Vietnam's textile industry is entering a phase that can easily look better than it really is. Orders have returned at many companies, export turnover is still growing, and factories are no longer under the same pressure to fill idle capacity. But for equity investors, fewer empty order books do not automatically mean an easier earnings cycle.

The bottleneck has simply changed. Earlier, the industry was struggling to keep production lines busy and workers employed. In the second half of 2026, the harder question is whether those orders are good enough to preserve margins while raw materials, freight, labor and compliance costs continue to rise.

The headline numbers are improving, but not by much

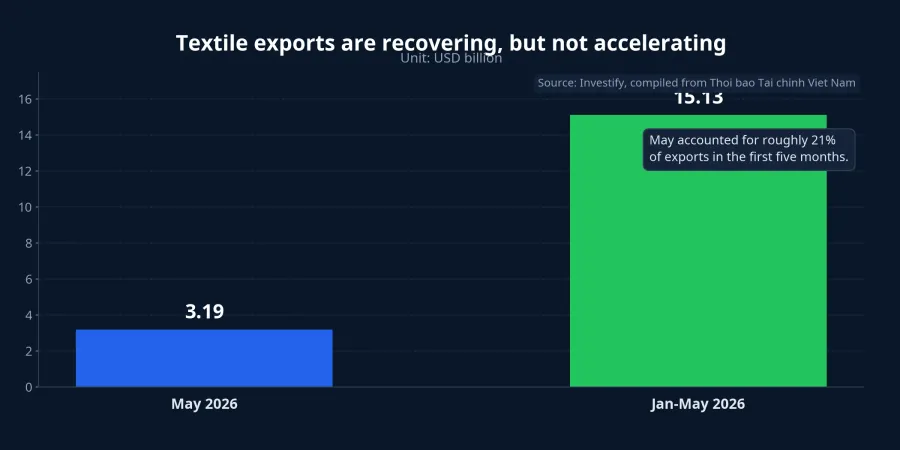

At first glance, the recovery is real. Citing Vietnam Customs data, Thời báo Tài chính Việt Nam reported that textile and garment exports reached about USD 3.19 billion in May 2026, up 3.5% year on year. Cumulative exports for the first five months stood at more than USD 15.13 billion, up 0.4%, while yarn exports were a relative bright spot at nearly USD 1.89 billion, up 8.7% from a year earlier.Thời báo TCVN

That is enough to say the industry has moved beyond outright contraction. It is not enough to say it has entered a strong expansion phase. A 0.4% increase over five months is still a thin growth cushion, and thin growth leaves very little room for rising costs before earnings start to feel pressure again.

That pressure becomes clearer once the annual target is placed next to the current run rate. According to the same report, the industry still needs another USD 30.2-31.2 billion in the remaining seven months of 2026 to hit its full-year export target of USD 48-49 billion. That implies an average of USD 4.3-4.5 billion per month, materially above the May pace if we focus only on garments.Thời báo TCVN

For investors, that means the right question is not simply whether exports are rising. It is whether the pace is strong enough, where the growth is showing up, and whether that growth can offset the cost inflation now moving through the supply chain. That distinction separates a revenue story from an earnings story.

Orders have returned, but order quality matters more

VITAS says most textile and garment companies already have orders booked through Q3 2026, with some larger firms seeing further out. That is a meaningful improvement from the earlier period when factories were mainly worried about finding work. But VITAS is also explicit that the core challenge is no longer order volume. It is order quality and profitability.Thời báo TCVN

This is where newer investors often stop too early. A factory can be busy without becoming more profitable. If selling prices stay low, delivery windows get tighter, technical requirements rise, and buyers demand more on environmental, social and governance standards, companies may end up working harder while keeping less profit from each order.Thời báo TCVN

That helps explain why a shared backdrop of returning orders can still produce very different outcomes. Companies with deeper control over materials, production planning and order management, or those moving further into FOB and ODM, have a better chance of defending gross margin. Firms still concentrated in low-priced work or heavily exposed to volatile input costs can end up squeezed at both ends: customers resist higher prices while costs keep climbing.Thời báo TCVN

VietnamPlus shows how that squeeze plays out in real operations. Industry representatives said that from July 2026 onward, orders have shown clearer signs of thinning as importers wait for more clarity on actual tariff levels before committing. At the same time, if companies have to switch to air freight to meet delivery schedules, transport costs can rise to USD 4-5 per kilogram, far above processing fees of just over USD 2 per product.VietnamPlus

In practical terms, textile companies do not just need orders right now. They need orders with decent pricing, manageable lead times and a logistics chain smooth enough to keep revenue from turning into a low-quality rush for volume. That is the layer investors should be watching.

One industry, very different margin stories

The divergence is already visible in Q1 2026 results. Vietnam National Textile and Garment Group posted revenue of roughly VND 4,490 billion, up 5% year on year, while an improved gross margin helped lift profit by more than 12%. Phong Phú also showed a healthier profile: revenue rose 5.1% to VND 624.6 billion, gross margin improved to 20.5%, and net profit increased 16.8% to VND 132.3 billion.Thời báo TCVN

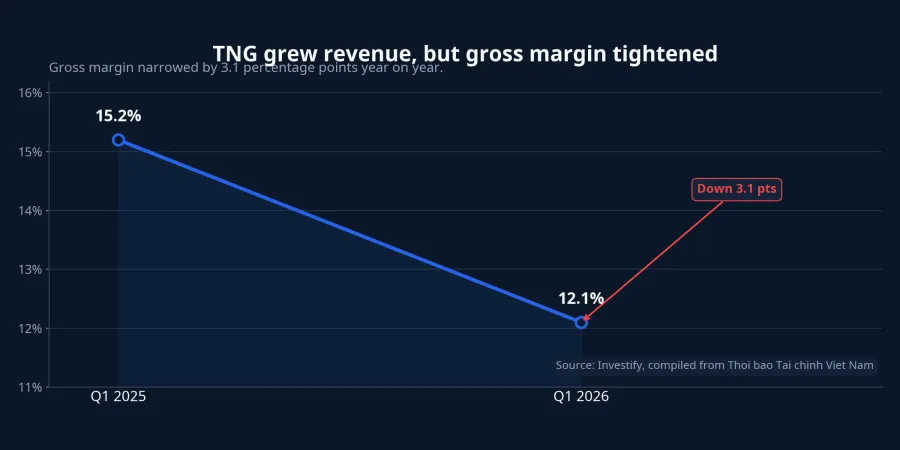

TNG tells a more cautionary story. Q1 2026 revenue jumped 29.2% to nearly VND 1,952 billion, but gross margin fell from 15.2% to 12.1%. Selling expenses rose 46.4%, pressuring operating profit, while net profit still increased 39.3% to VND 60.3 billion mainly because of a one-off gain booked during the quarter.Thời báo TCVN

That is the detail worth remembering. Revenue is usually the first number that grabs attention because it looks like momentum. But if gross margin is narrowing and logistics or selling costs are rising faster, stronger sales do not necessarily convert into durable profit or stronger cash generation.

Century Synthetic Fiber shows the other side of the same cycle. Its Q1 revenue fell nearly 29% year on year and the company posted a net loss of more than VND 34 billion.Thời báo TCVN In other words, some businesses have already moved past the worst, some are preserving profitability better than peers, and some are still stuck in the most cost-sensitive parts of the chain. Treating the sector as a single block is likely to produce the wrong conclusion.

Tariffs are still a variable, not a finished outcome

Another risk that needs careful framing is US tariff policy. USTR has published its findings and proposed actions under Section 301 on trade in goods tied to forced labor, set July 6, 2026 as the deadline for public comments, and scheduled a public hearing for July 7, 2026. That means the process is still at the proposal and consultation stage, not at the point of an effective tariff regime.USTR

According to Thời báo Tài chính Việt Nam, the proposed additional tariff rates are 10% or 12.5%, with Vietnam placed in the 12.5% group. The same report notes a textile-specific mechanism under which a certain volume of textile products could enter the US at lower tariff rates depending on their use of cotton, man-made fiber and cotton products imported from the US.Thời báo TCVN So this is not yet a locked-in legal shock. It is a policy variable that still needs to be tracked through the formal process.

The more immediate risk may not even be the final tariff number. It may be buyer behavior while everyone waits. When importers pause to see how policy settles, a Q4 order gap can show up before any new tariff officially takes effect. That is why tariffs affect textile exporters not only through legal text, but also through customer hesitation, delivery scheduling and the extra freight costs that come with tighter timelines.VietnamPlus

What newer investors should watch

The core thesis is straightforward: Vietnam's textile industry has moved beyond the worst of its order shortage, but the second half of 2026 still cannot be read through export turnover or revenue growth alone. The more useful lens is which companies can turn those orders into stable margins, and which ones are simply running faster to defend top-line numbers.

There are three signals worth tracking over the next few months. First is order visibility: coverage through Q3 is constructive, but the shape of Q4 demand is the next real test. Second is gross margin: if revenue grows while margins keep shrinking, the earnings story is still fragile. Third is the combination of freight costs and the US tariff process: even a modest delay in customer commitments or a need for faster delivery can bring margin pressure back quickly.Thời báo TCVNVietnamPlusUSTR

If the entire setup has to be reduced to one line, it is this: the textile story is no longer about whether orders exist. It is about which companies are still able to convert those orders into sturdier profits while costs and policy remain in flux.