A USD 75 billion IPO naturally pulls your eyes to size first. But with SpaceX, the most useful part of the story is not the deal size or the roughly USD 1.77 trillion valuation. The more practical question is where the company is actually making money, where it is still burning capital, and which part of the narrative is mature enough to stand on current economics rather than future ambition.MarketWatch

Put simply, investors buying SpaceX today are not just buying rockets. They are buying three different layers at once. The first is Starlink, the satellite connectivity business with subscribers and revenue. The second is launch, the segment that anchors SpaceX's technology edge and brand. The third is artificial intelligence, the piece that can stretch the valuation story much further but is also consuming the most capital.Fidelity

Not everyone buying SpaceX is buying the same thing

According to the IPO prospectus, SpaceX is offering 555,555,555 Class A shares at an expected price of USD 135 per share. That takes the deal size to roughly USD 75 billion and pushes the implied valuation to about USD 1.77 trillion, above most already-listed U.S. technology companies.FidelityMarketWatch

That headline number matters, but it does not answer whether the valuation is easy to support. For newer investors, a better framework is to break the company into economic layers. Once you do that, the picture becomes much cleaner: the most proven profit engine is not launch, but Starlink within the connectivity segment. By contrast, the piece that can justify even more upside in the story is AI, yet that is also the area demanding the heaviest spending and offering the least evidence so far of matching returns.Fidelity

Starlink is the easiest part of the filing to underwrite

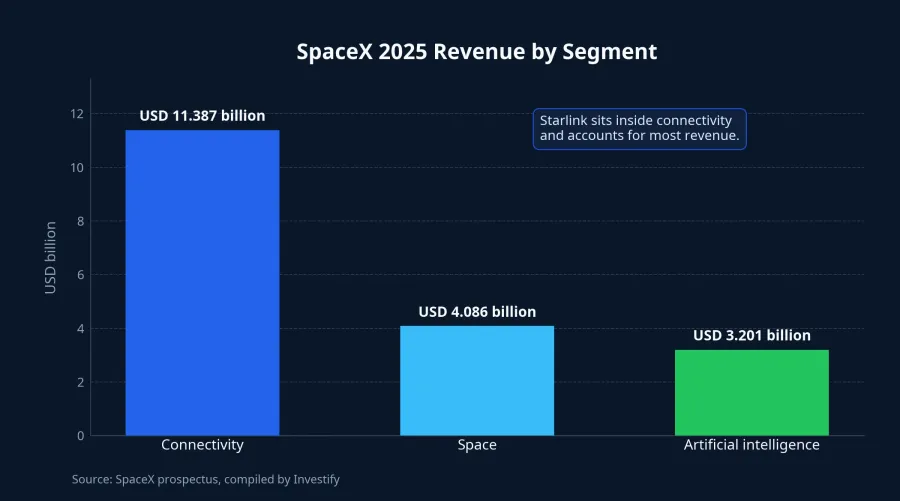

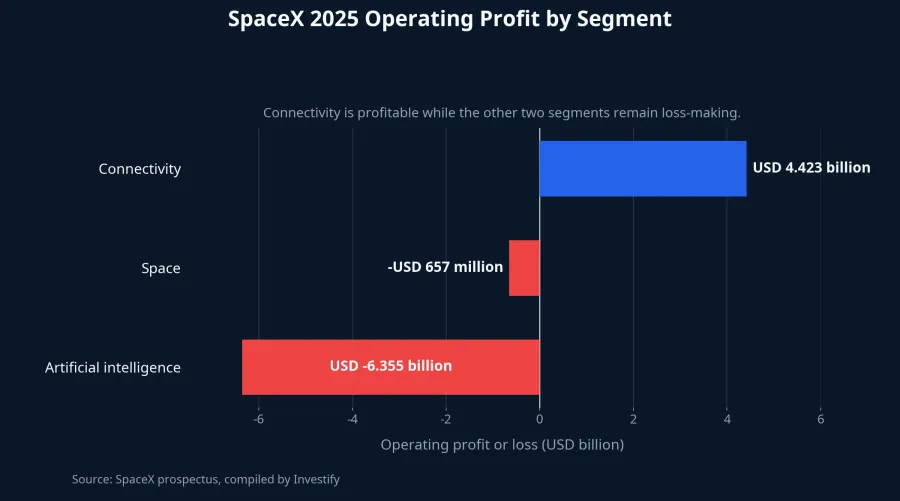

If you think of SpaceX as a three-story building, Starlink is the floor with the easiest foundation to inspect. As of March 31, 2026, Starlink had about 10.3 million subscribers across 164 countries, territories, and markets. In 2025, the connectivity segment generated USD 11.387 billion in revenue, USD 4.423 billion in operating profit, and USD 7.168 billion in segment-adjusted EBITDA.Fidelity

That is the key point for first-time investors. Satellite internet may sound futuristic, but at its core Starlink is increasingly behaving like a global subscription network. As user numbers grow, the fixed cost of the satellite constellation can be spread across a broader paying base. That makes the business model much easier to analyze than newer technology bets that still depend primarily on distant expectations.

At the group level, SpaceX reported USD 18.674 billion in consolidated revenue in 2025. That means connectivity alone accounted for roughly 61% of total sales. In other words, while the market talks about SpaceX as a space company, investors still need to remember that the largest revenue pool today comes from a satellite internet service with real customers, real receipts, and real operating profit.Fidelity

Launch matters strategically, but it does not carry the valuation alone

None of that means the space segment is unimportant. Quite the opposite. Falcon, Dragon, Starship, and launch services are what built the company's identity. They also form a difficult-to-replicate strategic advantage because SpaceX can launch its own satellites instead of renting launch capacity from somebody else. For a business like Starlink, that is similar to owning the road as well as the trucks moving on it.

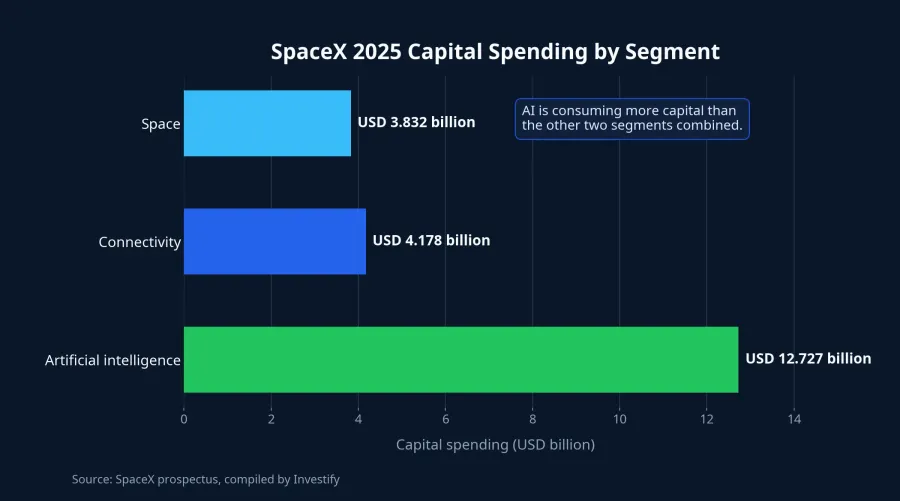

But when investors return to the financial statements, they find that launch is not the main segment explaining a USD 1.77 trillion valuation. In 2025, the space segment produced USD 4.086 billion in revenue but posted an operating loss of USD 657 million. During the same year, SpaceX also spent about USD 3.004 billion on Starship research and development. Those figures describe a strategically powerful segment that is still deep in investment mode.Fidelity

For newer investors, the plain-English takeaway is this: launch gives SpaceX long-term strategic leverage, but it is not yet the cash engine carrying the entire valuation. If you focus only on spectacular launches, it becomes easy to miss the less glamorous part of the business that is currently generating more revenue and profit.

AI stretches the story furthest and is the hardest piece to price

The hardest part of the IPO filing sits inside artificial intelligence. After consolidating xAI into its reporting, SpaceX showed USD 3.201 billion of AI revenue in 2025, but also an operating loss of USD 6.355 billion. Capital spending for that segment reached USD 12.727 billion, more than the combined capital spending of the space and connectivity businesses in the same year.Fidelity

This is where newer investors can get pulled into a brand and stop checking the profit structure underneath it. A company can be excellent in its core product, while the stock price reflects an additional premium for projects that still sit further out on the timeline. That premium is not automatically irrational. The issue is that once the valuation is already extremely high, the least proven cash-generating segment becomes the part most likely to challenge the story if market appetite for risk changes.

Discipline matters here as well. The filing clearly shows that AI is the biggest capital sink, but that alone does not prove the market is paying primarily for AI. The more careful reading is that Starlink is the most validated layer, launch is the strategic moat, and AI is the layer that could extend the valuation further while also holding the largest expectation risk.

Why huge demand does not automatically mean a stronger dollar

Another easy misunderstanding comes from the claim that global demand has already exceeded USD 250 billion. At first glance, that sounds like it should trigger a matching wave of dollar buying to fund the IPO. But MarketWatch notes that investors should not expect a standalone U.S. dollar frenzy from a single deal.MarketWatch

The reason sits in market plumbing, not just in the headline. Not every order turns into cash because allocations reduce what many buyers ultimately receive. Large institutions may already hold dollar liquidity. Others can fund purchases by selling existing U.S. assets or by using currency hedges before settlement. So demand for shares does not translate one-for-one into fresh demand for dollars.MarketWatch

Short-term market data also suggests a calmer picture. The DXY stood at 99.97 on June 10, rising just 0.02% in the session. USD/VND traded at VND 26,324.50 per dollar on the same day, down 0.06%. Those numbers do not prove the SpaceX IPO had no currency effect, but they do reinforce a basic point: exchange rates are still driven much more by interest rates, inflation, energy, and Fed expectations than by one blockbuster equity listing.

How first-time investors should break the story apart

If you read SpaceX through a risk-first lens, the sequence should run from what is already proven to what remains more speculative. Start with Starlink, because it already has subscribers, scale, and visible operating profit. Move next to launch, because that is the strategic backbone keeping the ecosystem integrated even though it still demands heavy investment. Only then should you move to AI, where the upside may be broad but the valuation risk is also the highest.

The clearest thesis from this IPO filing is that, at nearly USD 1.8 trillion, the most defensible part of SpaceX today sits in Starlink rather than in the glamour of launches or the promise of AI. The risk to watch is not whether the company has a strong enough brand. It is whether the most capital-hungry layer can eventually deliver returns large enough to justify the expectation premium already embedded in the price. The first few public quarters should answer that question much more clearly.