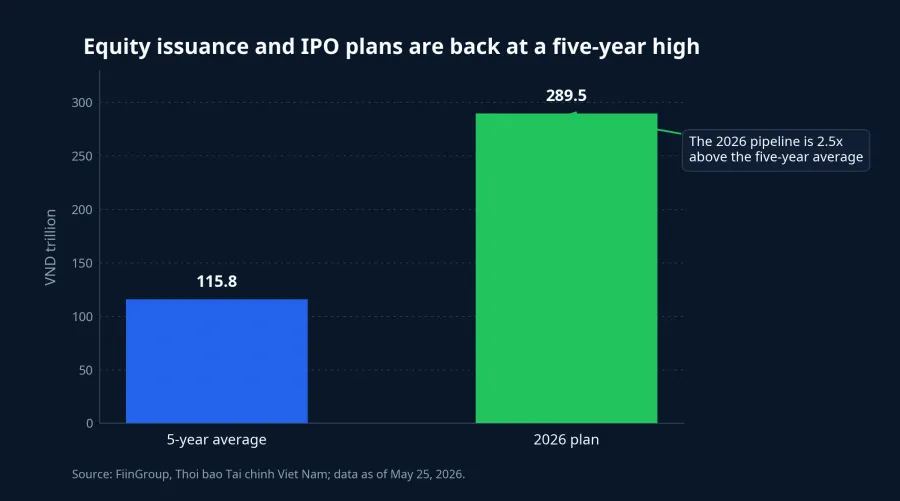

Vietnam's stock market is rediscovering one of its most basic functions: raising long-term capital for businesses through equity. As of May 25, 2026, listed and registered companies had lined up roughly VND 289.5 trillion of planned share issuance and IPO value, up 86.5% from 2025 and 2.5 times the five-year average.TBTCVN

That headline number can easily sound like a simple “risk-on” story. It is not. What matters more is where the money will go and whether existing shareholders will get enough incremental earnings in return for owning a smaller slice of the company after issuance.

The funding window is reopening, but under a different logic

The natural comparison point is 2021, when buoyant liquidity and rising prices made equity fundraising much easier. FiinGroup data, as cited by Thoi bao Tai chinh Viet Nam, shows that the 2026 pipeline has already returned to the highest level seen since that earlier boom.TBTCVN

The difference now is that investors are no longer rewarding every growth story on faith. After the volatility of 2022-2025, the market has become more selective about capital-raising plans that offer vague language and little accountability. So the current wave reflects two things at once: companies genuinely need capital, and the market is willing to listen again when the use of proceeds is specific enough.

That is why VND 289.5 trillion should not be read as automatically bullish. For issuers, more equity can fund expansion, deleveraging or listing preparation. For shareholders, every new share is also a redistribution of economic rights. If post-issuance profit does not rise quickly enough, EPS and ROE will come under pressure even if the company looks larger on paper.

Banks are doing most of the heavy lifting

Banks account for the biggest chunk of the pipeline, with planned fundraising of roughly VND 128 trillion in 2026.TBTCVN In plain terms, a bank that wants to lend more, absorb more risk or meet stricter capital standards needs a thicker capital cushion. Without it, balance-sheet expansion gets constrained quickly.

This is where newer investors often oversimplify the story. A bank capital raise is not automatically a green flag, but it is not automatically a red flag either. Raising equity to improve capital adequacy and support loan growth is a very different story from issuing shares while asset quality is deteriorating or profits are losing momentum.

Brokerages are raising money ahead of market demand

The next major bucket is financial services, mainly securities firms, with an expected VND 48.2 trillion in planned fundraising.TBTCVN This group is especially easy for retail investors to relate to because the impact of capital is visible almost immediately: more margin capacity, larger proprietary books, stronger underwriting ability and a broader product set.

In other words, brokerages are not raising capital simply to dress up their balance sheets. They are preparing operating capacity for a market that could become deeper, faster and more demanding. But that is also why dilution matters so much here. If a firm issues a large number of new shares and profit only edges up afterward, existing shareholders may own a bigger institution in theory while their per-share claim on earnings becomes thinner in practice.

Real estate needs capital, but the use of funds comes first

Real estate companies have nearly VND 37.3 trillion of planned equity issuance, up 68% from a year earlier.TBTCVN This is the part of the story that demands the most caution, because the same act of issuing shares can mean very different things across companies.

If the cash is going into legally clear projects with visible execution progress and identifiable future cash flow, a new issuance can support genuine growth. If the proceeds are mainly being used to relieve debt pressure, stretch liquidity or patch operating cash-flow gaps, shareholders should read that issuance as a defensive move before treating it as an opportunity.

For first-time investors, the framework does not need to be complicated. Do not start with “Will the stock go up?” Start with what the company is short of, what the money is for and whether post-issuance earnings power per share is likely to improve. That question is slower than a momentum trade, but it is also what keeps investors from paying growth valuations for growth that exists only in the fundraising memo.

A warmer IPO market does not mean every new listing is cheap

Beyond follow-on issuance, the 2026 IPO market is expected to reach roughly VND 22.4 trillion.TBTCVN That matters because IPO activity is not just about adding new tickers. It also suggests that private groups are again willing to spin off business lines, create stand-alone valuation stories and raise capital around more transparent operating units.

Still, new does not mean cheap. A freshly listed company may have a recognizable brand, strong customer traction and a convincing long-term narrative. Even so, the offer price still has to be tested against profit, cash flow, debt and execution after listing. Buying simply because an IPO feels like early access is an easy way to pay for hope before the numbers catch up.

The real stress test is the wave of new share supply

This is the section that matters most if you already own a stock or are thinking about subscribing to a deal. FiinGroup data shows that total new share supply in 2026, including capital-raising issuance and stock splits, is projected at about 48.2 billion shares. Of that total, 28.8 billion shares come from splits, stock dividends and bonus shares, while more than 19.4 billion shares come from capital-raising issuance, up 91.6% from the previous year.TBTCVN

Those numbers show that the market needs more than better sentiment. It needs genuine absorption capacity. If fresh money is strong enough, the extra supply can accompany a healthy expansion cycle in which companies get capital and investors get more investable options. If inflows do not keep pace, new issuance becomes supply pressure. In that case, the balance sheet may improve before the stock does.

Put more simply, dilution is not a problem when the new money makes the pie grow faster than the slices multiply. It becomes a problem when the share count rises faster than earnings power. That is why two companies can announce capital raises and receive completely different reactions from the market.

What first-time investors should read before backing an issuance

Start with the use of proceeds. Capital earmarked for core expansion, stronger financial capacity, cash-flowing projects or credit growth usually has a clearer operating logic. By contrast, language such as “supplementing working capital” or “restructuring finances” without a concrete roadmap deserves more skepticism.

Then look at the issuance method. Rights offerings give existing shareholders a chance to preserve ownership if they participate. Private placements can bring in strategic investors and fresh resources, but they can also disadvantage existing holders if the issue price is too low or the benefits are not distributed evenly.

Finally, compare the issue price, the market price and the likely post-issuance return profile. A reasonable discount is normal if a deal is going to get done. A very deep discount raises a more basic question: who benefits most from the newly created shares.

The broader takeaway is straightforward. Vietnam's 2026 equity fundraising wave suggests the market is again being used as a capital-allocation channel for the economy, not just a venue for daily trading.TBTCVN The core thesis should stay disciplined: do not treat capital raising as automatically positive or negative. Treat it as a test of growth quality. If new capital goes to productive uses and lifts earnings quickly enough, dilution is a manageable cost. If not, shareholders may be financing a larger company without receiving proportionately larger value.