings rates and investors believe the longer holding period is worth the short-term swings.

A bank deposit is really the right to wait

This is the most useful way to understand the VND 10.56 quadrillion figure. Deposits do not need to outperform every other asset to keep attracting money. They only need to preserve one practical advantage: they buy time without forcing households to pay for that time through daily anxiety.

Seen from that angle, saving is not passive at all. It is an intentional waiting position. Depositors are not saying they will never buy stocks, never buy gold and never allocate to funds. They are saying the reward in those assets is not yet clear enough to justify the volatility, attention and decision pressure.

That is why the persistence of household deposits says more about the emotional state of family money than about the absolute attractiveness of rates. As long as retail investors find markets hard to read, risks hard to size and allocation choices hard to own, bank balances still have a strong reason to stay where they are.

What would make that money start moving

The first trigger is a narrower real return on deposits. Data relayed by Vietstock from the General Statistics Office showed average CPI in the first five months of 2026 up 4.31% year on year, while core inflation rose 4.04%.Vietstock If inflation rises further while deposit rates stay flat or decline, savers will start asking whether bank yields still protect purchasing power.

The second trigger is an equity rebound supported by liquidity rather than a few brief relief sessions. Once the market shows that buyers are returning across sectors, the fear of volatility starts to weaken. That is when some of the money currently parked in banks gets a reason to move into risk assets.

The third trigger is simplicity. Funds, ETFs and even gold attract defensive capital more effectively when first-time investors feel the product is understandable, the risks are visible and the monitoring burden is manageable.

The cleanest thesis today is that household money has not left banks because the reward elsewhere is still not clear enough or durable enough. That does not deny the existence of opportunity in stocks, gold or funds. It says retail investors are still prioritizing clarity and the ability to delay a decision. The key signals to watch over the next few weeks are inflation, stock-market liquidity and how well alternative products are explained to newer investors.