When the World Bank cut its global growth forecast to 2.5% for 2026, the most useful takeaway for Vietnamese investors was not that they should suddenly turn bearish. The more practical question is how that risk travels before it reaches Vietnam's trading screen. For newer investors, this is where it helps to separate a relief rally in the US from a signal that is strong enough to make the local session look safe by default.World Bank

Two headlines are sitting next to each other, but they belong to different time frames. One is a full-year macro call in which the World Bank says the Middle East conflict has pushed energy prices higher, revived inflation, and hardened expectations for monetary policy.World Bank The other is a short-term rebound in Wall Street after geopolitical fears eased, with the Dow up 1.9%, the S&P 500 up 1.8%, and the Nasdaq up 2.5%.New York Post

Put simply, the US market is reacting to one shock cooling off for the moment, while the World Bank is describing the bill the global economy may still have to pay over the next few quarters. That is why “Wall Street is green” is not enough on its own. A better framework before the open is to read the signals in order: has oil really cooled, is FX still stable, and only then are cyclical stocks getting real confirmation from money flow.

Oil is still the first signal to read

The World Bank did not lower its forecast for an abstract reason. The core message is that the Middle East shock has lifted energy prices, making inflation and funding costs harder to bring down as quickly as markets had hoped.World Bank The Guardian, citing the same report, said global inflation could reach 4% in 2026, up from 3.3% in 2025. It also noted that average fertilizer prices could jump another 38% if supply through the Gulf is disrupted.The Guardian

In Vietnam, oil is not just an oil-and-gas equity story. Higher crude prices feed directly into freight costs, input costs for plastics and chemicals, and later into margins for consumer businesses. They also shape inflation expectations and how the market prices short-term risk.

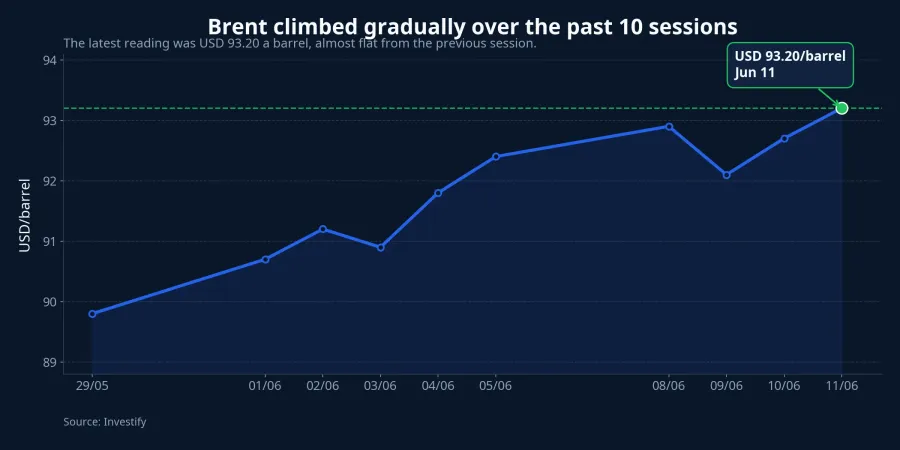

Internal data show Brent at USD 93.20 a barrel on June 11, almost flat from the previous session with only a 0.11% gain. That is not enough to say the energy risk has disappeared. But it does suggest the market is not being asked to absorb a fresh oil shock right before the open, and that is a meaningful distinction.

For newer investors, the reading is practical. If oil keeps easing after a sharp run-up, businesses exposed to input costs get some breathing room. If oil turns higher again, part of Wall Street's optimism gets discounted on the way into Vietnam because the inflation and cost story moves back to the front of the line.

FX decides how much of that optimism can travel into Vietnam

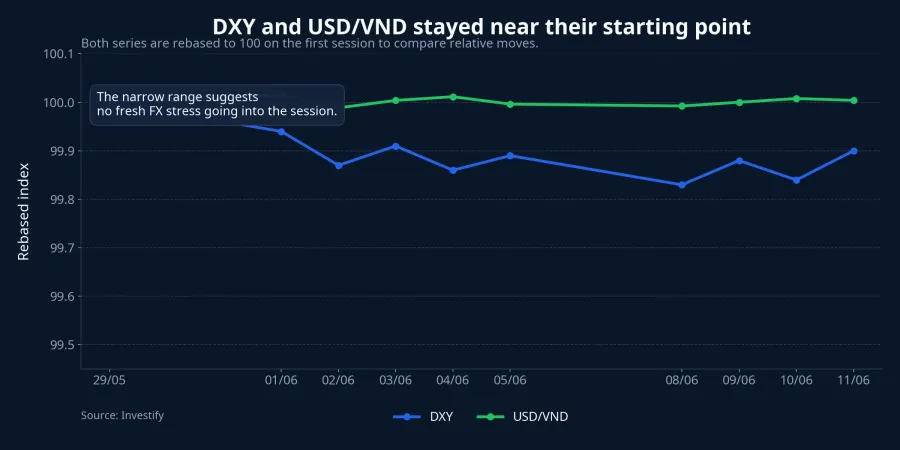

After oil, the next signal is the US dollar and USD/VND. These variables are less dramatic than a spike in Brent or a rally in the Nasdaq, but they often determine whether global relief lands softly or harshly in Vietnam. A stronger US market that comes with a stronger dollar does not automatically translate into comfort for risk assets in emerging markets.

Internal data put DXY at 99.92 on June 11, down 0.05%. USD/VND was VND 26,316 per dollar, down 0.03%. On their own, those are small moves. Together, they suggest no fresh FX pressure has built at the very moment the market needs stability to digest the global backdrop.

The simple version is this: Wall Street's bounce is a sentiment signal, while FX is the reality check. If that reality check remains calm, domestic money has a better chance of reacting with less defensiveness to overseas news. If USD/VND tightens again, many sectors will still be discounted, especially companies exposed to funding costs or foreign-currency obligations.

That does not mean a stable exchange rate guarantees a stronger market. FX only removes one layer of pressure. The market still needs liquidity, breadth, and a clear leadership group. But ignoring FX is one of the easiest ways for a new investor to mistake a green US session for a universal all-clear.

Cyclical stocks should be read only after the first two filters

When global growth is marked down, cyclical sectors usually respond the most clearly. That can mean steel, chemicals, industrial parks, transport, non-essential retail, or brokerages. Still, these should be the last step in the reading process, not the first, because their price action reflects earnings expectations after the market has already passed through the two input filters of commodities and FX.

If oil is stable and USD/VND is stable, cyclical stocks have a firmer basis for following global risk sentiment. But a single cause should not be assumed too quickly. A steel stock rising early in the session may reflect a general risk-on mood, technical bargain hunting, or just a delayed reaction after a weaker prior session. Without confirmation from liquidity and market breadth, it is too early to declare that larger capital is rotating back in.

That is why the 1,800 level on the VN-Index still matters. The index closed the previous session at 1,798.61, still below that psychological threshold. A market that has just slipped under a round number does not only need better headlines from abroad. It also needs a leadership group strong enough to make the rebound feel durable instead of looking like an opening burst that fades later in the day.

For newer investors, this is the difference between reading signals and chasing price. Reading signals means asking whether oil, FX, and market breadth are all supporting the same rebound. Chasing price means seeing a handful of stocks jump early and assuming the entire risk picture has already cleared.

The World Bank report works better as a risk map

The value of the World Bank report is that it ranks what deserves attention first. In the current setup, that order is still oil first, FX second, and only then the reaction in cyclical stocks.

That also fits the broader warning in the report. The Guardian said global growth could fall as low as 1.3% in a worse scenario. It also noted that government debt in developing economies has risen from 40% of GDP to 70% of GDP since 2010, leaving those economies with less room to absorb shocks.The Guardian In other words, one strong US session does not erase the structural risk still sitting underneath the global economy.

That leads to a clear thesis. Wall Street's rebound is worth noting, but it is not a green light for Vietnam on its own. For a higher-quality rebound, the market still needs two supporting conditions: oil must avoid reheating, and USD/VND must avoid taking on new pressure. Only after that does it make sense to ask whether cyclical sectors are being confirmed by liquidity.

The watch list for the next one or two sessions should stay on that same axis. First, does Brent continue to trade flat or cool further. Second, do DXY and USD/VND remain in a narrow range. Third, can the VN-Index reclaim 1,800 with a rise backed by clear sector leadership. If those three pieces do not appear together, caution remains a more defensible reading than default optimism.