FDI is rising, but that is not a universal ticket for every industrial park stock. In simple terms, foreign capital flows tell you something about the economy, while stock prices tell you something about individual businesses. The two stories overlap, but they never line up perfectly.

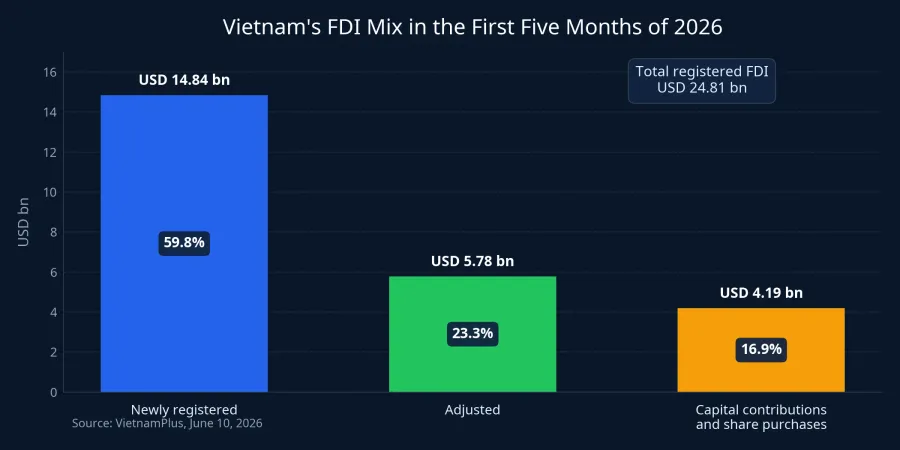

As of May 31, Vietnam's registered FDI had reached USD 24.81 billion, up 34.9% year on year, while disbursed FDI came in at USD 9.75 billion, up 9.6%. If you stop there, it is easy to assume industrial park names should be the first winners. That reading is only half complete. Investors still need to ask where the capital is going and which listed companies actually have something to sell into that wave.VietnamPlus

FDI is not one pool of money

One common mistake is treating FDI as a single number. In reality, the first five months of 2026 were made up of three different buckets: USD 14.84 billion in new registrations, USD 5.78 billion in adjusted capital and USD 4.19 billion in capital contributions and share purchases.VietnamPlus

Think of them as three different speeds of impact. Newly registered capital points to fresh projects. Adjusted capital tells you existing investors are still expanding. Capital contributions and share purchases are the most misleading bucket, because they can energize the market without creating immediate revenue in the next quarter.

Fresh capital is still leaning toward production

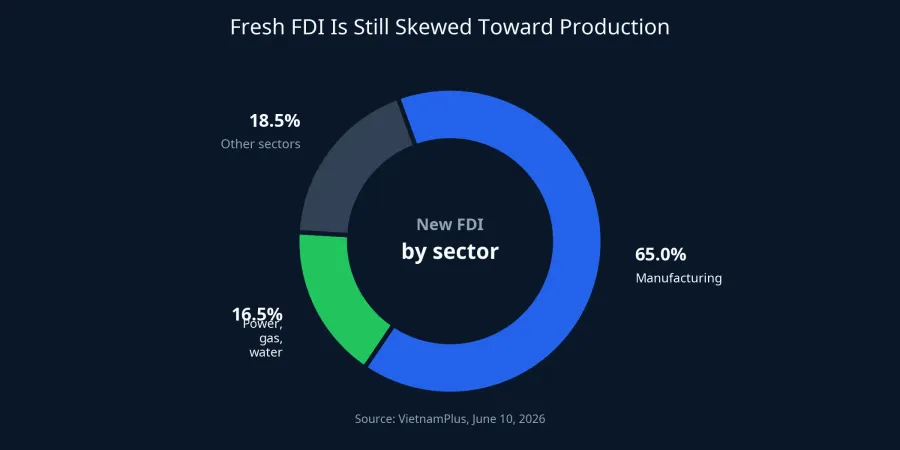

Within newly registered FDI, manufacturing accounted for 65.0%, while electricity, gas and water made up 16.5%. That tells investors something important: fresh foreign capital is still prioritizing productive capacity, not just land stories or asset narratives.VietnamPlus

When a manufacturer chooses Vietnam, land is only one part of the checklist. The investor also needs stable power, logistics access and enough operational readiness to start on time. That is why industrial parks come up first in this discussion. But coming up first is not the same as saying every industrial park ticker should move the same way.

More recent data from VietnamFinance adds another layer. Industrial production rose 8.7% in the first five months, while manufacturing grew nearly 9.5%. That supports the idea that FDI is moving alongside real production expansion, not just headline registrations on paper.VietnamFinance

Why industrial park stocks do not move in lockstep

This is where many first-time investors get tripped up. The statement that "rising FDI benefits industrial parks" is directionally true. Jumping from that to "every industrial park stock deserves attention" is where the logic starts to slip.

The first reason is that clean, lease-ready land is not evenly distributed. Some developers still have large plots that can be leased now. Others may have land on paper but still face legal or infrastructure work before they can monetize it.

The second reason is revenue timing. A project may be announced today, but the path from site selection to paperwork, land lease, construction and actual revenue recognition can take multiple quarters.

The third reason is financial structure. Two companies can both own industrial land, yet the one carrying more debt or slower project preparation may convert the FDI tailwind into profit much later than a peer with ready-to-lease assets.

One macro story does not create one price path

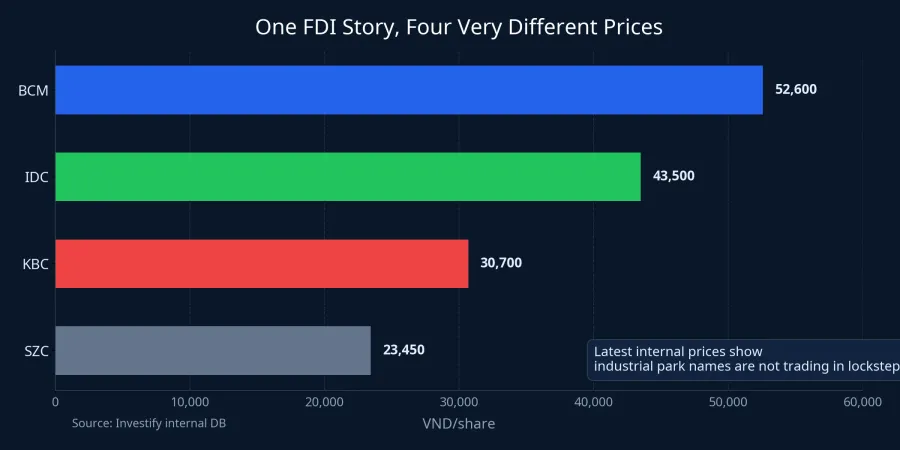

Investify's latest internal prices make that point clearly enough: BCM closed at VND 52,600 per share, IDC at VND 43,500, KBC at VND 30,700 and SZC at VND 23,450. All four are tied to the same broad FDI narrative, yet the market is still pricing them as four very different businesses.

Those prices do not tell you which stock is cheap or expensive by themselves. What they do show is that the market is separating names by land quality, location, revenue visibility and company-specific expectations.

Not every project on the map becomes revenue quickly

Even if the FDI backdrop remains supportive, the industrial land story is still not a straight line from project news to profit. On June 13, VietnamBiz reported that WHA had proposed a 400-hectare industrial park project in the former Da Nang area. That is meaningful as a sign of expansion intent, but it is still only at the proposal stage, not at the stage of booked lease income.VietnamBiz

That example matters because investors often collapse several stages into one. A proposal, an approval, completed infrastructure and signed leases are four different milestones.

Power and logistics usually benefit later

FDI flowing into manufacturing does not only matter for industrial parks. Power and logistics also stand to gain, but usually later in the chain because they need factories to be operating, cargo to be moving and actual throughput to materialize.

For power companies, the key question is what industries are arriving, how much electricity they will consume and whether the dispatch framework favors the listed utility in question. For logistics, the test is whether the goods actually pass through that port, warehouse or transport network.

A practical reading framework for new investors

If you want to read an FDI headline in a more useful way, start with three steps.

First, separate the type of capital. New registrations tend to be most directly linked to industrial land and early infrastructure. Adjusted capital says more about whether existing investors are still expanding. Capital contributions and share purchases require a closer look to see whether money is actually entering the business or merely changing ownership.

Second, focus on assets that can be monetized soon. For industrial park developers, that means clean land, location, infrastructure readiness and the ability to sign contracts in the near term. For power and logistics, it means real throughput and real customers.

Third, return to the financial statements. News opens a line of inquiry, but only revenue, cash flow and profit confirm whether a company has already begun turning the FDI wave into operating results.

The core takeaway is straightforward: rising FDI is a constructive backdrop for industrial parks and the broader manufacturing chain. But in the stock market, the real benefit does not sit inside the word FDI itself. It sits with companies that already have the right assets, clean enough legal groundwork and close enough revenue visibility to convert that optimism into income. Over the next few weeks, the signals worth watching are not which headline sounds most bullish on FDI, but which businesses start translating that story into contracts and reported numbers.